Defensive Algorithmic Design: Error Handling, Slippage Mitigation, and Backtesting

This analysis examines defensive algorithmic design principles, focusing on comprehensive error parsing, slippage mitigation through execution slicing, and rigorous pre-deployment validation. Engineers must treat market friction as a primary architectural constraint to ensure system reliability and capital preservation.

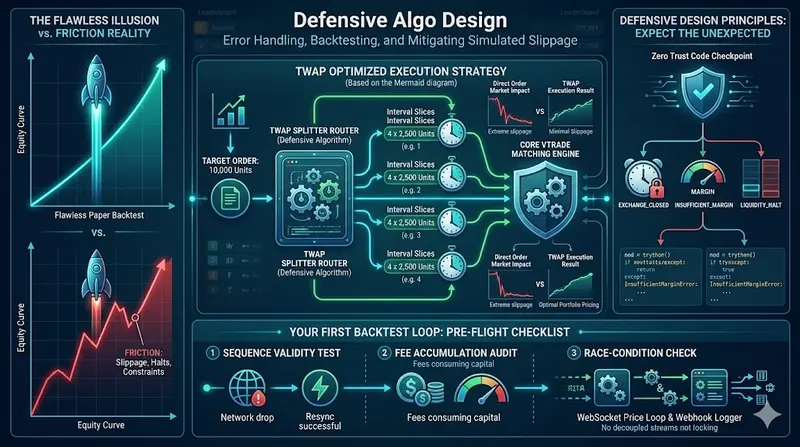

Algorithmic trading strategies frequently exhibit a stark performance gap between theoretical backtests and actual market deployment. Engineers often observe equity curves that appear flawless during development, only to encounter rapid capital erosion upon live deployment. This divergence stems from the absence of real-world market friction during the simulation phase. Understanding and engineering around these frictions requires a fundamental shift in how quantitative systems are architected.

This analysis examines defensive algorithmic design principles, focusing on comprehensive error parsing, slippage mitigation through execution slicing, and rigorous pre-deployment validation. Engineers must treat market friction as a primary architectural constraint to ensure system reliability and capital preservation.

What Causes the Divergence Between Paper Trading and Live Execution?

The transition from theoretical modeling to live deployment frequently exposes a critical vulnerability in quantitative systems. Early algorithmic trading frameworks often operated under the assumption that market liquidity was infinite and transaction costs were negligible. This assumption created a false sense of security during the development phase. Engineers would observe equity curves that climbed vertically without interruption, leading to premature confidence in the underlying strategy. The reality of live markets introduces mechanical friction that paper environments routinely omit. These frictions include volume-adjusted slippage, tiered partial fills, strict exchange session boundaries, and hard margin constraints. When a strategy encounters these conditions, the theoretical edge often evaporates. The system must therefore be designed to anticipate and absorb these costs rather than treating them as anomalies. Modern quantitative infrastructure addresses this by enforcing realistic market conditions from the earliest stages of development. By acknowledging that friction is a constant variable, developers can construct algorithms that remain robust under actual trading conditions. This approach shifts the focus from pure alpha generation to sustainable execution engineering.

How Does Defensive Error Handling Prevent Systemic Failure?

A robust trading system operates under a zero-trust architecture regarding external data streams and network responses. Amateur implementations frequently assume that every application programming interface call will return a successful confirmation block. This expectation creates catastrophic failure points when network latency spikes or market conditions shift abruptly. Defensive engineering requires the transaction layer to parse and intercept specific failure codes rather than allowing exceptions to propagate unchecked. When an asset enters a sudden trading halt, the system must recognize the session boundary violation and queue the order locally. If the account balance approaches leverage limits, the algorithm must automatically scale down the requested volume or halt execution entirely. These specific edge cases demand precise mapping between financial violations and client-side corrections. The architecture must treat unexpected responses as expected events. By implementing structured exception handling, the system can recalculate exposure parameters in real time. This prevents the accumulation of unmanaged floating positions that could trigger margin calls. The engineering discipline required here mirrors high-frequency clearinghouse operations, where state isolation and asynchronous messaging paths maintain system integrity. Developers must prioritize graceful degradation over immediate recovery, ensuring that capital preservation remains the primary objective during abnormal market states.

