PCB Prices Surge Amid Global Specialized Resin Shortage

Printed circuit board prices have increased by approximately forty percent in a single month due to a shortage of high-purity polyphenylene ether resin. A production halt at a major Saudi Arabian complex has disrupted global electronics manufacturing, forcing manufacturers to navigate extended lead times and elevated material costs while consumer pricing remains temporarily stable.

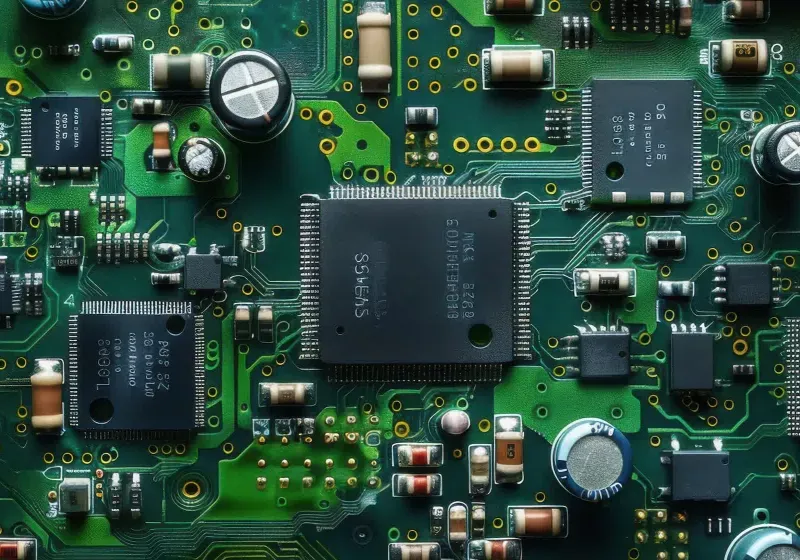

Modern electronics rely on an intricate web of materials that rarely capture public attention until a disruption occurs. A recent surge in printed circuit board costs highlights how deeply interconnected global manufacturing has become. When a single petrochemical facility in the Middle East experienced operational delays, the ripple effects reached every sector that depends on reliable hardware. The resulting price adjustments demonstrate that even minor bottlenecks in specialized chemical supply chains can trigger widespread economic consequences across the technology industry.

Printed circuit board prices have increased by approximately forty percent in a single month due to a shortage of high-purity polyphenylene ether resin. A production halt at a major Saudi Arabian complex has disrupted global electronics manufacturing, forcing manufacturers to navigate extended lead times and elevated material costs while consumer pricing remains temporarily stable.

What is the specific material driving this supply chain disruption?

High-purity polyphenylene ether resin (PPE) serves as a foundational component in modern electronics manufacturing. This specialized chemical compound provides essential thermal stability and maintains signal integrity across complex circuit layouts. Engineers rely on the material to prevent signal degradation in high-frequency applications, which makes it indispensable for next-generation communication infrastructure. The resin also contributes to the structural reliability of boards subjected to rigorous environmental conditions. When production facilities cannot supply adequate quantities, manufacturers lose a critical input that cannot be easily substituted without extensive engineering adjustments.

The chemical properties of this resin make it uniquely suited for advanced printed circuit boards. Traditional epoxy formulations struggle to maintain performance when operating temperatures rise during intensive computational tasks. The specialized polymer structure allows heat to dissipate efficiently while preventing electrical interference. Data centers and telecommunications equipment require these precise characteristics to function reliably. Manufacturers cannot simply switch to cheaper alternatives without compromising device longevity. The technical specifications required for modern hardware leave limited options for material substitution.

Supply chain experts emphasize that the absence of this specific resin creates a bottleneck that affects multiple industries simultaneously. The material functions as a critical binder within the board structure, ensuring that copper traces remain securely attached to the substrate. Without consistent supply, production lines experience delays that cascade through the entire manufacturing process. Companies must navigate complex procurement challenges while attempting to maintain delivery commitments. The situation demonstrates how deeply specialized chemical markets influence global hardware availability.

The chemical synthesis process for this resin requires precise industrial conditions and specialized catalysts. Manufacturing facilities must maintain strict quality control to meet electronics industry specifications. Any interruption in production affects downstream manufacturers immediately. The complexity of the synthesis pathway limits rapid capacity expansion. Companies cannot simply increase output to meet sudden demand spikes. The technical barriers to entry ensure that supply remains concentrated among established producers. This structural reality dictates market dynamics and pricing behavior.

