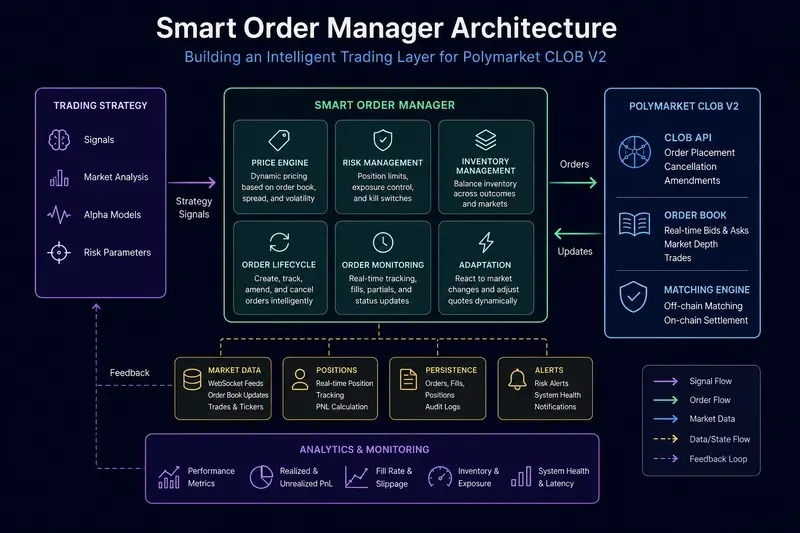

Designing a Smart Order Manager for Polymarket CLOB V2

Automated trading systems require robust execution layers to translate market signals into profitable outcomes. A smart order manager dynamically adjusts pricing, monitors inventory exposure, and enforces risk limits while processing thousands of events per second. This architectural approach minimizes slippage and prevents catastrophic drawdowns in highly volatile prediction markets.

Prediction markets have transitioned from niche forecasting tools into sophisticated financial ecosystems where automated execution dictates profitability. As platforms like Polymarket deploy Central Limit Order Book architectures, the margin between theoretical strategy and actual returns narrows considerably. Traders increasingly recognize that generating accurate directional signals represents only a fraction of the operational challenge. The true differentiator lies in how capital is allocated, monitored, and adjusted across rapidly shifting liquidity conditions.

Automated trading systems require robust execution layers to translate market signals into profitable outcomes. A smart order manager dynamically adjusts pricing, monitors inventory exposure, and enforces risk limits while processing thousands of events per second. This architectural approach minimizes slippage and prevents catastrophic drawdowns in highly volatile prediction markets.

What Defines a Smart Order Manager in Automated Trading?

Traditional algorithmic bots often follow linear workflows that generate signals, submit orders, and wait for fills without continuous oversight. This simplistic approach functions adequately during historical backtesting but frequently fails under live market conditions where liquidity shifts instantaneously and competing participants update quotes continuously. A smart order manager operates as an intermediary layer between raw trading strategies and exchange connectivity. It evaluates real-time market depth, calculates optimal execution prices, and determines whether new capital should be deployed or withdrawn based on current exposure levels.

The architecture must handle multiple concurrent responsibilities without introducing latency bottlenecks. Order creation requires translating abstract strategy signals into precise executable instructions that specify token identifiers, trading sides, price thresholds, and quantity limits. Simultaneously, the system tracks every submitted order through its entire lifecycle, distinguishing between open, partially filled, fully executed, and cancelled states. This continuous tracking prevents duplicate submissions and ensures accurate accounting of available capital across multiple active positions.

Position management extends beyond individual trade records to monitor aggregate exposure across an entire portfolio. Traders cannot evaluate risk by examining isolated transactions in isolation because overlapping positions create hidden directional bias. The system must continuously calculate net inventory for each market, adjusting bid and ask sizes when thresholds are breached. Implementing hard limits on maximum position size prevents uncontrolled accumulation during unexpected volatility spikes or rapid sentiment shifts that could otherwise trigger margin calls or forced liquidations.

How Does Dynamic Pricing Improve Execution Quality?

Submitting static prices represents a fundamental flaw in many early-stage trading implementations. Market conditions evolve continuously, and quotes that appeared attractive seconds ago may become irrelevant as liquidity providers adjust their spreads. A dynamic pricing engine recalculates bid and ask levels based on the current best available prices in the order book. By anchoring new quotes to the prevailing midpoint and applying a calculated fraction of the spread, traders maintain competitive positioning without unnecessarily chasing unfavorable execution rates.

This adaptive approach yields measurable improvements across multiple operational metrics. Orders placed closer to the market center achieve higher fill probabilities because they align with existing liquidity rather than sitting at distant price levels. Participants also benefit from reduced slippage since dynamic adjustments prevent stale quotes from being executed at outdated valuations. The system continuously evaluates whether the current spread justifies participation or if waiting for tighter conditions would yield superior long-term returns.

