Cash App Mobile Launches as an AT&T-Based MVNO

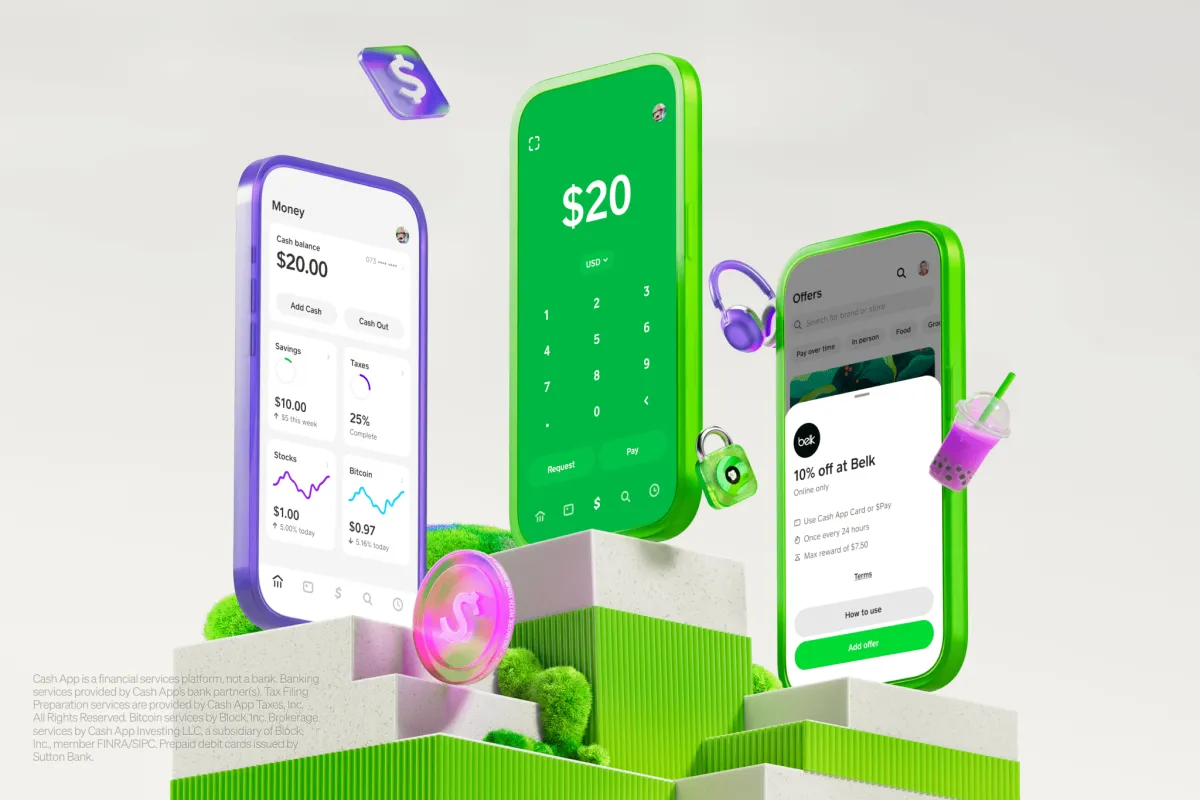

Cash App Mobile is launching as an AT&T-based MVNO powered by Gigs, offering unlimited 5G data, talk, and text for forty dollars monthly. The service integrates with Cash App Green rewards and supervised family accounts, targeting users seeking financial flexibility and ecosystem consolidation.

The intersection of personal finance and telecommunications has long been a quiet frontier, but that boundary is now shifting rapidly. Cash App has officially announced the launch of Cash App Mobile, a new mobile virtual network operator service designed to integrate cellular connectivity directly into its existing financial ecosystem. The service leverages a white-label infrastructure partnership to deliver unlimited 5G data, talk, and text for a flat monthly rate. This move signals a broader industry trend where digital wallets and banking platforms are expanding beyond transactional tools to become comprehensive lifestyle utilities.

