Nvidia Channels $150 Billion to Taiwan Amid US Policy Shifts

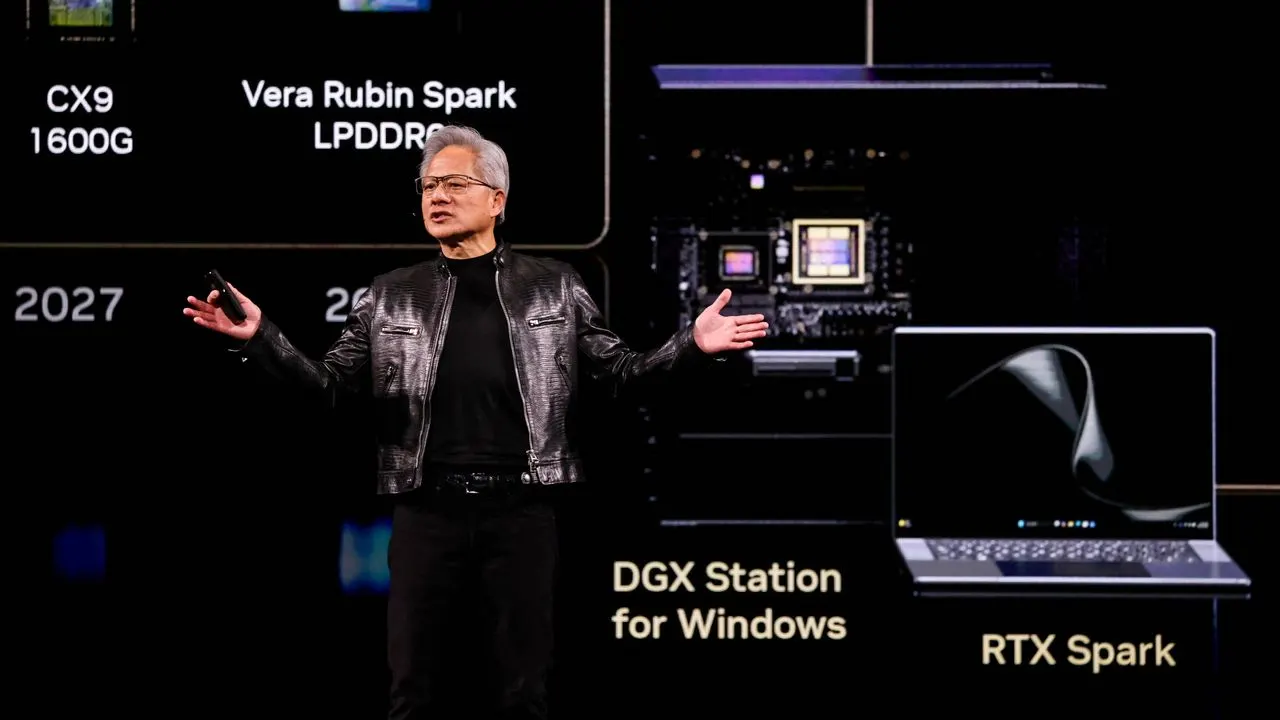

Nvidia CEO Jensen Huang unveiled a $150 billion annual investment plan to establish a new Taiwan headquarters by 2030. The move underscores the region’s irreplaceable role in advanced semiconductor packaging and AI infrastructure development, even as it complicates broader efforts to centralize chip manufacturing within the United States.

The global semiconductor landscape is undergoing a profound realignment as technology leaders navigate the complex intersection of geopolitical strategy and industrial demand. Nvidia recently announced a staggering annual investment of one hundred fifty billion dollars to establish a new headquarters in Taiwan, a decision that underscores the region’s critical position in the artificial intelligence supply chain. This massive capital commitment arrives at a moment when domestic manufacturing initiatives in the United States face significant structural hurdles. The announcement highlights a pragmatic recognition of existing industrial ecosystems over rapidly shifting political mandates.

Why does this massive capital commitment matter for the global technology sector?

The scale of this financial pledge fundamentally alters the competitive dynamics of the semiconductor industry. Historically, advanced chip fabrication and subsequent packaging have been heavily concentrated in East Asia due to decades of accumulated technical expertise and specialized infrastructure. By directing such substantial resources toward this specific geographic region, the company acknowledges that immediate production scaling cannot be rapidly replicated elsewhere. The announcement serves as a clear signal to investors and industry partners that near-term artificial intelligence growth will continue to depend on established manufacturing corridors. This strategic alignment prioritizes operational efficiency and technological continuity over political narratives regarding industrial relocation.

