Memory Architecture Shifts as Agentic AI Reshapes Global Market Projections

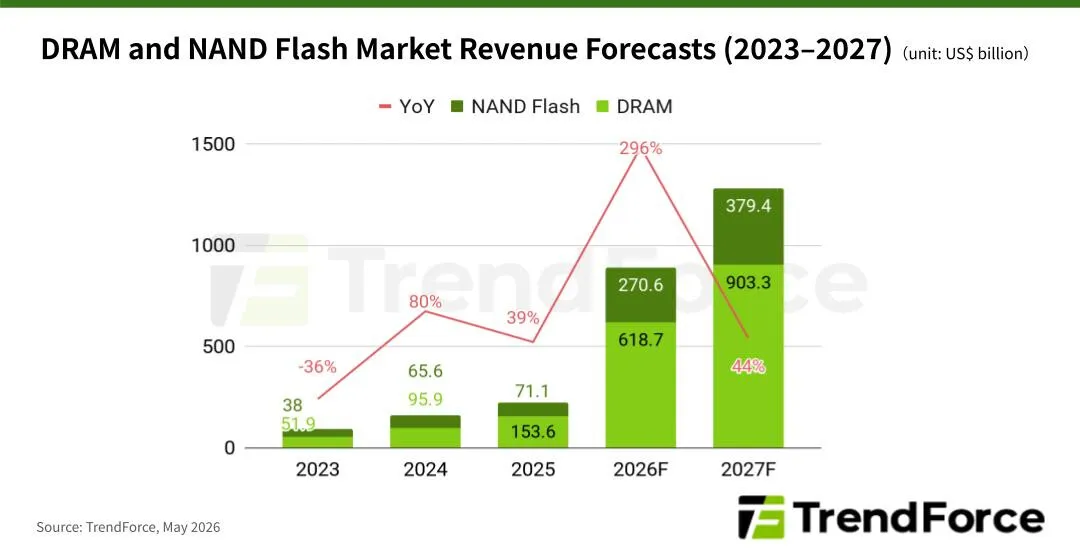

The transition from training-focused artificial intelligence to inference-centric agentic systems is creating a sustained structural expansion in memory demand. Industry analysis indicates that the global memory market will reach one point two eight trillion dollars by twenty twenty seven, while persistent supply deficits continue to challenge short-term infrastructure planning.

The architecture of artificial intelligence is undergoing a fundamental transformation. Developers are moving away from the massive computational bursts required for model training and toward continuous, real-time execution environments. This transition is reshaping the underlying hardware requirements that power modern computing. The industry is now confronting a new set of physical and economic constraints that will dictate the pace of technological advancement for the next decade. Organizations must adapt their infrastructure strategies to accommodate these permanent shifts in data processing demands.

What is driving the structural shift in memory demand?

The evolution of artificial intelligence workloads has fundamentally altered how data centers allocate physical resources. Early generations of machine learning relied heavily on training phases, where models processed static datasets to establish foundational patterns. These phases required immense computational throughput but allowed for batch processing and scheduled maintenance windows. The current generation of intelligent systems operates differently. These platforms function continuously, processing live data streams and making autonomous decisions in real time. This operational model demands immediate access to vast amounts of data without the latency that traditional storage architectures introduce. Memory subsystems must now sustain high bandwidth and low latency simultaneously to prevent bottlenecks. The architectural requirements have shifted from pure computational density to memory capacity and speed. This change forces hardware manufacturers to redesign server racks, upgrade interconnects, and reconfigure cooling systems. The physical footprint of modern data centers is expanding to accommodate these new memory-intensive configurations. Industry analysts observe that the demand curve is no longer cyclical but structural. This means the baseline requirement for advanced memory technologies has permanently elevated. Companies that fail to adapt their infrastructure will face immediate performance degradation. The shift also influences procurement strategies, as organizations must secure long-term supply agreements for specialized memory components. The economic implications extend beyond individual enterprises to global semiconductor manufacturing networks.

