Apple’s iOS 27 Receipt Scanner Reshapes Bill Splitting

Apple is preparing a bill-splitting feature for iOS 27 that photographs receipts, assigns items to individuals, and generates Apple Cash payment requests. The tool, expected to be announced at WWDC, competes directly with Splitwise, Venmo, and Cash App.

Apple’s iOS 27 Receipt Scanner Reshapes Bill Splitting

The intersection of everyday financial friction and digital ecosystem design has long defined the trajectory of mobile payment platforms. Consumers routinely navigate complex workflows when dividing group expenses, often relying on manual data entry or third-party applications that operate outside their primary device environment. A new development in the mobile technology sector suggests a shift toward automated, context-aware financial tools that eliminate traditional barriers to peer-to-peer transactions.

What is the new receipt-scanning bill splitter?

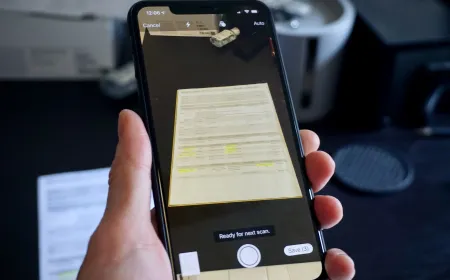

Apple is developing a dedicated financial utility designed to streamline the process of dividing shared expenses. The application will allow users to capture an image of a physical receipt using their device camera. Advanced image recognition technology will then parse the document to extract individual line items, tax amounts, and tip calculations. Users can manually assign specific purchases to different individuals before the system automatically generates payment requests through Apple Cash. The feature will be accessible directly within the Wallet application and the Messages interface, with an additional option to approve incoming transactions using an Apple Watch. Apple plans to introduce the functionality at its upcoming Worldwide Developers Conference before deploying it to the public alongside the iOS 27 update this autumn.

The technical implementation relies on optical character recognition and machine learning algorithms trained to distinguish between food items, beverages, service charges, and regional tax rates. This automated extraction process removes the need for users to manually type in dollar amounts or guess how to split a shared appetizer. The system calculates each participant’s exact share by combining the assigned item costs with a proportional distribution of the total tax and gratuity. By embedding these calculations directly into the payment request, the application ensures that all parties receive a transparent breakdown before any money changes hands.

Why does ecosystem integration matter for peer-to-peer payments?

The decision to embed this functionality within Apple’s existing financial infrastructure represents a deliberate strategy to reduce user friction. Traditional bill-splitting applications require participants to download separate software, create individual accounts, and verify banking information. Apple’s approach keeps the entire transaction lifecycle within a single environment. Users who already utilize Apple Pay for retail purchases or Apple Cash for casual transfers do not need to navigate external platforms or manage additional login credentials. This seamless continuity aligns with a broader industry trend toward consolidating financial utilities into primary operating systems.

Ecosystem integration also influences how consumers perceive the security and reliability of digital transactions. When payment workflows remain contained within a recognized operating system, users benefit from established authentication protocols and encrypted data handling. The Messages integration is particularly significant because it places the financial tool directly within the communication channel where group planning already occurs. Individuals can share a receipt photograph during a conversation about dinner plans and initiate the split without ever leaving the chat interface. This contextual placement reduces the cognitive load associated with managing multiple financial applications.

How does Apple Cash navigate a crowded fintech landscape?

The mobile payment sector has evolved into a highly competitive environment dominated by established platforms and specialized expense-tracking applications. Services like Splitwise have cultivated dedicated user bases by focusing exclusively on shared household and travel expenses. These applications typically rely on manual balance tracking and periodic settlement cycles. Venmo and Cash App operate as broader financial ecosystems that incorporate social networking features, merchant payments, and cryptocurrency trading. Apple’s entry into this space leverages its massive hardware distribution to challenge these incumbents without requiring users to adopt new software.

Market participants have already reacted to the announcement, with shares of PayPal and Block experiencing notable volatility following the report. This financial response underscores the potential disruption a major technology company can introduce into established payment networks. Apple’s advantage lies in its ability to distribute financial tools pre-installed on hundreds of millions of devices. The company does not need to spend heavily on customer acquisition because the hardware itself serves as the distribution channel. This model allows Apple to focus on refining user experience and transaction speed rather than competing for market share through traditional advertising.