Market observers note that the artificial intelligence infrastructure boom requires unprecedented volumes of high-performance computing hardware. Tech conglomerates are collectively planning to allocate hundreds of billions of dollars toward data center expansion in the current year alone. Meeting this accelerating demand necessitates seamless coordination between chip designers, fabrication facilities, and assembly partners. The proposed headquarters will reportedly serve as a central coordination hub for these complex operations. By consolidating partnerships with regional manufacturers and system integrators, the company aims to streamline production workflows and mitigate potential bottlenecks that could delay next-generation hardware releases.

The financial scale of this initiative reflects the intense competition driving artificial intelligence hardware development. Leading technology firms are racing to deploy next-generation computing architectures that require unprecedented processing power and memory bandwidth. Meeting these performance thresholds demands continuous innovation in chip design and manufacturing processes. The proposed headquarters will reportedly consolidate engineering teams and manufacturing partners under one operational umbrella. This structural integration aims to accelerate product development cycles and reduce coordination delays between design and fabrication stages.

Industry analysts emphasize that the current artificial intelligence boom is fundamentally driven by data center expansion and enterprise software adoption. Cloud providers and independent data center operators are constructing massive facilities to host machine learning workloads. These infrastructure projects require reliable access to high-performance computing hardware on predictable timelines. By securing a dedicated regional hub, the company ensures that production capacity aligns with customer deployment schedules. This operational certainty becomes a competitive advantage in a market where delivery speed directly influences market share.

How does this strategy intersect with existing domestic manufacturing initiatives?

American policymakers have actively promoted the reshoring of semiconductor production to strengthen national supply chains and reduce reliance on foreign facilities. Recent legislative frameworks and executive directives have encouraged technology firms to build domestic fabrication plants and assembly centers. The company initially responded to these pressures by initiating limited artificial intelligence chip production on American soil. Officials highlighted that expanding domestic manufacturing would improve supply chain resilience and support growing national security objectives. However, the technical requirements for advanced packaging remain a significant barrier to fully realizing these domestic ambitions within a compressed timeframe.

The new regional headquarters plan suggests that critical manufacturing capabilities cannot be easily transferred across continents without substantial time and investment. Advanced packaging techniques require highly specialized equipment and a deeply trained workforce that currently exists in concentrated clusters abroad. Attempting to replicate these conditions domestically would likely require years of additional development and capital expenditure. Consequently, the company is pursuing a dual-track approach that balances political expectations with practical engineering realities. This strategy allows continued expansion in targeted markets while gradually building out domestic capabilities over a longer horizon.

Government incentives and regulatory frameworks have successfully attracted initial rounds of domestic fabrication investment. Technology executives have publicly supported these efforts while simultaneously acknowledging the technical limitations of rapid industrial relocation. Advanced semiconductor manufacturing requires highly controlled environmental conditions and specialized chemical supply chains that take years to establish. Attempting to compress these development timelines often results in yield challenges and increased production costs. Companies must therefore balance political expectations with realistic engineering milestones.

The dual-track approach also addresses workforce development requirements that domestic facilities currently lack. Advanced chip packaging demands technicians and engineers with deep experience in microelectronics assembly and testing. Training a qualified workforce to industry standards requires substantial time and financial investment. By maintaining strong operations in established manufacturing regions, the company preserves critical technical knowledge while gradually building domestic training programs. This phased strategy minimizes operational disruption during the transition period.

What are the implications for international trade and export policies?

Geopolitical tensions have introduced new complexities into global technology trade, particularly regarding semiconductor exports to Asian markets. Recent policy proposals have attempted to implement financial levies on specific hardware shipments to certain regions. These measures were designed to generate revenue and encourage domestic production, but they have encountered unexpected resistance from international buyers. Foreign governments have expressed concerns regarding the security and integrity of hardware routed through third-party jurisdictions. This diplomatic friction has complicated sales strategies and forced technology executives to navigate delicate trade negotiations.

