Intel and Google TPU Manufacturing Rumors Assessed by Market Analysts

Recent market speculation regarding Intel manufacturing three million Google tensor processing units has drawn sharp corrections from major financial institutions. Analysts emphasize that the partnership primarily involves advanced chip packaging rather than full fabrication, highlighting the critical distinction between assembly and semiconductor production in the current supply chain landscape.

The semiconductor industry operates on a delicate balance between innovation and speculation. Recent reports suggesting a massive manufacturing shift between two technology giants have sparked intense debate among market analysts and supply chain experts. When claims of multi-million unit orders surface, the immediate reaction often leans toward transformative industry realignment. However, a closer examination of the technical and commercial realities reveals a more nuanced picture. The intersection of artificial intelligence hardware demands and foundry capacity constraints continues to shape how major corporations structure their partnerships. Understanding the precise boundaries of these agreements requires separating verified operational details from broader market narratives.

Recent market speculation regarding Intel manufacturing three million Google tensor processing units has drawn sharp corrections from major financial institutions. Analysts emphasize that the partnership primarily involves advanced chip packaging rather than full fabrication, highlighting the critical distinction between assembly and semiconductor production in the current supply chain landscape.

What Drives the Speculation Around Intel and Google?

The recent narrative emerged from a detailed report that suggested Google had committed to a substantial manufacturing agreement with Intel. This claim immediately captured attention because it implies a significant shift in the custom artificial intelligence chip market. Historically, these specialized processors have relied heavily on a single primary foundry partner. The suggestion that a competitor could secure such a large volume of production naturally triggers questions about capacity allocation and strategic diversification. Market participants quickly began evaluating the potential impact on existing supply chain dynamics.

Financial institutions have responded by carefully dissecting the technical specifications mentioned in the initial coverage. The core of the debate centers on whether Intel would actually fabricate the silicon or merely handle the final assembly stages. Packaging technology represents a critical phase in semiconductor manufacturing where individual components are integrated into a functional unit. Experts note that distinguishing between fabrication and assembly is essential for accurately assessing the commercial implications of any reported partnership. The technical boundaries between these processes define the actual scope of corporate cooperation.

The initial report generated significant discussion because it touched upon a fundamental shift in how technology corporations manage their hardware production. When a major design firm considers allocating multi-million unit orders to a secondary manufacturer, it signals a strategic recalibration of supply chain priorities. Industry analysts examine these moves to understand how capacity constraints at primary foundries influence corporate decision-making. The resulting market reaction often reflects broader concerns about production scalability and technological independence.

The semiconductor sector continuously adapts to shifting market demands through strategic resource allocation. Companies evaluate multiple production pathways to maintain competitive advantages in hardware performance. This approach encourages steady innovation across manufacturing ecosystems. Industry participants recognize that sustainable growth depends on balanced partnerships rather than sudden operational overhauls. The resulting ecosystem supports long-term technological progress.

How Does the Packaging Versus Fabrication Distinction Matter?

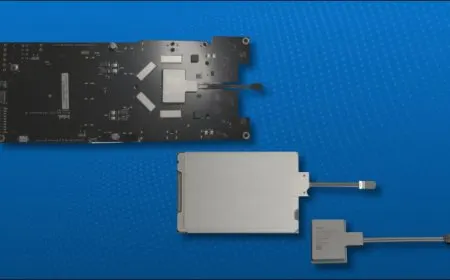

The semiconductor industry relies on highly specialized processes that require different infrastructure and expertise. Fabrication involves creating the actual silicon circuits through complex lithography and chemical treatments. Packaging focuses on connecting these delicate dies to external systems while managing power delivery and thermal performance. Intel has developed advanced interconnect solutions that allow multiple chip components to function as a single unit. These systems offer a cost-effective alternative to competing high-density assembly technologies. The distinction fundamentally changes how investors and industry observers should interpret manufacturing capacity claims.

