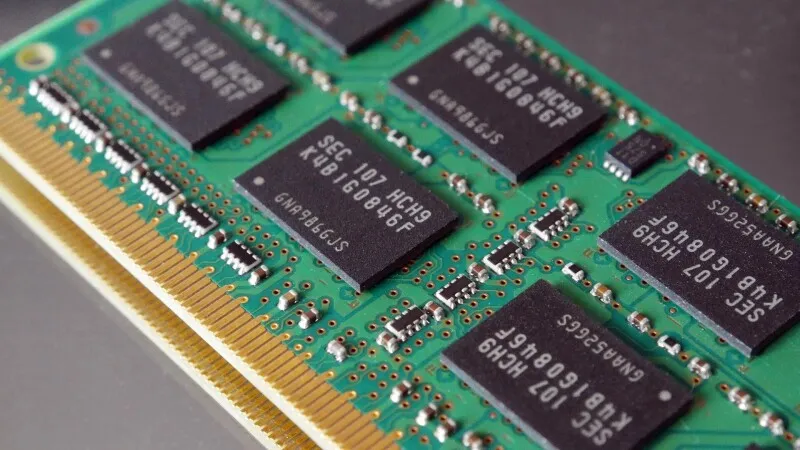

DRAM Prices Surge Amid AI Memory Shortage and Supply Constraints

The ongoing artificial intelligence memory crunch has effectively doubled dynamic random access memory prices in the first quarter of twenty twenty six. Market analysts project further increases of nearly sixty percent this quarter as suppliers prioritize high bandwidth memory for server infrastructure. Conventional memory shortages will likely persist until at least twenty twenty eight, forcing device manufacturers and enterprise buyers to navigate a constrained and increasingly expensive procurement landscape.

The global semiconductor landscape is currently navigating a profound structural shift that extends far beyond laboratory research or specialized data centers. Memory chip manufacturers are witnessing unprecedented revenue growth, yet this financial success masks a tightening supply chain that threatens to reshape hardware pricing for years to follow. As artificial intelligence workloads consume an increasing share of production capacity, the traditional market for standard dynamic random access memory faces severe constraints. Buyers across multiple industries are now adjusting procurement strategies to accommodate a new economic reality where memory costs dictate broader technological adoption rates.

What is driving the current DRAM pricing surge?

The fundamental mechanism behind the current pricing surge lies in a severe imbalance between production capacity and mounting demand. Contract prices for conventional dynamic random access memory experienced a ninety eight percent increase during the first quarter of the year. This dramatic escalation directly correlates with the rapid expansion of artificial intelligence infrastructure, which requires massive amounts of high capacity memory modules. Memory chipmakers have capitalized on this dynamic, reporting an eighty one percent revenue spike that reached ninety seven billion dollars within the same period. The financial metrics clearly indicate a seller market where production constraints dictate terms rather than consumer demand.

Inventory levels held by major suppliers remain critically low, leaving little room for market correction. Any incremental supply that enters the market is immediately diverted toward high capacity registered dual in line memory modules designed for artificial intelligence servers. This prioritization creates a cascading effect where standard memory components become increasingly scarce. Bit shipment growth for conventional dynamic random access memory is expected to remain severely constrained throughout the current quarter. Market forecasting firms anticipate that contract prices for everyday memory components will climb by an additional fifty eight to sixty three percent before the year concludes.

Hyperscale cloud providers have demonstrated a distinct willingness to absorb steep price increases in order to secure necessary supply allocations. This aggressive procurement strategy forces traditional enterprise buyers and consumer electronics manufacturers to follow suit. Companies that previously relied on long term pricing agreements must now navigate a spot market characterized by volatility and rapid escalation. The economic pressure inevitably transfers down the supply chain, altering how hardware is designed, priced, and distributed across global markets.

How does the artificial intelligence demand reshape memory markets?

The architectural requirements of modern artificial intelligence workloads have fundamentally altered semiconductor manufacturing priorities. High bandwidth memory chips represent the highest margin products available to fabricators, making them the primary focus for major production facilities. The top three global suppliers continue to allocate the majority of their advanced process capacity toward these specialized modules. This strategic reallocation leaves conventional memory production to secondary manufacturers or mature manufacturing nodes. The resulting gap in standard memory supply creates a structural deficit that cannot be resolved through temporary production adjustments.

Semiconductor fabrication requires immense capital investment and years of development before new capacity becomes operational. Existing facilities cannot simply switch output between high bandwidth memory and standard dynamic random access memory without significant retooling and validation periods. Manufacturers must carefully balance their production lines to meet both enterprise server requirements and consumer electronics demand. The current market dynamics force a difficult trade off between maximizing short term profitability and maintaining long term supply chain stability for everyday computing devices.

The shift toward specialized memory production also impacts the broader ecosystem of component suppliers. Secondary manufacturers in Taiwan have begun focusing heavily on mature node dynamic random access memory products to fill the market gaps left by tier one suppliers. These companies are expanding their capacity to serve traditional computing and smartphone markets. Their strategic positioning highlights how the industry is adapting to a bifurcated demand landscape where artificial intelligence infrastructure and conventional computing operate under entirely different supply constraints.