Industry leaders have privately acknowledged that restricting access to major consumer markets may ultimately harm domestic manufacturers more than foreign competitors. The Chinese technology sector has accelerated its efforts to develop independent chip architectures and manufacturing processes. Domestic substitution programs are progressing rapidly, reducing the long-term addressable market for foreign hardware suppliers. Executives have noted that conceding specific market segments to local competitors might be a strategic necessity rather than a voluntary retreat. Maintaining commercial relationships in high-growth regions remains essential for sustaining research and development funding.

Diplomatic negotiations surrounding technology trade have become increasingly complex as nations prioritize economic security. Export control mechanisms have been expanded to address national security concerns, but they also create commercial uncertainties for hardware suppliers. Companies operating in this environment must navigate overlapping regulatory requirements from multiple jurisdictions. Compliance costs have risen significantly as firms adapt to evolving trade frameworks. These administrative burdens can slow product deployment and complicate customer relationships in affected markets.

Market dynamics in major Asian economies continue to shift as domestic technology sectors mature. Local manufacturers have made substantial progress in developing alternative chip architectures and fabrication processes. While foreign hardware remains competitive in certain performance segments, domestic substitution programs are gaining momentum. Technology executives recognize that maintaining long-term commercial viability requires adapting to these structural market changes. Strategic planning now incorporates scenarios where foreign suppliers compete directly with domestic alternatives in previously exclusive markets.

How will supply chain diversification reshape the industry over the next decade?

The concentration of advanced semiconductor production in a single region has historically created systemic vulnerabilities for global technology markets. Recent supply chain disruptions have prompted governments and corporations to prioritize diversification strategies that reduce single-point failures. Multiple nations are now investing heavily in domestic fabrication capabilities and supporting allied manufacturing networks. This geographic redistribution will likely occur gradually as technical expertise and infrastructure mature across different regions. The transition will require sustained cooperation between public agencies and private industry stakeholders to ensure seamless integration of new facilities.

Despite these diversification efforts, regional manufacturing advantages will persist for the foreseeable future due to established ecosystem advantages. Decades of accumulated process knowledge, supplier networks, and specialized labor pools create significant barriers to rapid replication. Industry analysts suggest that while domestic production will increase, it will likely focus on mature node technologies rather than cutting-edge fabrication. The most advanced hardware will continue to rely on specialized international facilities for the near term. This reality forces technology companies to balance political objectives with long-term engineering requirements and global market demands.

Geographic redistribution of manufacturing capacity will likely follow a phased implementation model. Initial investments will focus on mature node technologies that require less specialized infrastructure. As domestic fabrication capabilities improve, companies will gradually introduce more advanced production processes. This incremental approach allows manufacturers to build technical expertise while managing financial risk. Industry stakeholders anticipate that full supply chain rebalancing will require sustained investment across multiple decades rather than immediate transformation. Long-term success will depend on consistent policy support and private sector commitment.

Regional manufacturing advantages will persist due to deeply integrated supplier networks and specialized infrastructure. Decades of accumulated process knowledge create significant barriers to rapid replication in new locations. Companies operating in this environment must optimize their global footprint to balance efficiency with resilience. Future supply chain models will likely feature multiple specialized hubs rather than single dominant centers. This distributed architecture reduces systemic vulnerabilities while maintaining access to advanced technical capabilities across different regions. Strategic planning must account for these enduring structural realities.

What does the future hold for global semiconductor supply chains?

The semiconductor industry continues to evolve in response to technological innovation and geopolitical developments. Massive capital commitments to established manufacturing hubs demonstrate that industrial ecosystems cannot be rebuilt overnight through policy directives alone. Companies operating at the forefront of artificial intelligence development must prioritize supply chain stability and technical capability to meet accelerating global demand. Future market dynamics will likely reflect a hybrid model that combines regional specialization with gradual domestic expansion. Stakeholders across the technology sector will need to adapt to a landscape where engineering realities continue to shape commercial outcomes and investment strategies.

Looking ahead, the technology sector must prepare for a prolonged period of structural adaptation. Supply chain managers will need to develop more flexible procurement strategies that account for shifting trade policies and regional manufacturing capabilities. Investment decisions will increasingly weigh technical feasibility against political incentives. Industry participants who successfully navigate these complexities will likely secure stronger competitive positions in the evolving global market. The intersection of engineering constraints and economic policy will continue to define the trajectory of semiconductor manufacturing for years to come. Long-term industry stability depends on balanced strategic planning.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)