Intelligent order cancellation complements dynamic pricing by removing stale instructions that no longer reflect market reality. Automated systems must periodically scan active orders and evaluate their age against predefined thresholds. When a quote exceeds its maximum allowable lifespan, the system cancels it to free up capital for newer opportunities. Additional triggers include widening spreads, reversed trading signals, or inventory levels exceeding safety limits. This proactive cleanup prevents accidental fills at unfavorable prices during rapid market transitions.

Why Is Inventory Control Critical for Market Makers?

Professional liquidity providers prioritize inventory management over raw fill counts because unbalanced exposure directly threatens capital preservation. A market maker accumulating a large directional position while attempting to provide two-sided quotes faces asymmetric risk. If the underlying asset moves against that concentration, losses compound faster than hedging mechanisms can correct them. Automated systems must continuously evaluate net positions and adjust quoting behavior accordingly when limits are approached or breached.

Inventory management algorithms modify bid and ask parameters based on current exposure levels. When long positions exceed predefined thresholds, the system reduces bid sizes to discourage further accumulation while simultaneously increasing sell aggressiveness to unwind excess inventory. Conversely, short positions trigger opposite adjustments that encourage buying back shares at favorable prices. This continuous rebalancing maintains neutrality across fluctuating market conditions and prevents concentration risk from dominating the portfolio.

Monitoring tools provide essential visibility into how inventory shifts impact overall profitability. Traders track realized profit and loss alongside active order counts, cancellation rates, and current exposure metrics. Exporting these measurements to observability platforms enables historical analysis and rapid debugging when execution deviates from expectations. Systems lacking comprehensive telemetry operate blindly, making it impossible to identify whether losses stem from strategy flaws or operational inefficiencies in the order management layer.

The Architecture of Event-Driven Order Processing

Polling external APIs at fixed intervals introduces unnecessary latency and network overhead that degrades execution quality. Modern trading infrastructure relies on event-driven architectures where components communicate through published messages rather than continuous requests. Market data updates, order fills, cancellations, and strategy signals trigger specific handlers that process information immediately upon arrival. This design reduces processing delays and allows the system to scale efficiently as market activity increases.

An event bus facilitates communication between independent modules without creating tight coupling dependencies. When a new trade executes on the exchange, the matching engine publishes an order filled event that propagates through the system. The position tracker updates exposure records while the risk module evaluates whether current levels remain within acceptable bounds. Simultaneously, the pricing engine recalculates quotes based on the latest market depth data received through separate WebSocket feeds.

Implementing this architecture requires careful attention to message ordering and state reconciliation. Network interruptions or API rate limits can cause events to arrive out of sequence or duplicate across multiple processing cycles. Production systems incorporate retry mechanisms, idempotent handlers, and persistent storage layers to maintain consistency during connectivity disruptions. Regular order reconciliation compares local records against exchange confirmations to detect discrepancies before they impact capital allocation.

Common Operational Pitfalls in Prediction Market Bots

Overtrading represents a frequent mistake among developers who equate activity with profitability. Submitting excessive orders generates unnecessary transaction fees and increases operational complexity without improving execution outcomes. Systems must implement filtering logic that evaluates whether new quotes offer genuine advantage over existing market conditions before submission. Limiting order frequency reduces noise in the order book and prevents the bot from consuming exchange resources during low-volatility periods.

Ignoring inventory exposure creates hidden vulnerabilities that compound rapidly during adverse price movements. Automated systems must continuously validate position sizes against predefined risk parameters rather than assuming market conditions will remain favorable. Network failures and API rate limits are inevitable in production environments, making robust error handling essential. Developers should implement structured exception handling that logs failures, triggers fallback procedures, and prevents cascading system crashes when external dependencies become unavailable.

The transition from theoretical strategy to live deployment requires treating execution infrastructure as a primary development focus rather than an afterthought. Polymarket Central Limit Order Book V2 provides authenticated endpoints for order management and market data access that demand careful integration. Traders who prioritize robust order handling, dynamic pricing logic, and comprehensive monitoring will achieve superior long-term results compared to systems relying on simplistic submission workflows.

Conclusion

Automated prediction market trading demands precision at every layer of the execution stack. Signal generation alone cannot guarantee profitability when capital allocation, risk management, and order lifecycle handling remain unoptimized. Developers who architect systems around event-driven processing, dynamic pricing algorithms, and continuous inventory monitoring position themselves to navigate volatile conditions effectively. The infrastructure supporting automated strategies ultimately determines whether theoretical edge translates into sustained returns or erodes through operational friction.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)