The transition from general purpose computing to specialized acceleration architectures has fundamentally altered component valuation. Data centers now require memory bandwidth that exceeds traditional specifications by significant margins. Manufacturers must invest in advanced packaging techniques and specialized testing protocols to meet these rigorous standards. The capital expenditure required for these upgrades further restricts the availability of resources for conventional memory production. This structural reallocation ensures that high bandwidth modules command premium pricing while standard components face persistent scarcity.

Why do conventional memory shortages matter to everyday consumers?

The economic impact of memory shortages extends well beyond server racks and data centers. End consumers bear the final cost of these supply chain imbalances through elevated hardware prices. Average costs for laptop and desktop personal computers have already increased by double digit percentages across major markets. Device manufacturers cannot absorb these component costs without severely compressing profit margins, which would threaten long term business sustainability. Recent hardware announcements, such as the Acer returns to the handheld PC fold, highlight how companies are adapting their product lines to navigate these economic pressures. The pricing adjustments reflect a direct pass through of semiconductor manufacturing expenses to retail channels.

Smartphone producers face similar pressures when designing mid range and budget devices. Standard dynamic random access memory remains a fundamental requirement for mobile computing, and its scarcity forces manufacturers to redesign internal layouts or reduce storage capacities. Some companies may delay product launches while they negotiate supply contracts or source components from alternative channels. The resulting delays and price adjustments create a fragmented consumer market where hardware availability fluctuates based on semiconductor production cycles rather than technological innovation.

Enterprise procurement teams must also adapt their financial planning to accommodate volatile component pricing. Organizations that rely on standardized computing infrastructure for daily operations now face unpredictable budgeting requirements. Long term hardware refresh cycles are being compressed as companies attempt to secure inventory before prices escalate further. This reactive procurement strategy disrupts traditional IT planning and forces technology leaders to prioritize immediate operational needs over strategic infrastructure development.

What does the future hold for memory production and availability?

The timeline for market stabilization depends heavily on the pace of new manufacturing capacity coming online. Major suppliers have outlined ambitious expansion plans, but semiconductor fabrication operates on multi year cycles. SK hynix has announced intentions to double its silicon wafer output capacity, though this expansion will occur gradually over a five year period. Industry observers note that such measured growth suggests the current shortage could persist until twenty thirty. Other analysts maintain a more optimistic outlook, projecting that supply constraints will ease by the end of next year.

Micron has initiated dynamic random access memory manufacturing at its facility in Manassas, Virginia. The company expects initial wafer output at its first Idaho fabrication plant to arrive in the middle of twenty twenty seven. Meaningful new capacity is projected to fully integrate into global supply chains during twenty twenty seven and twenty twenty eight. These timelines indicate that near term pricing will remain elevated as existing demand continues to outpace available production.

Labor relations also play a critical role in production stability. A threatened strike by workers at Samsung Electronics was recently resolved after the company agreed to establish a profit sharing fund. Industrial action would have introduced additional disruption to memory production, potentially worsening the global shortage. The resolution of labor disputes ensures that existing facilities can maintain steady output while new capacity undergoes testing and validation. This stability provides a baseline for supply chain recovery, though it does not immediately address the structural capacity deficit.

Secondary manufacturers continue to expand their operations to capture market share left by primary suppliers. PSMC is expected to aggressively increase its supply capacity for mature node products. Nanya and Winbond are also adjusting their production strategies to serve traditional computing and mobile markets. Their expansion efforts demonstrate how the semiconductor industry naturally reallocates resources when primary producers shift focus toward higher margin segments. This organic adaptation helps maintain some level of conventional memory availability despite the overarching shortage.

Supply chain resilience will depend on coordinated investment across the entire semiconductor ecosystem. Governments and private investors are increasingly recognizing memory production as a critical infrastructure component. Strategic initiatives may accelerate facility construction and reduce regulatory bottlenecks that currently delay capacity expansion. However, the inherent complexity of semiconductor manufacturing means that physical output will always lag behind financial commitments. Buyers must prepare for a prolonged period of elevated component costs as the industry gradually rebalances its production portfolio.

Conclusion

The semiconductor industry is currently navigating a complex transition period that will redefine hardware economics for the foreseeable future. Memory manufacturers are balancing immediate profitability with long term supply chain health as they redirect capacity toward artificial intelligence infrastructure. Device producers and enterprise buyers must adapt to a market where component costs dictate product availability and pricing strategies. The gradual expansion of manufacturing capacity will eventually restore balance, but the transition requires patience and strategic planning across all sectors. Technology leaders who anticipate these supply chain dynamics will be better positioned to manage procurement cycles and maintain operational continuity.

Hardware design teams are already recalibrating their architecture to accommodate higher component costs and limited inventory windows. Engineers prioritize memory efficiency and modular designs that allow for easier upgrades when supply conditions improve. Retail channels are adjusting inventory turnover rates to prevent stockouts during peak procurement periods. The industry will continue to evolve as manufacturers and buyers navigate the intersection of technological advancement and economic constraint. Sustainable growth depends on aligning production timelines with realistic demand forecasts.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)