Apple AirPods Pro 2 Hearing Aid Feature Reshapes Market

Apple’s announcement that AirPods Pro 2 can function as personalized hearing aids triggered immediate stock declines among traditional manufacturers. Analysts emphasize that over-the-counter devices target a different demographic than prescription models. This shift underscores a broader industry transition toward accessible consumer electronics and raises important questions about healthcare competition.

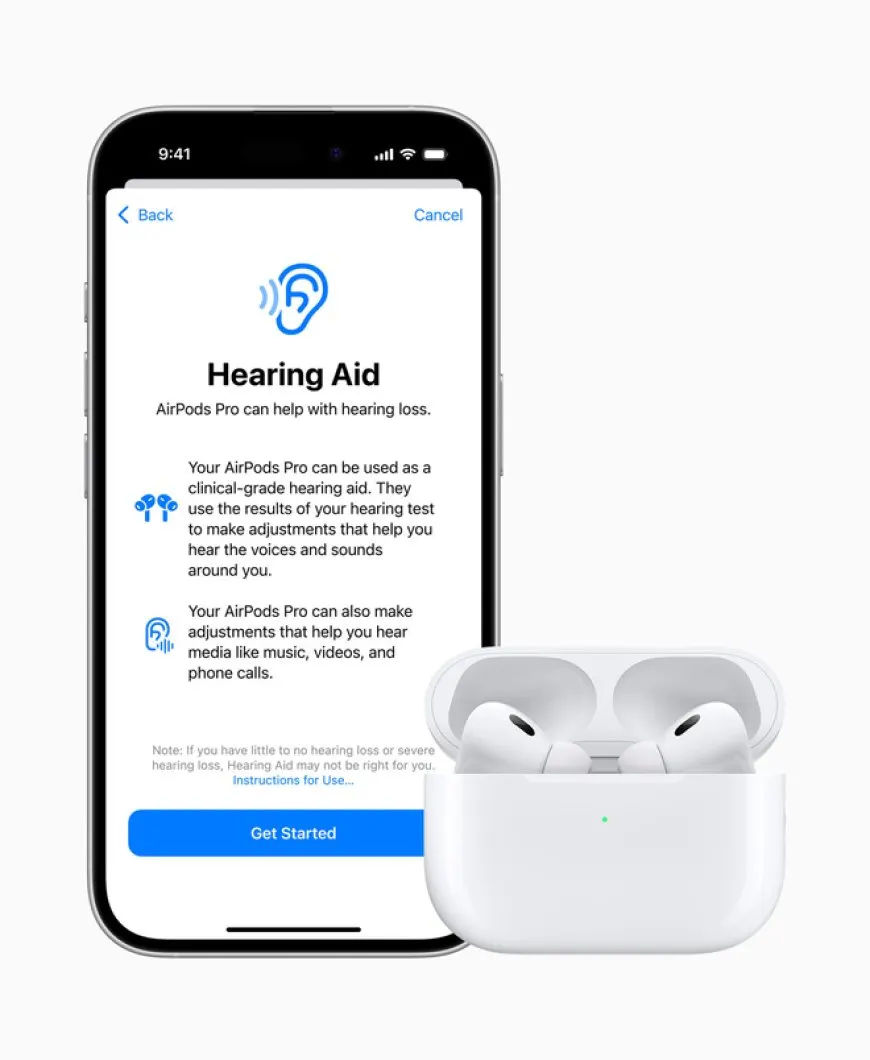

The intersection of consumer electronics and healthcare has always been a complex space, but recent developments are shifting the boundaries in noticeable ways. Apple recently announced that its AirPods Pro 2 can be customized to function as personalized hearing aids through a software update. This capability introduces real-time amplification of specific sounds, tailored to individual preferences. The announcement immediately triggered a measurable response in financial markets, highlighting the growing tension between legacy medical device manufacturers and consumer technology giants.

What Is Driving the Market Reaction to Apple’s Hearing Aid Feature?