The technical specifications required for modern hardware leave limited options for material substitution. Engineers must verify that alternative compounds meet strict performance thresholds. Testing protocols demand extensive validation before production can resume. The validation process consumes valuable time and financial resources. Companies that maintain strong engineering teams will navigate these challenges more effectively. The situation demonstrates how deeply specialized chemical markets influence global hardware availability. Industry stakeholders must prioritize material research to secure future supply chains.

Why does the Jubail complex matter to global electronics manufacturing?

The petrochemical facility located in Jubail, Saudi Arabia, operated as a joint venture between a major American industrial corporation and a national energy enterprise. Industry analysis indicates that this single location supplied approximately seventy percent of the world high-purity polyphenylene ether resin. The facility experienced operational shutdowns in late March as shipping companies began avoiding the Strait of Hormuz due to regional security concerns. Subsequent missile strikes in early April further damaged an already strained logistics network. The absence of alternative suppliers means that global manufacturers must navigate a complete vacuum in this specialized chemical market.

Geopolitical tensions in the Middle East have historically influenced global energy markets and industrial production. The Strait of Hormuz represents a critical maritime corridor for petrochemical exports. Shipping disruptions force companies to reroute cargo through significantly longer pathways, increasing transit times and operational costs. The initial shutdowns in late March reflected proactive risk management by logistics providers. The subsequent attacks accelerated the decline of an already fragile supply network. Industrial stakeholders now face extended recovery periods that complicate production planning.

Corporate leadership has acknowledged the severity of the disruption during recent financial communications. Executives have indicated that normalizing logistics and supply chains will require approximately nine months. This extended timeline reflects the complexity of rebuilding petrochemical distribution networks. Manufacturers must adjust procurement strategies to account for prolonged delays. The situation highlights the vulnerability of relying on concentrated production hubs for specialized materials. Diversification efforts will likely accelerate as companies seek to mitigate future geopolitical risks.

Regional security assessments directly influence industrial operations and material distribution. Shipping insurers and logistics providers adjust routes based on threat levels. The initial shutdowns reflected conservative risk management strategies. The subsequent attacks accelerated the decline of an already fragile supply network. Industrial stakeholders now face extended recovery periods that complicate production planning. Corporate leadership has acknowledged the severity of the disruption during recent financial communications. Executives have indicated that normalizing logistics will require approximately nine months.

Geopolitical tensions in the Middle East have historically influenced global energy markets and industrial production. The Strait of Hormuz represents a critical maritime corridor for petrochemical exports. Shipping disruptions force companies to reroute cargo through significantly longer pathways, increasing transit times and operational costs. The initial shutdowns in late March reflected proactive risk management by logistics providers. The subsequent attacks accelerated the decline of an already fragile supply network. Industrial stakeholders now face extended recovery periods that complicate production planning.

How are manufacturers responding to the sudden resin shortage?

Electronics producers face significant operational challenges when critical materials become unavailable. Substituting the missing resin requires comprehensive board redesigns and extensive reliability testing protocols. Industry representatives note that lead times for epoxy-resin inputs have expanded from three weeks to fifteen weeks. Major manufacturers are implementing price adjustments to offset rising material costs, with some companies raising rates by up to twenty-five percent. The situation also highlights the historical shift in manufacturing geography, as domestic production capacity has declined significantly over the past two decades. Companies must now manage extended procurement cycles while maintaining production schedules.

The manufacturing landscape has undergone substantial transformation over the last twenty years. Historical data shows that domestic production accounted for nearly thirty percent of global output in the early two thousand s. Current figures indicate that domestic share has fallen to approximately four percent. This geographic concentration creates dependencies that become apparent during supply disruptions. Manufacturers must navigate complex international logistics to secure necessary components. The shift toward offshore production optimized cost efficiency but reduced regional resilience. Companies are now reassessing their supply chain architectures.

Industry observers note that the producer price index reflects broader economic pressures within the manufacturing sector. Processed goods have experienced significant year-over-year increases, with plastic resins emerging as a primary driver. These inflationary trends indicate widespread strain across material markets. Companies must carefully balance cost management with product quality standards. The current environment requires strategic inventory planning and supplier relationship management. Organizations that maintain strong procurement networks will navigate the disruption more effectively. Market dynamics will continue evolving as supply conditions stabilize.

Procurement teams must navigate complex inventory management challenges during periods of material scarcity. Strategic stockpiling provides temporary relief but requires significant capital allocation. Companies must evaluate whether holding excess inventory aligns with long-term financial objectives. The current environment rewards organizations that maintain flexible supplier relationships. Manufacturers that diversify their material sources will reduce vulnerability to future disruptions. Supply chain professionals must balance cost efficiency with operational security. The technology sector will continue adapting to global economic shifts while maintaining innovation momentum.

What does this mean for consumer electronics and future pricing?