The Architecture of Time-Weighted Average Price Execution

Large order execution presents a fundamental challenge in quantitative finance. When a system attempts to purchase a substantial position in a single transaction, the order book depth is quickly exhausted. This action pushes the effective fill price deeper into the spread, generating significant market impact costs. The solution involves implementing an automated execution pipeline that distributes volume across time rather than concentrating it in a single block. Time-Weighted Average Price algorithms achieve this by dividing the total target quantity into uniform slices. Each slice executes at predetermined intervals, allowing the market to organically replenish liquidity between transactions. The mathematical foundation relies on dividing the total quantity by the number of execution slices. This calculation determines the precise volume size for each incremental trade. The timing mechanism divides the total execution window by the same integer count, establishing consistent spacing between submissions. This structural approach minimizes the effective slippage factor by preventing sudden demand shocks. It also aligns transaction accounting with broader market volume profiles. Engineers must carefully calibrate the slice size and timing interval to balance execution speed against market impact. Faster execution increases the risk of adverse price movement, while slower execution exposes the position to additional volatility. The optimal configuration depends on historical liquidity patterns and current market depth. Implementing this pipeline requires precise synchronization between the execution scheduler and the order management system. The architecture must handle network retries and partial confirmations without duplicating orders or leaving gaps in the execution timeline.

Which Validation Checks Guarantee Backtest Reliability?

Deploying an algorithmic strategy without rigorous validation introduces unnecessary risk to the capital base. Engineers must verify that the core state machine passes structural checks before allowing the system to interact with live markets. The first validation requirement involves simulating network disruptions in a controlled environment. The client application must detect missing sequence numbers, purge stale in-memory caches, and trigger a clean re-synchronization routine. This ensures that the order book remains accurate during periods of connectivity loss. The second requirement focuses on transaction cost modeling. High-frequency strategies often appear highly profitable during initial testing until trading commissions and exchange fees are factored into the calculations. The algorithm must incorporate the complete fee schedule into its profitability metrics to avoid false positive signals. The third requirement addresses concurrency management. The price processing loop must run entirely decoupled from the transaction confirmation logger. This architectural separation prevents lockups during periods of extreme data throughput. Engineers should implement asynchronous messaging paths to handle WebSocket price feeds and webhook confirmations independently. This design pattern ensures that real-time market updates do not block order execution logic. The validation phase also requires testing against historical market metrics to verify that the execution logic processes time-series datasets accurately. These pre-flight checks establish a baseline for system reliability. They transform theoretical models into production-ready infrastructure capable of withstanding real-world operational stress.

The Broader Implications of Friction-Aware System Design

The principles governing defensive algorithmic design extend far beyond quantitative trading. Modern software engineering increasingly recognizes that theoretical models rarely survive contact with production environments unchanged. Systems must be built to anticipate failure, manage state transitions carefully, and maintain operational continuity under stress. The approach mirrors architectural patterns found in distributed computing and cloud infrastructure. Engineers who treat market friction as a first-class citizen develop more resilient software across all domains. This mindset encourages comprehensive documentation and structured knowledge management. Projects like the Portable Knowledge Mesh demonstrate how single-file offline architectures can preserve critical system information without relying on external dependencies. Similarly, reliable monitoring frameworks emphasize the importance of continuous state validation and automated alerting. These parallels highlight a universal engineering truth: robustness emerges from designing for edge cases rather than ideal conditions. The quantitative trading community has long understood this reality. High-fidelity simulation environments force developers to confront the limitations of their assumptions. By embracing realistic constraints, engineers can build systems that perform consistently across varying market conditions. This discipline reduces technical debt and accelerates the deployment cycle. The focus shifts from chasing theoretical perfection to engineering practical reliability.

Conclusion

Algorithmic trading systems require a fundamental shift in engineering philosophy. Treating market friction as a primary constraint rather than an afterthought transforms how developers approach strategy implementation. Comprehensive error handling, execution slicing, and rigorous validation checks form the foundation of reliable quantitative infrastructure. Engineers who prioritize defensive design principles build systems capable of sustaining performance under actual market conditions. The transition from theoretical modeling to live deployment becomes a matter of architectural maturity rather than speculative guessing.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)