IBM Spins Off America's First Quantum Chip Foundry With $2B Funding

IBM is launching Anderon, a dedicated quantum chip foundry backed by two billion dollars in federal and private capital. The Albany-based facility will produce three hundred millimeter wafers for competing hardware vendors, aiming to establish a neutral manufacturing ecosystem similar to traditional semiconductor foundries while navigating complex geopolitical funding landscapes.

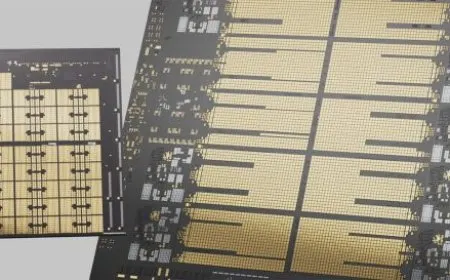

IBM has officially announced the creation of Anderon, a standalone enterprise designed to function as America’s first pure-play quantum chip foundry. The initiative is supported by a proposed one billion dollar research and development award from the CHIPS Act alongside a matching one billion dollar cash investment from the technology corporation. Headquartered in Albany, New York, the new facility will operate a three hundred millimeter quantum wafer fab and extend manufacturing services to competing quantum hardware vendors. This structural shift marks a deliberate attempt to establish a neutral third-party manufacturer capable of fabricating superconducting qubit wafers for the broader industry.

What is the strategic purpose behind establishing a dedicated quantum foundry?

The quantum computing sector has historically operated through vertically integrated models. Every operational quantum computer to date has been constructed by a single organization that designs, fabricates, and operates its own hardware. Anderon represents a fundamental departure from this paradigm. By spinning off a standalone manufacturing entity, IBM intends to build the quantum computing industry equivalent of a traditional semiconductor foundry. This approach mirrors the evolution of classical chip manufacturing, where design and fabrication eventually separated to accelerate innovation and reduce capital barriers.

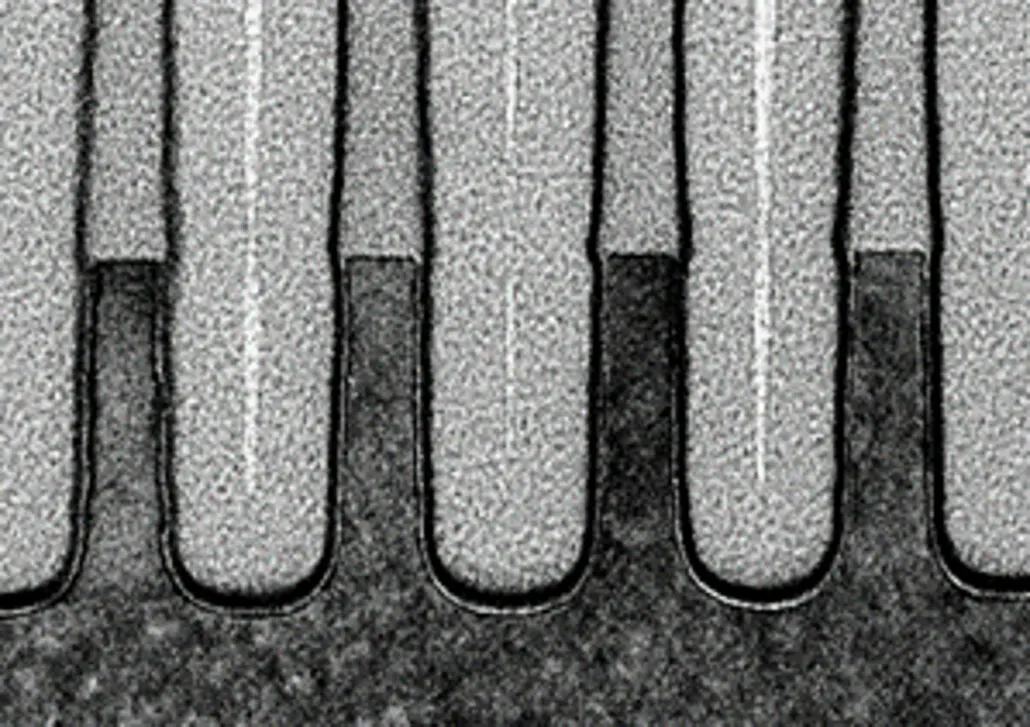

A dedicated foundry with established process design kits, in-line wafer testing, and baseline production routes could allow other superconducting quantum companies to bypass the years and capital required to construct their own cleanrooms. The initial fabrication process will support superconducting wiring, through-silicon vias, and bump interconnects, with documented plans to expand into alternative qubit modalities over time. This structural change aims to accelerate hardware iteration cycles across the entire ecosystem. The transition toward a foundry model introduces significant operational considerations for participating hardware vendors.

