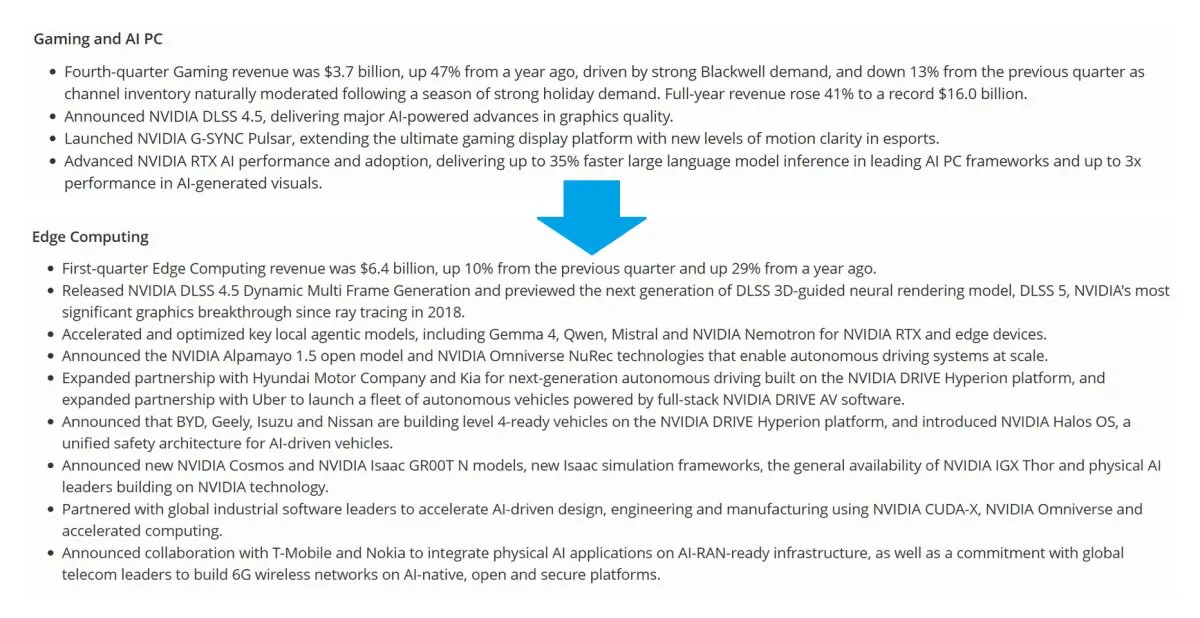

NVIDIA Shifts Gaming GPU Revenue to Edge Computing Segment

NVIDIA has reclassified its GeForce RTX gaming graphics processing unit revenue to fall under the Edge Computing segment in its latest quarterly financial disclosures. This reporting change coincides with a record-breaking eighty-one point six billion dollar revenue quarter, reflecting a strategic alignment between consumer hardware and distributed computing architectures. The shift highlights evolving market dynamics and offers investors a clearer view of how traditional gaming components integrate into modern infrastructure.

Corporate financial reporting often evolves alongside technological landscapes, and recent disclosures from one of the world’s leading semiconductor manufacturers highlight a notable shift in how consumer hardware revenue is categorized. The company recently announced that revenue generated from its GeForce RTX gaming graphics processing units will now be reported under the Edge Computing segment. This adjustment arrives alongside a record-breaking quarterly revenue figure of eighty-one point six billion dollars, underscoring the rapid expansion of the broader computing ecosystem.

What is the significance of NVIDIA's recent reporting shift?

Corporate accounting practices require regular adjustments to ensure that financial statements accurately reflect the underlying business model. When a technology leader moves an entire product line from one reporting category to another, it signals a fundamental change in how the organization views its market positioning. The decision to place GeForce RTX gaming graphics processing unit revenue within the Edge Computing segment indicates that the company no longer considers these components purely as standalone consumer peripherals. Instead, the hardware is being treated as a foundational element of distributed processing networks. This classification change does not alter the physical characteristics of the chips or the performance metrics delivered to end users. It simply recontextualizes the financial data to align with current architectural realities. The gaming division has historically operated as a distinct profit center, providing consistent cash flow that funds research and development for data center and artificial intelligence workloads. Moving these figures into a broader infrastructure category suggests that the boundaries between consumer gaming hardware and professional edge devices are becoming increasingly porous. Analysts will need to adjust their valuation models to account for this structural change. The underlying business strategy remains focused on maximizing hardware utilization across multiple domains, but the accounting framework now emphasizes connectivity and distributed processing over isolated consumer sales.

How does segment reclassification reflect broader industry trends?

The technology sector has experienced a prolonged period of convergence, where distinct hardware categories increasingly share architectural DNA and market trajectories. Graphics processing units originally designed for rendering complex video game environments now serve as critical accelerators for machine learning inference, autonomous vehicle navigation, and industrial automation. This overlap has made traditional reporting categories less useful for understanding actual market dynamics. When financial statements continue to separate gaming revenue from infrastructure revenue, they can obscure the true scale of a company’s total addressable market. The recent adjustment aligns corporate reporting with the reality that modern graphics processors are no longer confined to desktop towers or gaming laptops. They are deployed in retail kiosks, medical imaging systems, smart city infrastructure, and compact server racks. This trend is visible across the semiconductor industry, where manufacturers are deliberately designing silicon that can operate efficiently in both high-performance data centers and constrained edge environments. The reclassification also mirrors a shift in customer acquisition strategies. Sales teams are increasingly bundling gaming hardware with enterprise software licenses, cloud credits, and developer tools. This cross-pollination makes it difficult to isolate gaming revenue without artificially fragmenting a unified commercial strategy. The broader industry is moving toward a model where hardware serves as a gateway to recurring software and service revenue. Financial reporting frameworks must evolve to capture this reality. Segment boundaries are becoming less about physical form factors and more about computational workload distribution.