Major technology companies frequently utilize multiple suppliers to mitigate risk and optimize performance across different product tiers. Lower-power custom processors often benefit from specialized packaging architectures that prioritize efficiency over raw transistor density. When a corporation seeks to expand its production capabilities, it may distribute tasks across different partners rather than consolidating everything under one roof. This approach allows design teams to maintain control over core architecture while leveraging external expertise for assembly. Recent developments in advanced packaging architectures, such as those explored in Intel EMIB-T Packaging Gains Traction as Google Diversifies TPU Supply Chain, highlight how assembly technologies evolve alongside core design requirements.

Advanced interconnect architectures enable manufacturers to combine multiple silicon components into highly efficient processing units. These systems require precise alignment and specialized materials to maintain signal integrity across different chip dies. Companies investing in this technology focus on optimizing power delivery and thermal dissipation rather than increasing transistor counts. The economic implications of choosing specific assembly methods directly impact production costs and overall hardware performance. Recognizing these technical boundaries prevents confusion regarding manufacturing responsibilities.

Why Are Major Financial Institutions Approaching These Claims Cautiously?

Investment banks routinely analyze market reports to separate verified operational data from broader industry trends. Analysts at prominent financial firms have pointed out that the initial coverage lacked concrete evidence regarding full fabrication transfers. They emphasize that existing production schedules and capacity allocations at primary foundries remain tightly controlled. The suggestion that a massive order has already shifted entirely to a new partner requires substantial documentation to be considered accurate. Financial institutions prioritize verified capacity commitments over speculative headlines.

Market participants also consider the technical requirements of next-generation artificial intelligence processors. These advanced chips typically demand cutting-edge lithography nodes for their core computing components. The primary foundry partner continues to utilize advanced process technologies that meet these stringent performance standards. Meanwhile, secondary partners may contribute through specialized assembly techniques that complement rather than replace core manufacturing. This collaborative model allows technology companies to scale production without compromising architectural integrity. Analysts view the reported arrangement as a complementary expansion rather than a complete supply chain replacement.

Market analysts routinely evaluate the credibility of supply chain reports by cross-referencing technical requirements with known production capabilities. They examine whether the proposed manufacturing arrangement aligns with the physical limitations of existing foundry infrastructure. Financial institutions also consider the historical patterns of corporate partnerships to assess the likelihood of rapid operational shifts. This methodical approach ensures that investment decisions remain grounded in verifiable industry data rather than speculative narratives.

What Does This Mean for the Broader Semiconductor Supply Chain?

The ongoing evolution of custom processor manufacturing reflects a broader industry trend toward diversified production networks. Technology companies are increasingly evaluating multiple foundry options to ensure consistent supply and competitive pricing. This strategic shift encourages continuous innovation across the entire manufacturing ecosystem. Competing assembly technologies gain visibility as corporations seek reliable alternatives to established high-density solutions. The resulting competition drives improvements in interconnect design and thermal management across the sector.

Industry observers note that partnerships involving advanced packaging often serve as stepping stones for deeper collaboration. Companies frequently begin with assembly agreements before exploring shared design services or specialized process technologies. This gradual integration allows both parties to align their technical capabilities and operational workflows. Recent developments in custom networking silicon, as seen when Marvell Designs Custom Networking Silicon For Google TPUv8e On Intel Process demonstrates how supply chain partnerships naturally expand across different hardware categories. This collaborative model frequently extends to specialized components.

The semiconductor sector continues to adapt to increasing computational demands through incremental technological advancements. Companies routinely explore multiple manufacturing pathways to maintain competitive advantages in hardware performance and efficiency. This strategic flexibility encourages continuous improvement across assembly techniques and interconnect designs. Industry participants recognize that sustainable growth depends on balanced partnerships rather than unilateral supply chain transformations. The resulting ecosystem supports steady innovation across the entire hardware manufacturing landscape.

Looking Ahead at Hardware Manufacturing Trends

The semiconductor industry thrives on continuous refinement rather than sudden structural overhauls. Corporate partnerships in hardware production typically evolve through measured stages of technical integration and capacity planning. Market narratives often accelerate the perceived timeline of these developments, creating temporary uncertainty among investors and industry participants. A disciplined focus on verified manufacturing capabilities and established technical boundaries provides a clearer understanding of long-term industry trajectories. The ongoing collaboration between design leaders and manufacturing specialists will continue to shape the future of custom processor production.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)