Cash App Mobile is launching as an AT&T-based MVNO powered by Gigs, offering unlimited 5G data, talk, and text for forty dollars monthly. The service integrates with Cash App Green rewards and supervised family accounts, targeting users seeking financial flexibility and ecosystem consolidation.

What is Cash App Mobile and how does it function?

Cash App Mobile operates as a mobile virtual network operator, meaning it does not own physical cell towers but instead purchases wholesale network capacity to resell to consumers. The service runs on Gigs, a white-label telecommunications operator that recently facilitated the launch of Klarna’s mobile offering. By utilizing this shared infrastructure, Cash App can deploy a fully functional cellular plan without the massive capital expenditures typically required to build network hardware.

The platform provides unlimited 5G data, unlimited talk and text, unlimited high-definition streaming, and ten gigabytes of monthly hotspot data. Service includes data roaming in Canada and Mexico, positioning it as a viable domestic and cross-border option. The rollout is currently limited to select users, with broader availability expected in the coming months. This phased deployment allows the company to monitor network performance, customer support load, and billing integration before scaling the service to the general public.

White-label operators have become increasingly common in the telecommunications sector, allowing non-traditional companies to enter the market without building physical infrastructure. These partnerships rely on sophisticated software platforms that manage subscriber data, billing, and network routing automatically. Cash App Mobile will leverage these automated systems to handle account creation, plan adjustments, and customer service inquiries entirely through its mobile application. This digital-first approach eliminates the need for physical retail locations and reduces operational overhead significantly.

The underlying network technology utilizes AT&T’s extensive coverage map, which provides reliable connectivity across urban and rural regions. Users will experience standard 5G speeds during peak hours, with potential throttling during periods of high network congestion. The service does not require a physical SIM card, as it will likely utilize eSIM technology for instant activation. This modern activation process aligns with the company’s broader strategy of minimizing friction between financial transactions and daily utility management.

Why does the fintech-to-MVNO shift matter?

The expansion of financial technology companies into telecommunications represents a strategic pivot toward deeper consumer engagement. Traditional carriers have historically relied on device subsidies and long-term contracts to lock in customers, but digital-first platforms are pursuing a different model. By embedding a phone plan within a financial application, companies can capture recurring monthly revenue while increasing daily active usage. This strategy reduces churn rates because users who manage their banking, investing, and mobile service in a single interface face higher switching costs.

The move also reflects a maturation of the fintech sector, which is transitioning from niche payment processors to comprehensive lifestyle managers. As competition intensifies in the digital banking space, offering essential utilities like cellular service provides a tangible differentiator. Consumers increasingly expect seamless interoperability between their financial accounts and daily communication tools, making this shift both economically logical and culturally relevant. The convergence of these industries will likely redefine how consumers evaluate service providers in the coming decade.

Historically, telecommunications and financial services operated as separate regulatory and commercial domains. Carriers focused on network reliability and hardware sales, while banks concentrated on credit, savings, and payment processing. The digital age has blurred these boundaries, enabling platforms to offer bundled services that simplify household management. This trend accelerates as consumers demand greater control over their digital lives and seek consolidated billing solutions. The financial technology industry is now leveraging its existing user base to capture new revenue streams.

Market analysts view this expansion as a natural evolution of super-app strategies that originated in Asian markets. By offering a phone plan alongside peer-to-peer payments and cryptocurrency trading, Cash App creates a closed-loop ecosystem that encourages continuous engagement. Users who rely on the platform for daily transactions are more likely to adopt supplementary services that streamline their financial routines. This approach transforms the application from a utility into a central hub for personal and household management.

How does the pricing structure compare to traditional carriers?