Manufacturers are responding by prioritizing the production of high-bandwidth memory modules over traditional dynamic random-access memory. This shift requires retooling fabrication plants and retraining workforces. The transition is gradual and capital intensive. Supply chain managers are establishing long-term contracts with foundries to secure production capacity. These contracts often include clauses that adjust pricing based on raw material costs and yield rates. The geopolitical landscape also influences supply chain dynamics. Governments are investing in domestic semiconductor production to reduce reliance on foreign manufacturing. This decentralization creates multiple production hubs but reduces overall economies of scale. The result is a more complex supply network that requires sophisticated logistics management. Inventory strategies are shifting from just-in-time delivery to strategic stockpiling. Companies are maintaining higher inventory levels to buffer against production delays and transportation disruptions. The industry is also exploring alternative materials and manufacturing techniques to improve yield rates. These innovations require significant research funding and cross-industry collaboration. The supply chain is becoming more transparent as companies share demand forecasts with suppliers. This collaboration helps align production schedules with actual market needs. The evolution of the supply chain will determine the pace of technological adoption. A resilient supply network enables faster deployment of new architectures. A fragile network creates bottlenecks that slow industry-wide progress. The coming years will test the adaptability of global manufacturing networks. Companies that build flexible and transparent supply relationships will gain a competitive advantage. The structural expansion in memory demand will continue to drive innovation in logistics and production.

How does inference-centric computing differ from traditional training workloads?

Training workloads and inference workloads operate under completely different mathematical and physical constraints. Training involves calculating gradients across billions of parameters to adjust model weights. This process is computationally intensive but highly parallelizable across thousands of processors. Once training concludes, the model is deployed for inference. Inference requires the model to retain its learned parameters in active memory while processing incoming queries. Agentic applications add another layer of complexity. These systems must maintain context windows, manage state transitions, and execute multiple concurrent tasks without interruption. The memory architecture must support rapid read and write operations to handle dynamic data structures. Traditional storage solutions cannot meet these requirements because they introduce unacceptable latency. High-bandwidth memory technologies have become essential for maintaining system responsiveness. The physical design of these memory modules prioritizes data throughput over raw capacity. Engineers must balance power consumption with performance to prevent thermal throttling. This balance dictates the layout of server blades and the routing of data buses. The difference between training and inference also affects software optimization. Developers now write code that assumes memory is always available and instantly accessible. This assumption changes how applications are architected and deployed. The industry is responding by standardizing new memory interfaces that reduce communication overhead. These standards aim to minimize the distance between processing units and data storage. The result is a more integrated computing environment where memory and processors function as a unified system.

Software frameworks are being rewritten to accommodate these architectural realities. Legacy applications that rely on sequential data access patterns struggle to perform in modern environments. Engineers are migrating to asynchronous processing models that maximize memory utilization. This migration requires significant refactoring and testing efforts. The industry is also developing new programming languages optimized for high-memory workloads. These languages provide built-in mechanisms for memory management and garbage collection. The shift also impacts debugging and monitoring tools. Traditional profiling utilities cannot capture the real-time memory fluctuations of agentic systems. New diagnostic platforms are being deployed to track memory allocation patterns across distributed networks. These platforms provide visibility into resource consumption and identify bottlenecks before they impact performance. The technical complexity of managing memory at scale is driving demand for specialized engineering talent. Organizations are investing heavily in training programs to upskill their workforce. The talent gap represents a significant bottleneck for industry growth. Companies that develop robust training pipelines will secure a competitive advantage. The technical evolution of inference computing continues to accelerate. Each new generation of processors requires tighter integration with memory subsystems. This integration reduces latency and increases overall system efficiency. The industry is moving toward a future where memory and processing are indistinguishable at the architectural level.

Why does the projected market valuation matter for infrastructure planning?

Market projections provide a roadmap for capital allocation and long-term strategic positioning. The forecast indicating a global memory market valuation of one point two eight trillion dollars by twenty twenty seven reflects a sustained period of growth. This valuation is not driven by speculative demand but by concrete infrastructure requirements. Organizations must align their financial planning with these projections to avoid budget shortfalls. Procurement teams need to anticipate price fluctuations and secure inventory before capacity constraints tighten. The valuation also signals the level of investment flowing into semiconductor fabrication facilities. Manufacturers are expanding production lines to meet the structural demand for advanced memory chips. This expansion requires billions of dollars in capital expenditure and years of construction time. The timeline creates a lag between demand signals and physical supply. Companies that recognize this lag can negotiate favorable terms and establish strategic partnerships. The financial model for data center operators is shifting from operational expenditure to capital expenditure. Building facilities that support high-density memory architectures requires upfront investment. The projected valuation also influences research and development priorities. Companies are funding new memory technologies that offer higher efficiency and lower power consumption. The financial landscape is becoming increasingly consolidated as only large players can afford the necessary scale. This consolidation affects pricing dynamics and supply chain resilience. Investors are monitoring these trends to identify opportunities in semiconductor manufacturing and data center development. The long-term outlook suggests that memory will remain a critical bottleneck for technological progress.