The economic impact of material shortages typically follows a predictable trajectory through the technology sector. Initial disruptions manifest as elevated wholesale costs before eventually reaching retail environments. Market analysts suggest that flagship device pricing will likely remain stable in the immediate term due to long-term supplier agreements and strategic inventory management. However, product categories with thinner profit margins may experience earlier price adjustments. Manufacturers of personal computers, networking equipment, and mid-range mobile devices possess less financial flexibility to absorb sudden cost increases. The automotive and data center sectors will also monitor the situation closely as infrastructure projects require reliable component availability.

Large technology corporations possess distinct advantages when navigating supply chain constraints. These organizations maintain substantial scale, sophisticated demand forecasting capabilities, and established supplier relationships. They can rework designs more rapidly than smaller competitors while securing long-term material commitments. Nevertheless, even the largest manufacturers cannot eliminate upstream bottlenecks. Every device still depends on the same global materials network that smaller companies utilize. Strategic inventory management and contract negotiations provide temporary relief but cannot replace physical material availability. The fundamental constraints remain unchanged regardless of corporate size.

Product categories with complex architectures will experience the most pronounced effects. Foldable smartphones require intricate circuit layouts that depend heavily on specialized resins. These devices already operate with tight engineering tolerances and limited margin for material substitution. Manufacturers in this segment must navigate additional procurement challenges while maintaining performance standards. The situation also impacts gaming hardware and peripheral accessories, which rely on consistent component availability. Retail pricing strategies will likely shift as companies evaluate long-term cost structures. Consumers should anticipate gradual adjustments across multiple hardware categories.

Market analysts observe that retail pricing adjustments typically lag behind wholesale cost increases. Companies absorb initial expenses to maintain customer loyalty and market share. However, prolonged material shortages eventually force price revisions across multiple product categories. Consumers may notice gradual adjustments in peripheral accessories and networking equipment. The automotive industry will also monitor component availability closely. Infrastructure projects require reliable supply chains to meet deployment timelines. Organizations that anticipate these shifts will navigate the disruption more effectively.

How will the industry adapt to prolonged supply chain constraints?

Technology companies must develop more resilient procurement strategies to navigate future material shortages. Diversifying supplier networks and increasing regional production capacity will likely become standard industry practices. Engineers will continue optimizing designs to reduce dependency on single-source materials while maintaining performance standards. The current situation underscores the importance of monitoring upstream chemical markets to anticipate downstream hardware costs. Organizations that establish robust contingency planning will maintain competitive advantages during periods of global logistical instability. The technology sector will continue evolving its supply chain frameworks to ensure long-term operational stability.

Academic experts emphasize that policymakers often overlook industrial choke points until crises emerge. The sudden visibility of these bottlenecks highlights the need for proactive supply chain management. Companies must invest in material research and alternative sourcing strategies to reduce vulnerability. The current disruption serves as a catalyst for broader industry transformation. Manufacturers will likely prioritize supply chain transparency and geographic diversification in future procurement decisions. The technology sector will continue adapting to global economic shifts while maintaining innovation momentum. Long-term resilience requires sustained investment in infrastructure and supplier relationships.

Academic research highlights the importance of supply chain transparency in modern manufacturing. Companies must track material origins and production capacity to anticipate potential bottlenecks. The current disruption serves as a catalyst for broader industry transformation. Manufacturers will likely prioritize geographic diversification in future procurement decisions. The technology sector will continue adapting to global economic shifts while maintaining innovation momentum. Long-term resilience requires sustained investment in infrastructure and supplier relationships. Industry stakeholders must collaborate to build robust systems that withstand global volatility.

The intersection of geopolitics and industrial production demonstrates how interconnected modern manufacturing has become. A single facility shutdown can trigger widespread economic consequences across multiple sectors. Supply chain professionals must balance cost efficiency with operational security. The current environment rewards organizations that anticipate disruptions and develop flexible response strategies. Industry stakeholders will continue monitoring material availability and logistics capacity to guide procurement decisions. The technology sector will adapt through strategic planning and collaborative supplier networks. Sustainable growth depends on building robust systems that withstand global volatility.

Technology companies must develop more resilient procurement strategies to navigate future material shortages. Diversifying supplier networks and increasing regional production capacity will likely become standard industry practices. Engineers will continue optimizing designs to reduce dependency on single-source materials while maintaining performance standards. The current situation underscores the importance of monitoring upstream chemical markets to anticipate downstream hardware costs. Organizations that establish robust contingency planning will maintain competitive advantages during periods of global logistical instability. The technology sector will continue evolving its supply chain frameworks to ensure long-term operational stability.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)