Financial markets reacted swiftly to the news, reflecting the substantial revenue streams that traditional manufacturers have historically protected. Shares in Amplifon, a major Italian hearing aid provider, experienced a notable decline during early trading hours. Other prominent industry players, including Sonova, Demant, and GN Store Nord, also recorded drops ranging from two to four percent. These movements illustrate how investors interpret technological advancements in consumer audio as potential threats to established medical device monopolies.

The immediate market response stems from the perception that Apple is entering a highly lucrative sector with a vastly different business model. Traditional hearing aids often carry premium price tags due to extensive research, clinical fitting processes, and proprietary technology. Consumer electronics manufacturers typically operate with thinner margins but rely on massive scale and ecosystem integration. Investors are closely monitoring how these contrasting approaches will interact within the hearing health market.

Analysts from Jefferies have noted that the introduction of over-the-counter devices does not necessarily threaten prescription-based manufacturers. The distinction lies in the target demographic and the level of medical intervention required. Over-the-counter solutions are designed for individuals with mild hearing difficulties who seek convenience and affordability. Prescription devices remain essential for patients with severe hearing loss who require clinical supervision and advanced customization.

The financial sector is also evaluating the long-term implications of software-driven hearing assistance. Apple’s approach relies on continuous software updates and algorithmic improvements rather than hardware replacements. This model challenges the traditional cycle of frequent device upgrades and in-person fittings. Market participants are assessing whether this shift will gradually erode the profit margins of legacy manufacturers or simply expand the overall addressable market for hearing assistance.

How Does the OTC Hearing Aid Market Differ from Prescription Devices?

The regulatory and technological frameworks governing over-the-counter hearing aids differ significantly from those managing prescription models. Over-the-counter devices are intended for adults with perceived mild to moderate hearing loss. They operate without the need for clinical evaluation or professional fitting. This accessibility model removes traditional barriers to entry, allowing consumers to purchase and configure hearing assistance directly through retail channels or digital platforms.

Prescription hearing aids require a comprehensive medical evaluation to determine the precise nature and severity of hearing loss. Audiologists and hearing care professionals use specialized equipment to map individual hearing thresholds. The resulting data guides the configuration of advanced features such as directional microphones, noise reduction algorithms, and frequency-specific amplification. This clinical process ensures that the device addresses the user’s specific auditory needs while preventing further damage.

The level of fitting provided by over-the-counter devices does not suffice for individuals with severe hearing impairment. Clinical studies consistently demonstrate that severe hearing loss requires precise calibration and ongoing professional adjustment. Over-the-counter solutions prioritize ease of use and immediate availability over clinical precision. Users with mild hearing difficulties often find that these devices provide adequate assistance for daily conversations and environmental awareness.

Technological limitations also separate the two categories. Over-the-counter devices rely on standardized algorithms that cannot adapt to complex auditory environments. Prescription models utilize proprietary processing chips that analyze sound in real time and adjust output based on clinical data. The distinction is not merely about price but about the fundamental capability to address different degrees of auditory impairment. Consumers must carefully evaluate their specific needs before selecting a solution.

The Historical Context of Consumer Audio and Healthcare Convergence

The integration of health monitoring features into consumer electronics represents a gradual evolution rather than a sudden disruption. Audio technology has consistently pushed the boundaries of miniaturization and processing power. Early wireless earbuds focused primarily on music playback and call clarity. Subsequent generations introduced active noise cancellation and spatial audio to enhance listening experiences. These advancements naturally laid the groundwork for auditory health applications.

Regulatory changes have also facilitated this convergence. Government agencies in multiple jurisdictions have worked to streamline the approval process for over-the-counter hearing devices. The goal has been to reduce costs and increase accessibility for millions of individuals who experience mild hearing difficulties. By removing stringent medical device classifications for certain products, regulators have created space for consumer electronics companies to enter the hearing health market.