Why does the reclassification of gaming revenue matter for investors?

Financial transparency requires that investors receive data in a format that supports accurate forecasting and risk assessment. When a major semiconductor firm alters how it reports revenue from one of its most recognizable product lines, it directly impacts how analysts track growth trajectories and margin trends. The immediate effect is a temporary disruption in historical comparability. Investors who have relied on gaming revenue as a standalone metric must now integrate those figures into a larger infrastructure category. This does not diminish the importance of the gaming market, but it does require a more nuanced approach to financial analysis. The reclassification also provides a clearer picture of how consumer hardware contributes to the company’s overall ecosystem strategy. Gaming graphics processing units often share core architectures with professional workstation components and edge inference accelerators. Grouping these revenue streams together allows stakeholders to evaluate the combined health of the silicon portfolio rather than analyzing isolated product cycles. Market participants will need to monitor aggregate infrastructure margins and total addressable market expansion rather than focusing exclusively on traditional gaming sales channels. This approach reduces the noise caused by seasonal consumer demand fluctuations and highlights the underlying stability of the broader computing platform. The shift also encourages a more holistic view of supply chain dynamics, as manufacturing capacity for gaming chips directly supports edge deployment pipelines. Investors who understand this interconnectedness can better anticipate how production constraints or architectural updates will impact overall financial performance. The reclassification ultimately serves as a reminder that modern hardware valuation requires looking beyond individual product categories to examine systemic technological integration.

How does edge computing intersect with traditional gaming hardware?

The technical relationship between consumer gaming processors and edge computing infrastructure is rooted in shared architectural principles. Both domains require high parallel processing capabilities, low latency data handling, and efficient thermal management within constrained physical spaces. Graphics processing units designed for real-time rendering have naturally evolved to handle complex mathematical operations required for artificial intelligence workloads. This evolution has made gaming hardware highly suitable for edge deployment scenarios where centralized cloud processing is impractical or too expensive. The reclassification acknowledges that the same silicon architecture can be optimized for different operational contexts without requiring entirely separate product development cycles. Manufacturers can leverage gaming research and development to advance edge computing capabilities, and vice versa. This bidirectional flow of innovation accelerates the deployment of intelligent devices across retail, manufacturing, and transportation sectors. The financial reporting change reflects this technical reality by removing artificial barriers between consumer and professional hardware categories. It also highlights the growing importance of developer ecosystems, as software frameworks originally built for gaming are increasingly adapted for edge inference applications. The convergence of these markets demonstrates how foundational computing technologies are becoming platform-agnostic. Hardware manufacturers are no longer selling discrete components but rather providing computational foundations that can be deployed across diverse environments. This paradigm shift requires a comprehensive understanding of how silicon, software, and network architecture interact to deliver value. The reclassification provides a more accurate reflection of this integrated approach, allowing stakeholders to evaluate the company’s position within the broader distributed computing landscape.

What are the long-term implications for market analysis?

Financial reporting adjustments of this nature will inevitably reshape how industry analysts and market researchers evaluate semiconductor performance. Historical data will require careful normalization to maintain meaningful year-over-year comparisons. Analysts will need to develop new methodologies for tracking gaming hardware adoption rates within the context of edge infrastructure growth. This transition will encourage more sophisticated modeling techniques that account for cross-segment revenue dependencies and shared supply chain dynamics. The broader market will likely see a decline in isolated product category reporting, replaced by holistic platform valuations. This shift benefits transparency by reducing the potential for misleading narratives that overemphasize consumer hardware sales while underestimating infrastructure contributions. It also aligns financial disclosure with how technology companies actually operate, where research and development, manufacturing, and sales functions are increasingly integrated across multiple product lines. The reclassification does not indicate a decline in gaming hardware relevance, but rather a maturation of the market where consumer and professional applications are deeply interconnected. Stakeholders who adapt their analytical frameworks to this new reality will gain a more accurate understanding of industry trends. The focus will naturally shift toward total silicon deployment, software ecosystem expansion, and long-term infrastructure demand. This perspective provides a more stable foundation for investment decisions and strategic planning. The semiconductor industry continues to evolve at a rapid pace, and financial reporting must remain equally dynamic to capture the full scope of technological advancement.

Conclusion

The reclassification of GeForce RTX gaming graphics processing unit revenue under the Edge Computing segment represents a logical evolution in corporate financial reporting. It aligns accounting practices with the technical reality that modern hardware operates across multiple domains rather than isolated market segments. This adjustment provides a more accurate reflection of how consumer components integrate into distributed computing networks and supports a clearer understanding of overall business strategy. Investors and analysts will need to adapt their evaluation methods to account for this structural change, focusing on aggregate platform performance rather than discrete product categories. The broader semiconductor industry is likely to follow suit as hardware convergence continues to blur traditional boundaries. Financial transparency will improve as reporting frameworks capture the interconnected nature of modern computing ecosystems. This shift underscores the importance of viewing technology companies through a holistic lens, where silicon architecture, software development, and infrastructure deployment are evaluated as a unified whole. The long-term impact will be more sophisticated market analysis and better-informed strategic decisions across the technology sector.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)