Apple Explores Native Bill Splitting for iOS 27

Apple is reportedly developing a native bill-splitting feature for iOS 27 that will integrate directly with Apple Cash, Messages, and Wallet. The tool aims to streamline shared payments through receipt scanning and automatic tax calculations, challenging established peer-to-peer platforms while reinforcing the company’s broader financial ecosystem strategy.

Apple has long positioned the iPhone as a multifunctional device, but the company is now steering the hardware toward a more centralized role in personal finance. Industry observers note that a new built-in expense-sharing capability is reportedly under development for the upcoming iOS 27 release. This addition would allow users to photograph receipts, allocate costs automatically, and settle balances without leaving the native operating system. The move signals a deliberate shift in how the tech giant intends to manage shared financial transactions.

The Mechanics of Apple’s New Expense Tool

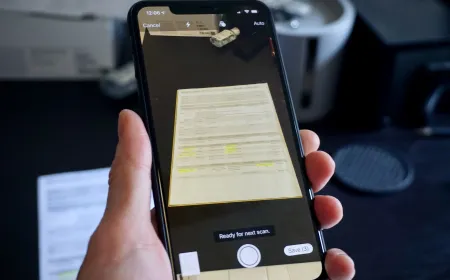

Apple is reportedly preparing to introduce a comprehensive bill-splitting utility that will function across multiple native applications. The system relies on optical character recognition to capture restaurant receipts and identify individual line items. Once the image is processed, the software automatically calculates tax allocations and tip distributions for each participant. Users can then assign specific dishes to friends or family members before generating a formal payment request.

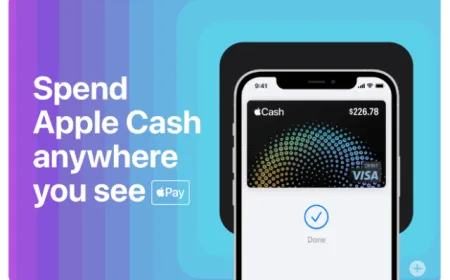

This functionality will operate directly within the Wallet application and the Messages platform. Individuals receiving payment requests can approve or decline the amounts without switching to a third-party application. The interface will also extend to the Apple Watch, allowing users to settle balances quickly during social gatherings or travel scenarios. The design prioritizes speed and reduces the friction typically associated with manual expense tracking.

The underlying architecture draws heavily from Apple’s existing payment infrastructure. Since the initial launch of Apple Pay in 2014, the company has methodically expanded its financial services portfolio. Previous iterations introduced Apple Card, Apple Cash, and Tap to Pay for merchants. Each successive update has focused on removing external dependencies and keeping transactional data within the proprietary environment. The new expense-sharing tool follows this established developmental trajectory.

Receipt scanning technology has evolved significantly over the past decade. Early implementations required manual entry of individual costs and tax rates. Modern algorithms now recognize menu layouts, distinguish between taxable and non-taxable items, and apply regional sales percentages automatically. This advancement allows the feature to function reliably across diverse dining establishments. The system reduces the administrative burden that traditionally accompanies group dining and shared travel expenses.

Why Does Ecosystem Integration Matter for Digital Payments?

The strategic value of embedding financial tools directly into an operating system cannot be overstated. Consumers increasingly prefer unified experiences that eliminate the need to download and maintain multiple applications. When a payment feature operates seamlessly across smartphones, messaging platforms, and wearable devices, it creates a self-reinforcing loop of convenience. Users become less likely to abandon the platform once they experience frictionless transactions.

Apple’s approach contrasts sharply with the standalone application model that dominates the current market. Competing services require users to create separate accounts, verify identities, and manually transfer funds between banking institutions. Apple’s method bypasses these steps by leveraging existing authentication protocols and pre-verified banking relationships. The result is a significantly faster checkout process that appeals to demographics accustomed to instant digital settlements.

Integration also influences long-term user retention metrics. When financial activity becomes deeply woven into daily communication and device usage, switching costs rise considerably. Individuals who rely on native messaging for payment requests find it cumbersome to migrate to external platforms. This retention strategy protects the company’s revenue streams while reducing customer acquisition expenses. The approach prioritizes sustained engagement over temporary promotional incentives.

Wearable technology further amplifies the utility of integrated financial tools. Smartwatches provide quick access to payment approvals during physical activities or professional meetings. The ability to settle a dinner bill with a wrist gesture eliminates the need to retrieve a smartphone. This convenience factor drives adoption among younger demographics who manage shared expenses through digital channels rather than traditional banking methods. The hardware synergy creates a compelling value proposition, especially when paired with the best MagSafe and magnetic wireless chargers for iPhone to ensure devices remain powered during extended use.

How Does Apple Position Itself Against Established Peer-to-Peer Platforms?

The mobile payment landscape features several entrenched competitors with substantial market share. Splitwise has accumulated over ten million monthly active users since its founding and facilitated more than ninety billion dollars in shared expenses. Venmo processes hundreds of billions of dollars annually, while Cash App maintains a user base exceeding fifty-seven million monthly active participants. These platforms have established strong brand recognition and network effects that new entrants must overcome.