The monthly cost for Cash App Mobile is set at forty dollars, inclusive of all taxes and fees. This pricing model aligns closely with other white-label MVNO services entering the market, such as the recently launched Klarna mobile plan. Traditional major carriers typically charge significantly more for comparable unlimited data packages, often exceeding seventy dollars monthly once promotional discounts expire. The forty-dollar flat rate eliminates surprise charges and simplifies budgeting for users who prefer predictable expenses.

However, the economics of unlimited data plans require careful network management to prevent congestion and maintain service quality. White-label operators mitigate these costs by leveraging shared infrastructure and dynamic data throttling policies. The inclusion of international roaming in Canada and Mexico adds substantial value without inflating the base price. This approach appeals to budget-conscious consumers who prioritize transparency and straightforward billing over extensive physical retail support or premium device financing options.

The forty-dollar price point also reflects a broader industry shift toward flat-rate subscription models that replace complex tiered pricing. Consumers no longer need to calculate overage charges or upgrade their plans when they exceed data limits. This simplicity reduces administrative friction and aligns with modern subscription economy expectations. The financial technology sector has successfully trained users to expect predictable monthly costs for digital services, and cellular connectivity is the next logical extension of that expectation.

Network operators traditionally profit from selling excess capacity to smaller providers, creating a symbiotic relationship between infrastructure owners and virtual operators. Cash App Mobile benefits from this arrangement by accessing premium network infrastructure without bearing the maintenance costs. The company can focus its resources on customer acquisition, app development, and financial product integration. This division of labor allows fintech platforms to compete effectively against legacy carriers that carry heavier operational burdens.

What role does ecosystem integration play in this strategy?

The true differentiator for Cash App Mobile lies in its deep integration with the broader Cash App platform. The service will connect directly to Cash App Green, the company’s rewards program, allowing users to earn benefits on a recurring utility expense. This feature transforms a standard monthly bill into an opportunity for passive accumulation of platform credits. Additionally, the plan integrates with Cash App Families, which manages supervised accounts for children and teenagers. Parents can monitor usage, set spending limits, and align cellular allowances with broader financial education goals.

This level of interoperability mirrors the consolidated digital experiences found in major technology ecosystems, where hardware, software, and services operate as a unified whole. Users who already rely on the platform for peer-to-peer transfers, direct deposit, and cryptocurrency trading will find the transition to a mobile carrier remarkably frictionless. The seamless connection between financial management and telecommunications reduces administrative overhead and creates a sticky user environment. For those navigating complex digital security landscapes, streamlining account management across services often becomes a priority, and unified billing directly addresses that need.

Financial applications are increasingly designed to function as central command centers for personal wealth management. By adding cellular service, the platform expands its utility beyond investment and payment processing into daily operational management. Users can track their phone bill alongside their mortgage, credit card statements, and savings goals within a single dashboard. This consolidation reduces the cognitive load associated with managing multiple financial relationships and minimizes the risk of missed payments. The integration also enables automated savings features that deduct cellular costs directly from linked accounts.

The Cash App Families feature specifically targets households seeking to establish financial discipline among younger members. Supervised accounts allow parents to set data limits, monitor spending patterns, and teach responsible budgeting through real-time tracking. When combined with a mobile phone plan, this tool provides a practical framework for financial education. Teenagers learn to manage their own connectivity expenses while parents maintain oversight of household communications. This dual benefit strengthens the platform’s appeal to multi-generational user bases.

How will this expansion affect consumer behavior and market competition?

The entry of a major fintech platform into the telecommunications market will inevitably reshape competitive dynamics. Established carriers must now compete not only on network coverage and device availability but also on financial incentives and ecosystem convenience. Consumers who prioritize budgeting and financial tracking may gravitate toward services that consolidate expenses into a single monthly statement. This trend could accelerate the decline of traditional postpaid contracts in favor of flexible, app-managed subscriptions. The integration of financial tools with cellular service also raises questions about data privacy and cross-platform analytics.