Companies that currently maintain closed fabrication loops must evaluate whether outsourcing yields tangible efficiency gains or introduces unacceptable supply chain vulnerabilities. The quantum hardware market remains highly specialized, with distinct architectural requirements dictating manufacturing processes. Superconducting circuits demand precise control over metallic deposition and lithography, while trapped-ion and photonic systems rely on entirely different material science frameworks. Anderon's explicit focus on superconducting architectures initially means that addressable customers will be limited to Rigetti, IQM, SEEQC, and a handful of smaller enterprises.

Whether these organizations will actually outsource to a facility owned by their largest rival remains to be seen. The decision will ultimately depend on how companies balance manufacturing access against the risk of sharing proprietary process knowledge. The comparison to TSMC is inevitable, yet a fundamental difference exists in corporate strategy. TSMC succeeded partly because its founder, Morris Chang, made an explicit promise not to compete with the companies that outsourced their fabrication. IBM obviously cannot credibly make that promise, as it claims more than ninety operational quantum computers and an ecosystem spanning over three hundred twenty-five Fortune fifty companies, universities, and government agencies.

This dual role as both manufacturer and competitor creates inherent tension. Hardware startups considering Anderon must weigh three hundred millimeter production access against the risk of sharing process knowledge with their largest rival. Google, which builds its own superconducting chips at its Santa Barbara facility and recently demonstrated quantum advantage on its one hundred five qubit Willow processor, is unlikely to outsource fabrication to IBM. IonQ and Quantinuum use trapped-ion architectures with almost no process commonality with superconducting silicon, and Microsoft's topological qubit program is on a different fabrication path entirely.

How does the Albany facility reshape semiconductor manufacturing for quantum hardware?

The physical infrastructure at the Albany NanoTech Complex provides a critical foundation for this new manufacturing model. IBM transitioned its quantum processor production from two hundred millimeter wafers to three hundred millimeter silicon wafers at this location, which is the largest public-private semiconductor research and development facility operated by the nonprofit NY CREATES. Jay Gambetta, the Director of Research at IBM, noted that this dimensional shift produces device output roughly thirty times faster by multiplying device complexity tenfold and tripling devices per line.

Current production processors like Heron r2 hold one hundred fifty-six fixed-frequency qubits, while the recently deployed Nighthawk processor packs one hundred twenty qubits in a square lattice with two hundred eighteen tunable couplers. The facility also hosts tenants including GlobalFoundries, Samsung, Applied Materials, ASML, Tokyo Electron, and Lam Research. New York State previously committed one billion dollars toward a High-NA EUV Accelerator at the complex as part of a broader ten billion dollar public-private partnership. This existing ecosystem provides the necessary supply chain density for advanced quantum fabrication.

The move to three hundred millimeter wafers aligns with broader industry trends toward scaling classical semiconductor production. Larger wafers enable higher throughput and reduced per-chip costs, which are essential for commercial viability. IBM's fault-tolerance roadmap targets the Starling processor in twenty twenty-nine at roughly two hundred logical qubits running one hundred million gates, followed by Blue Jay in twenty thirty-three at two thousand logical qubits and one billion gates. All of those future chips require three hundred millimeter fabrication capabilities.

A dedicated foundry with established process design kits, in-line wafer testing, and baseline production routes could allow other superconducting quantum companies to bypass the years and capital required to construct their own cleanrooms. The facility's location on the SUNY Polytechnic campus also creates a direct pipeline for academic research and specialized workforce development. This geographic concentration of expertise may accelerate the translation of theoretical quantum mechanics into manufacturable hardware. The choice of Albany carries historical irony given IBM's previous divestment of regional chip manufacturing.

The company sold its East Fishkill three hundred millimeter fab and Essex Junction two hundred millimeter fab to GlobalFoundries in twenty fourteen for one point five billion dollars. Those operations were losing roughly seven hundred million dollars per year combined. GlobalFoundries later sold East Fishkill to ON Semiconductor in a deal finalized in twenty twenty-three, and IBM and GlobalFoundries settled years of litigation over the original terms in January twenty twenty-five. This manufacturing exit contrasts sharply with the current investment strategy, illustrating a complete reversal in corporate priorities.