The demographic targeting also reflects a shift in how younger consumers manage their finances. Mobile-first generations increasingly prefer app-based money management over traditional banking relationships. These users expect financial tools to be accessible, transparent, and integrated into their daily digital routines. By embedding bill-splitting capabilities directly into the Messages application, Apple aligns its financial infrastructure with the communication habits of this demographic. The feature effectively transforms a standard smartphone into a portable expense management system that operates alongside existing social interactions.

What does Apple’s fintech track record reveal about its expansion strategy?

Apple’s approach to financial services has consistently followed a pattern of aggressive experimentation followed by strategic refinement. The company successfully established Apple Pay as a dominant contactless payment method across numerous global markets. Subsequent initiatives, including Apple Cash peer-to-peer transfers, the Apple Card credit product, and business tap-to-pay solutions, demonstrate a commitment to expanding its financial footprint. However, not every venture has achieved long-term sustainability. The partnership with Goldman Sachs for the Apple Card has created financial pressures, prompting discussions about transferring the business to another institution.

The discontinuation of Apple’s buy now, pay later service further illustrates the company’s willingness to withdraw from ventures that do not meet specific performance thresholds. This pattern suggests that Apple prioritizes ecosystem cohesion and user retention over maintaining every financial product indefinitely. The company appears comfortable allowing underperforming initiatives to fade while doubling down on features that enhance core device functionality. The new bill-splitting tool fits this model by addressing a common consumer pain point without requiring the creation of an entirely new financial platform.

This strategic restraint also extends to how Apple manages third-party partnerships and regulatory compliance. Financial products require extensive licensing, security audits, and consumer protection measures. By keeping the bill-splitting utility contained within its own operating system and payment network, Apple maintains direct control over data handling and transaction processing. This approach minimizes reliance on external financial institutions while reducing the complexity of cross-platform interoperability. The result is a more controlled environment where financial tools operate consistently across all supported devices.

How will the broader iOS 27 update reshape everyday financial tools?

The receipt-scanning utility is part of a larger suite of enhancements coming to the Wallet application in the upcoming operating system release. Apple is also introducing a feature that allows users to create custom digital passes for event tickets, gym memberships, and property access. These additions transform the Wallet application from a simple payment interface into a comprehensive digital identity and asset management hub. The expansion of digital keys and passes reflects a broader industry shift toward consolidating physical credentials into mobile formats.

The iOS 27 update will simultaneously focus heavily on artificial intelligence integration across the entire platform. A revamped Siri assistant will introduce new camera-based interaction modes, while AI-powered photo editing tools will enhance image processing capabilities. This expansion of digital utilities occurs alongside broader hardware developments, such as the recent confirmation regarding the new iPhone 18 Pro Dark Cherry, Light Blue colors. These technological advancements will likely influence how financial applications process data and interact with users. Machine learning algorithms can improve receipt scanning accuracy, detect fraudulent transactions, and provide personalized spending insights.

Embedding financial tools within AI-driven operating systems also raises important considerations regarding data privacy and user consent. Consumers must understand how their transaction history and receipt images are processed and stored. Apple has historically emphasized on-device processing to protect user information, an approach that aligns with growing regulatory scrutiny of data collection practices. The company’s ability to balance advanced functionality with strict privacy standards will likely influence consumer adoption rates. Financial applications that prioritize transparency and local data handling will maintain a competitive advantage in an increasingly privacy-conscious market.

The integration of bill-splitting capabilities into the Messages application also demonstrates how financial infrastructure is becoming invisible to the end user. Transactions no longer require dedicated banking applications or explicit financial planning sessions. Instead, the process occurs naturally within social conversations and daily routines. This normalization of peer-to-peer payments reflects a broader cultural shift toward real-time financial settlement and decentralized money management. As mobile operating systems continue to absorb traditional banking functions, the distinction between communication platforms and financial networks will continue to blur.

What does this mean for the future of mobile finance?

The introduction of automated receipt scanning marks a significant step in the evolution of mobile financial services. By eliminating manual data entry and consolidating payment workflows within a single ecosystem, Apple addresses a persistent consumer inconvenience. The feature’s success will depend on its ability to maintain accuracy, ensure transaction security, and compete effectively against established financial platforms. As operating systems increasingly absorb everyday utility functions, the companies that master seamless integration will define the next generation of digital finance. The trajectory of mobile payments will continue to be shaped by how well technology providers balance convenience, privacy, and ecosystem loyalty.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)