Apple’s competitive advantage lies in its pre-installed user base and hardware integration capabilities. The company does not need to convince consumers to download a new application or migrate their banking credentials. The feature arrives automatically with the next major operating system update. This distribution model allows Apple to capture casual users who currently rely on third-party apps for occasional expense tracking. The barrier to entry for competitors increases with each new native capability.

Market dynamics shift when a dominant platform introduces a function that previously required external software. Developers of standalone expense-tracking applications face pressure to differentiate through advanced analytics, subscription models, or cross-platform compatibility. Casual users often abandon niche apps in favor of built-in alternatives that require zero additional configuration. This consolidation trend benefits the platform owner while challenging independent software vendors to innovate beyond basic payment routing.

The competitive landscape also reflects broader consumer behavior regarding financial privacy and data security. Users increasingly prefer services that do not sell transaction data to third-party advertisers. Apple’s business model relies primarily on hardware sales and subscription services rather than data monetization. This distinction influences consumer trust and encourages adoption among privacy-conscious demographics. The company leverages this positioning to attract users seeking secure, transparent financial tools.

What Are the Broader Implications for Apple’s Financial Strategy?

Apple’s financial expansion has encountered notable regulatory and operational challenges in recent years. The partnership behind Apple Card faced financial headwinds that required strategic restructuring. The company also discontinued its buy-now-pay-later offering shortly after its initial launch. These setbacks demonstrate the complexities of navigating consumer credit markets and banking partnerships. Each initiative requires careful risk management and compliance with evolving financial regulations.

Despite these obstacles, the company continues to prioritize financial services as a core growth driver. Revenue from services has consistently outpaced hardware sales growth in recent quarters. Expanding the financial ecosystem increases the average revenue per user while strengthening platform loyalty. The new expense-sharing feature represents a low-risk entry point that enhances utility without introducing complex lending products. This measured approach aligns with long-term profitability targets.

The integration of financial tools also supports broader corporate objectives regarding environmental and social governance. Reducing reliance on physical currency and paper receipts aligns with sustainability initiatives. Digital transactions generate fewer carbon emissions compared to traditional banking infrastructure. Consumers increasingly evaluate technology companies based on their environmental impact and ethical business practices. Apple leverages these values to differentiate its financial offerings from competitors.

Looking forward, the success of this feature will depend on user adoption rates and network effects. If individuals begin requesting and receiving payments exclusively through native applications, the platform will achieve a critical mass. Developers may then build complementary services around the infrastructure, creating an expanded economic ecosystem. The company’s ability to maintain security standards while scaling transaction volume will determine long-term viability in the financial sector.

The Broader Context of iOS 27 and Apple Intelligence

The expense-sharing utility will debut alongside a comprehensive operating system update focused on artificial intelligence. iOS 27 introduces upgraded voice assistant capabilities, enhanced photo editing tools, and deeper system-wide automation. Apple Intelligence aims to personalize device interactions while maintaining strict privacy boundaries. The new financial feature aligns with these objectives by utilizing on-device processing to analyze receipts and calculate splits without transmitting sensitive data to external servers.

Hardware releases continue to complement software advancements. Recent reports indicate that upcoming iPhone models will feature new color options and refined display technologies, a development that aligns with the recent leak confirms new iPhone 18 Pro Dark Cherry, Light Blue colors. These hardware iterations provide the necessary processing power to run advanced machine learning models efficiently. The synergy between software updates and device upgrades ensures that users experience optimal performance across all integrated services. This coordinated development strategy maximizes the value of each annual release cycle.

Consumers evaluating new devices will likely consider the cumulative software experience rather than individual features. A robust financial ecosystem increases the practical utility of the hardware beyond communication and entertainment. Users who rely on native payment tools find greater value in devices that support seamless transaction workflows. This perspective influences purchasing decisions among professionals and students who manage shared expenses regularly. The software ecosystem ultimately drives hardware adoption.

Apple’s approach to financial innovation reflects a deliberate pacing strategy. The company avoids rushing untested products to market and instead focuses on refining existing infrastructure. This methodology reduces technical failures and ensures that new capabilities meet stringent quality standards. The upcoming expense-sharing feature will undergo extensive testing before public release. The company prioritizes reliability over speed, recognizing that financial transactions require absolute trust and precision.

Conclusion

The financial technology sector continues to evolve as consumers demand faster, more secure transaction methods. Apple’s decision to embed expense-sharing capabilities directly into the operating system represents a calculated move toward platform consolidation. By eliminating the need for external applications, the company reduces friction and increases user retention. The feature will operate alongside upgraded artificial intelligence tools and refined hardware designs.

Market dynamics will shift as casual users transition from third-party applications to native solutions. Competing platforms must adapt to a landscape where financial utilities arrive pre-installed on billions of devices. Apple’s strategy emphasizes privacy, convenience, and seamless integration across all owned hardware. These factors collectively strengthen the company’s position in the digital payments market while establishing new industry standards for consumer financial tools.

Long-term success will depend on sustained user engagement and network effects. If individuals consistently utilize native applications for shared expenses, the platform will achieve a self-sustaining ecosystem. The company’s measured approach to financial innovation ensures that new features meet rigorous security and reliability standards. The next operating system release will demonstrate whether this strategy translates into lasting market influence and continued consumer trust.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)