Financial analysts are adjusting their forecasting models to account for these structural changes. Traditional valuation metrics no longer capture the full cost of memory-intensive deployments. New financial frameworks are being developed to measure return on investment more accurately. These frameworks incorporate metrics for memory utilization, latency reduction, and computational efficiency. Enterprises are using these metrics to justify infrastructure upgrades to executive leadership. The financial implications extend to insurance and risk management. Data centers are purchasing specialized policies to cover hardware failures and supply chain disruptions. The cost of downtime is increasing as applications become more dependent on continuous memory access. Risk management teams are developing comprehensive contingency plans to mitigate these threats. The market valuation also influences venture capital funding. Investors are directing capital toward companies developing next-generation memory technologies. This funding accelerates innovation and reduces the time required to bring new products to market. The financial ecosystem is adapting to the realities of modern computing. Capital flows are aligning with technological priorities. The result is a more efficient allocation of resources across the industry. Companies that understand these financial dynamics will navigate the market more effectively. The projected valuation serves as a critical indicator of industry health. It reflects both current demand and future growth potential. Stakeholders use this indicator to make informed decisions about investment and expansion.

What are the practical implications for enterprise and cloud deployments?

Enterprises and cloud service providers face immediate operational challenges as they adapt to these new requirements. The structural expansion in memory demand means that existing hardware configurations are quickly becoming obsolete. Organizations must evaluate their current infrastructure against the performance standards required by modern applications. Upgrading to memory-intensive architectures often requires complete data center renovations. This includes reinforcing floors, upgrading power distribution units, and installing advanced cooling systems. The financial burden of these upgrades is substantial but unavoidable. Companies that delay modernization will experience degraded service quality and increased latency. Cloud providers are responding by offering specialized instances optimized for high-memory workloads. These instances command premium pricing but deliver the performance necessary for agentic applications. Enterprises must carefully calculate the return on investment for these specialized resources. The shift also impacts software licensing models. Vendors are adjusting their pricing structures to reflect the increased memory consumption of their products. This creates a new cost center for IT departments that must track memory utilization across multiple environments. The practical response involves implementing rigorous monitoring and optimization protocols. Teams are adopting automated scaling mechanisms to allocate memory resources dynamically. These mechanisms prevent waste while ensuring that peak demand periods are handled efficiently. The industry is also developing new standards for memory virtualization to improve resource sharing. These standards allow multiple applications to run on the same physical hardware without interference. The practical implications extend to disaster recovery and backup strategies. High-memory systems require specialized backup solutions that can handle large data volumes without impacting performance. Organizations are investing in redundant memory architectures to ensure continuous operation. The practical reality is that memory management has become a core competency for modern IT departments.

The deployment of specialized hardware requires careful physical planning. Server racks must be configured to maximize airflow and minimize heat buildup. Engineers are designing modular chassis that allow for easy component replacement. This modularity reduces maintenance downtime and extends hardware lifespan. The industry is also exploring liquid cooling solutions to manage thermal loads. These solutions provide superior heat dissipation compared to traditional air cooling. The adoption of advanced cooling technologies is accelerating across the sector. Organizations are recognizing that thermal management is critical to system reliability. The practical implications also extend to network architecture. High-memory systems generate massive amounts of data that must be transmitted quickly. Network switches are being upgraded to support higher bandwidth protocols. Cabling infrastructure is being replaced with optical fiber to reduce signal degradation. These upgrades ensure that data moves seamlessly between memory and processing units. The industry is standardizing new networking protocols to improve efficiency. These protocols reduce overhead and increase overall throughput. The practical reality is that memory, processing, and networking must be optimized together. Siloed improvements yield diminishing returns. Integrated optimization delivers sustainable performance gains. Organizations that embrace this holistic approach will achieve superior results. The deployment landscape is evolving rapidly. New standards are emerging to guide infrastructure development. Companies that stay informed will navigate these changes successfully.

How will supply chain dynamics evolve over the coming years?