Companies that successfully merge banking infrastructure with telecommunications will possess unprecedented visibility into user spending habits and communication patterns. Regulatory frameworks will likely need to adapt to address the intersection of financial regulation and telecommunications oversight. Meanwhile, smaller MVNOs may face increased pressure to differentiate through niche demographics or specialized network features. The long-term impact will depend on how effectively these platforms balance convenience with consumer protection and network reliability. Industry stakeholders will need to monitor these developments closely.

Consumer behavior is gradually shifting toward subscription-based models that prioritize flexibility and digital accessibility. Traditional carriers have struggled to retain customers who feel trapped by lengthy contracts and hidden fees. Cash App Mobile offers an alternative that aligns with modern expectations for instant activation, transparent pricing, and seamless cancellation. This model appeals to gig workers, students, and remote professionals who value adaptability over long-term commitments. The ability to manage service entirely through a mobile application further enhances its attractiveness to digitally native demographics.

Market competition will intensify as other financial technology companies evaluate similar expansion opportunities. The success of this venture will determine whether bundled telecommunications services become a standard expectation or a supplementary feature. Legacy carriers may respond by accelerating their own digital transformation efforts or forming strategic partnerships with fintech platforms. The telecommunications industry has historically resisted disruption from outside sectors, but the subscription economy has fundamentally altered consumer expectations. Adaptation will be necessary to maintain market relevance.

What does this mean for the future of digital banking?

The convergence of financial services and telecommunications illustrates a broader transformation in how consumers interact with technology. Digital wallets are no longer confined to transactional exchanges but are evolving into comprehensive lifestyle hubs. This evolution demands robust infrastructure, reliable customer support, and continuous innovation to maintain user trust. As more platforms attempt to replicate this model, the market will likely experience both consolidation and fragmentation. Users will benefit from increased competition and innovative pricing structures, but they must also remain vigilant about data sharing agreements and service terms.

The success of Cash App Mobile will hinge on its ability to deliver consistent network performance while maintaining the financial flexibility that defines its core brand. Industry observers will watch closely to see whether this model becomes a standard expectation or remains a niche offering tailored to specific demographics. The broader financial technology sector continues to demonstrate that convenience and integration are becoming the primary drivers of consumer loyalty. Traditional service providers will need to adapt their business models accordingly.

Financial institutions that embrace ecosystem expansion must carefully balance innovation with regulatory compliance. Telecommunications services fall under different oversight mechanisms than banking products, requiring distinct operational frameworks and customer protection standards. Companies that navigate these regulatory complexities successfully will gain a significant competitive advantage. Those that fail to maintain transparency or data security may face reputational damage and legal challenges. The long-term viability of this model depends on sustainable growth and responsible service management.

The future of digital banking will likely feature even deeper integration between financial products and daily utilities. Consumers will expect their banking applications to manage insurance, healthcare, transportation, and connectivity expenses. This consolidation will simplify household management but will also concentrate significant data and financial power within a few dominant platforms. Regulatory bodies will need to establish clear guidelines for cross-sector service offerings. The industry will continue to evolve as technology enables new forms of financial and utility management.

As digital assistants like integrated AI tools evolve, financial platforms will increasingly rely on automation to manage subscriptions and billing. Voice-activated payment routing and predictive expense tracking will become standard features within bundled utility services. This technological progression will further blur the lines between personal finance applications and telecommunications providers. The next generation of digital wallets will likely function as comprehensive household management systems rather than simple transactional interfaces.

The launch of Cash App Mobile marks a deliberate step toward unifying personal finance with everyday connectivity. By leveraging existing white-label infrastructure and embedding cellular service within a financial application, the company is testing a model that prioritizes convenience and budget transparency. Whether this approach becomes a dominant industry standard or a supplementary feature will depend on network reliability, user adoption, and regulatory developments. Consumers interested in consolidating their financial and communication expenses should monitor the rollout closely and evaluate how the integration aligns with their personal spending habits and network requirements.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)