Consumer electronics manufacturers have historically approached healthcare features with a focus on convenience and integration. The strategy involves embedding sensors and processing capabilities into everyday devices rather than creating specialized medical equipment. This approach appeals to users who prefer to avoid the stigma or inconvenience associated with traditional hearing aids. The market response suggests that convenience and affordability are becoming significant factors in healthcare decisions.

The broader industry context reveals a shift toward preventive health and wellness monitoring. Consumers increasingly expect their daily devices to track physiological metrics and provide actionable insights. Hearing health fits naturally into this framework, as auditory decline often begins gradually and goes unaddressed for years. By positioning hearing assistance as a software feature rather than a medical device, companies are normalizing regular auditory care and encouraging earlier intervention.

Why Does Accessibility Matter for Future Audio Technology?

Accessibility remains a central consideration in the development of modern audio technology. Millions of individuals experience hearing difficulties that impact communication, safety, and quality of life. Traditional hearing aids have historically been expensive and difficult to obtain, creating significant barriers to care. The introduction of accessible alternatives addresses a longstanding gap in the market and provides practical solutions for underserved populations.

The economic implications of accessible hearing technology are substantial. High costs have historically prevented many individuals from seeking treatment, leading to social isolation and cognitive decline. Affordable options reduce financial strain and encourage earlier adoption. When hearing assistance becomes integrated into everyday devices, users are more likely to utilize them consistently. Regular use helps maintain auditory function and supports overall cognitive health.

Technological accessibility also extends beyond pricing. The configuration process for over-the-counter devices is designed to be intuitive and user-driven. Individuals can adjust amplification levels and frequency responses based on personal comfort and environmental needs. This user-controlled approach empowers individuals to manage their hearing health independently. It reduces reliance on clinical appointments and simplifies ongoing maintenance.

The broader implications for audio technology involve redefining the relationship between devices and human senses. Future audio systems will likely incorporate adaptive hearing assistance that responds dynamically to environmental changes. Machine learning algorithms will refine amplification strategies based on user feedback and usage patterns. This evolution will blur the lines between entertainment devices and health tools, creating a more seamless experience for users.

The Economic and Regulatory Landscape Ahead

The intersection of consumer electronics and healthcare will require ongoing regulatory oversight and industry collaboration. Governments must ensure that over-the-counter devices meet safety and efficacy standards without stifling innovation. Clear guidelines will help consumers make informed decisions and protect vulnerable populations from misleading claims. Regulatory frameworks will also need to address data privacy concerns associated with health monitoring features.

Manufacturers face the challenge of balancing affordability with clinical reliability. Over-the-counter devices must deliver consistent performance across diverse user profiles and environments. Continuous software updates will play a crucial role in maintaining accuracy and improving functionality. Companies will need to invest heavily in research and development to ensure their algorithms address real-world hearing challenges effectively.

The traditional hearing aid industry must adapt to a changing competitive landscape. Legacy manufacturers are exploring partnerships with technology companies and developing their own over-the-counter lines. Some are focusing on premium clinical services that cannot be replicated by consumer electronics. Others are investing in direct-to-consumer models to compete on price and convenience. The industry will likely consolidate around distinct market segments.

Long-term market stability will depend on consumer education and transparent labeling. Individuals need clear information about device capabilities, limitations, and appropriate use cases. Healthcare providers will continue to play a vital role in diagnosing severe hearing loss and recommending appropriate interventions. The coexistence of consumer electronics and medical devices will require clear communication about their respective roles in hearing health.

Looking Toward a More Integrated Future

The emergence of software-driven hearing assistance in consumer audio devices marks a significant shift in how auditory health is approached. Traditional manufacturers face new competitive pressures, but the market for hearing assistance continues to expand. Over-the-counter solutions provide practical alternatives for individuals with mild hearing difficulties, while prescription devices remain essential for complex medical cases. The industry will continue to evolve as technology advances and regulatory frameworks adapt. Future developments will likely focus on improving accessibility, enhancing algorithmic precision, and fostering collaboration between consumer electronics and healthcare sectors.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)