The semiconductor supply chain is undergoing a period of intense restructuring to meet the new demand profile. Manufacturers are prioritizing the production of high-bandwidth memory modules over traditional dynamic random-access memory. This shift requires retooling fabrication plants and retraining workforces. The transition is gradual and capital intensive. Supply chain managers are establishing long-term contracts with foundries to secure production capacity. These contracts often include clauses that adjust pricing based on raw material costs and yield rates. The geopolitical landscape also influences supply chain dynamics. Governments are investing in domestic semiconductor production to reduce reliance on foreign manufacturing. This decentralization creates multiple production hubs but reduces overall economies of scale. The result is a more complex supply network that requires sophisticated logistics management. Inventory strategies are shifting from just-in-time delivery to strategic stockpiling. Companies are maintaining higher inventory levels to buffer against production delays and transportation disruptions. The industry is also exploring alternative materials and manufacturing techniques to improve yield rates. These innovations require significant research funding and cross-industry collaboration. The supply chain is becoming more transparent as companies share demand forecasts with suppliers. This collaboration helps align production schedules with actual market needs. The evolution of the supply chain will determine the pace of technological adoption. A resilient supply network enables faster deployment of new architectures. A fragile network creates bottlenecks that slow industry-wide progress. The coming years will test the adaptability of global manufacturing networks. Companies that build flexible and transparent supply relationships will gain a competitive advantage. The structural expansion in memory demand will continue to drive innovation in logistics and production.

Logistics providers are adapting their operations to handle larger and heavier components. Transportation routes are being optimized to reduce transit times and minimize damage risks. Warehousing facilities are being upgraded to accommodate specialized storage requirements. These upgrades ensure that memory modules are protected from environmental factors. The industry is also developing new packaging standards to improve durability. These standards reduce waste and lower shipping costs. The practical implementation of these standards requires coordination across multiple stakeholders. Manufacturers, logistics providers, and retailers must align their processes. This alignment creates a more efficient and reliable supply chain. The industry is also investing in predictive analytics to anticipate disruptions. Machine learning models analyze historical data to identify potential risks. These models enable proactive mitigation strategies that prevent delays. The adoption of predictive analytics is transforming supply chain management. Companies that leverage these tools gain a significant operational advantage. The future of supply chain dynamics depends on continuous innovation. Organizations must remain agile to navigate changing market conditions. The structural expansion in memory demand will drive further evolution. Companies that invest in resilience and transparency will thrive.

What steps should organizations take to prepare for memory-intensive workloads?

Organizations must adopt a systematic approach to infrastructure modernization. The first step involves conducting a comprehensive audit of current hardware capabilities. Teams should evaluate memory utilization rates, latency metrics, and power consumption levels. This audit provides a baseline for measuring future improvements. The second step focuses on identifying applications that will benefit most from memory upgrades. High-memory workloads include real-time analytics, machine learning inference, and large-scale data processing. Prioritizing these applications ensures that upgrades deliver maximum value. The third step involves engaging with hardware vendors to understand available solutions. Companies like Beelink ME Pro Storage PC Expansion Targets AI Workloads are developing specialized platforms designed for these exact requirements. Evaluating these platforms helps organizations select hardware that aligns with their technical needs. The fourth step requires developing a phased deployment plan. Rushing upgrades can lead to operational disruptions and budget overruns. A phased approach allows teams to test new configurations in controlled environments before full-scale implementation. The fifth step involves training IT staff on new memory management tools and protocols. Continuous education ensures that teams can maintain and optimize modern infrastructure effectively. The sixth step focuses on establishing monitoring and reporting mechanisms. Real-time dashboards provide visibility into memory utilization and system performance. These dashboards enable proactive adjustments that prevent bottlenecks. The seventh step involves reviewing procurement contracts to ensure flexibility. Long-term agreements should include clauses that accommodate future upgrades and capacity expansions. The eighth step requires aligning infrastructure planning with broader business objectives. Technology investments must support strategic goals rather than operating in isolation. The ninth step involves participating in industry forums to stay informed about emerging standards. Collaboration with peers accelerates knowledge sharing and reduces trial-and-error costs. The tenth step focuses on building a culture of continuous improvement. Organizations must regularly reassess their infrastructure to ensure it remains aligned with evolving demands. The transition to memory-intensive computing is ongoing. Companies that follow these steps will navigate the transition successfully. The process requires patience, investment, and strategic foresight. The rewards include enhanced performance, reduced latency, and improved operational efficiency. The industry is moving toward a future where memory is the primary driver of computational capability. Organizations that prepare now will lead the next generation of technological advancement.

How will hardware vendors adapt to the evolving memory landscape?