The broader federal investment landscape and corporate equity dynamics

The two billion dollar commitment to Anderon functions as the centerpiece of a larger two point zero one three billion dollar federal quantum portfolio distributed across nine companies. GlobalFoundries received a separate three hundred seventy-five million dollar allocation to launch a Quantum Technology Solutions foundry covering multiple qubit architectures. The remaining seven recipients each received smaller awards, with D-Wave, Rigetti, Atom Computing, Infleqtion, PsiQuantum, and Quantinuum each receiving one hundred million dollars, while the Australian startup Diraq will receive up to thirty-eight million dollars.

Federal funding structures typically require non-foundry companies to grant the government a minority, non-controlling equity stake. Rigetti disclosed a memorandum of understanding regarding a fifteen percent discount on common stock, while GlobalFoundries separately disclosed a one percent federal equity stake. IBM's announcement contains no equivalent equity-stake disclosure for Anderon, which stands as a notable distinction given recent precedents in government technology funding. The absence of immediate equity terms suggests a different regulatory framework or a deliberate strategic choice to maintain corporate control over the new foundry.

Government involvement in private technology development has evolved significantly in recent years. The Trump administration previously converted part of Intel’s CHIPS Act manufacturing award into a roughly ten percent government equity stake, establishing a precedent for direct federal ownership in critical infrastructure. Anderon's funding structure appears to diverge from that model, potentially reflecting negotiations over intellectual property rights and commercialization timelines. The distinction between pure-play foundries and multi-architecture research initiatives also influences how federal dollars are allocated and monitored.

GlobalFoundries will cover superconducting, trapped-ion, photonic, and silicon-spin designs, creating a broader technological safety net. Anderon's singular focus on superconducting qubits represents a more targeted industrial policy approach. This specialization may yield faster manufacturing breakthroughs but could also concentrate risk within a single hardware pathway. The long-term implications of these funding choices will become apparent as the industry matures and commercial deployment timelines clarify. Definitive documents between IBM and the Department of Commerce have not yet been executed.

Why does the global funding race matter for quantum computing development?

The American quantum package arrives amid an accelerating international spending competition. China's National Venture Guidance Fund authorized one trillion yuan across hard technology sectors, with direct quantum investment estimated at fifteen billion dollars already deployed. Japan has committed roughly seven point four billion dollars to semiconductors and quantum combined under its twenty twenty-five industrialization agenda. The EU Quantum Flagship program allocates one billion euros over ten years. While cumulative U.S. public quantum funding approaches parity with European and Japanese initiatives, the gap with Chinese capital deployment remains substantial.

Market projections vary widely regarding commercial viability. Boston Consulting Group estimates quantum computing could generate up to eight hundred fifty billion dollars in economic value by twenty forty, though this figure describes end-user economic value rather than vendor revenue. McKinsey projects a smaller twenty-eight to seventy-two billion dollar quantum computing revenue market by twenty thirty-five. Industry leaders like Nvidia CEO Jensen Huang have publicly argued that practical quantum computing remains two decades away. These divergent timelines highlight the long-term nature of the current capital allocation.

International competition in quantum technology extends beyond mere financial metrics. National security, supply chain resilience, and technological sovereignty drive policy decisions across multiple governments. The United States has historically led in quantum research output, but manufacturing capacity determines which nations can scale experimental prototypes into deployable systems. Anderon's establishment in Albany directly addresses this manufacturing gap by creating a domestic production hub for advanced quantum processors.

The facility's reliance on public-private partnerships mirrors successful models in classical semiconductor development, where government incentives attracted private capital to build critical infrastructure. However, the quantum sector faces unique challenges, including extreme environmental controls, specialized material requirements, and a limited talent pool. Overcoming these hurdles will require sustained investment and cross-sector collaboration. The success of Anderon will depend on whether competing hardware vendors trust a foundry owned by a direct competitor, or whether they continue to prioritize vertical integration.

Conclusion

The launch of Anderon introduces a new structural variable into an industry defined by rapid iteration and substantial capital requirements. Whether competing superconducting hardware manufacturers will outsource fabrication to a facility owned by their largest rival remains an open question. The decision will ultimately depend on how companies balance manufacturing access against the risk of sharing proprietary process knowledge. Definitive documents between IBM and the Department of Commerce have not yet been executed, and proposed federal awards frequently shrink during due diligence.

The quantum manufacturing landscape will likely evolve through a combination of public incentives, corporate strategy, and technological milestones rather than immediate market consolidation. Stakeholders must monitor how equity terms, international policy shifts, and architectural breakthroughs intersect over the coming decade. The path toward commercial quantum advantage will require sustained collaboration across academia, industry, and government. Anderon's trajectory will serve as a critical indicator of whether neutral foundry models can successfully scale in emerging computing paradigms.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)