Hardware manufacturers are fundamentally redesigning their product lines to address the new demand profile. The focus has shifted from maximizing processor speed to optimizing memory bandwidth. Engineers are developing new chip architectures that integrate memory controllers directly onto the processor die. This integration reduces communication latency and increases data throughput. The physical design of server blades is also changing. Manufacturers are creating modular chassis that allow for easy memory expansion. These chassis support hot-swappable memory modules that minimize downtime during upgrades. The industry is also exploring new materials for memory modules. Advanced substrates and interconnects are being tested to improve signal integrity. These materials reduce power consumption and increase reliability. The manufacturing process is becoming more precise to meet tighter tolerances. Automated inspection systems are being deployed to detect defects early in the production cycle. These systems improve yield rates and reduce waste. The industry is also standardizing new form factors to ensure compatibility across platforms. These standards simplify procurement and deployment for enterprises. Manufacturers are investing heavily in research and development to stay ahead of demand. The pace of innovation is accelerating as competition intensifies. Companies that fail to innovate will lose market share. The hardware landscape is becoming increasingly specialized. Vendors are developing niche products tailored to specific workloads. This specialization allows companies to capture premium pricing and build loyal customer bases. The industry is also collaborating with software developers to optimize performance. Joint development efforts ensure that hardware and software work seamlessly together. The result is a more efficient and powerful computing ecosystem. The evolution of hardware will continue to drive technological progress. Companies that embrace this evolution will shape the future of computing.

What role will policy and regulation play in shaping the market?

Government policies are increasingly influencing the semiconductor and memory markets. Nations are implementing subsidies and tax incentives to attract manufacturing investments. These policies aim to reduce dependency on foreign suppliers and strengthen domestic production. The regulatory landscape is also evolving to address environmental concerns. Governments are setting stricter standards for energy efficiency and waste management. Manufacturers are adapting their processes to comply with these regulations. This adaptation requires additional investment but improves long-term sustainability. The industry is also facing scrutiny regarding data privacy and security. Regulations are being updated to protect sensitive information processed by memory-intensive systems. Companies must implement robust security measures to comply with these requirements. The regulatory environment is becoming more complex but also more transparent. Organizations that engage with policymakers can help shape favorable outcomes. Collaboration between industry and government fosters innovation and economic growth. The market is also influenced by trade agreements and tariffs. These agreements determine the flow of components across borders. Companies must navigate these regulations carefully to maintain supply chain stability. The role of policy will continue to grow as the industry matures. Governments will play a key role in ensuring fair competition and technological advancement. Organizations that understand these dynamics will position themselves for success. The intersection of technology and policy is a critical area of focus. Stakeholders must monitor regulatory developments closely. The future of the memory market depends on a balanced and supportive policy framework. Companies that align their strategies with these frameworks will thrive.

What is the long-term outlook for memory technology innovation?

The long-term outlook for memory technology points toward unprecedented levels of integration and efficiency. Researchers are exploring new physical principles to store and process data. Emerging technologies include phase-change memory, magnetoresistive memory, and optical memory. These technologies promise higher speeds, lower power consumption, and greater durability. The industry is also investigating three-dimensional memory structures to increase capacity without expanding footprint. These structures stack memory cells vertically to maximize density. The manufacturing of three-dimensional memory requires advanced lithography techniques. These techniques are becoming more sophisticated as nodes shrink. The industry is also developing new error-correction algorithms to improve reliability. These algorithms detect and fix data corruption in real time. The result is more stable and predictable systems. The long-term outlook also includes the convergence of memory and processing. Computing architectures are evolving to blur the line between storage and computation. This convergence reduces data movement and increases overall efficiency. The industry is investing heavily in these concepts to secure future competitiveness. The pace of innovation will determine the trajectory of technological progress. Companies that fund research and development will lead the next wave of advancement. The long-term outlook is optimistic but requires sustained commitment. The industry must navigate technical challenges and economic pressures to realize these innovations. The journey toward advanced memory technology is ongoing. Organizations that remain focused on long-term goals will achieve lasting success. The future of computing depends on the continued evolution of memory. The industry is poised for a period of remarkable transformation. Stakeholders must prepare for the opportunities and challenges that lie ahead.

How will the industry measure success in this new era?

Success in the memory-intensive era will be measured by multiple metrics. Traditional benchmarks focused on processor speed and storage capacity. New metrics emphasize memory bandwidth, latency, and power efficiency. Organizations are adopting comprehensive scoring systems that evaluate overall system performance. These systems provide a more accurate picture of operational capability. The industry is also measuring success by deployment speed. Companies that can rapidly scale infrastructure to meet demand gain a competitive advantage. The ability to adapt to changing workloads is a key indicator of success. Organizations are tracking their agility through automated provisioning and scaling capabilities. The industry is also measuring success by cost efficiency. Reducing the total cost of ownership while maintaining performance is a critical goal. Companies are optimizing their operations to minimize waste and maximize resource utilization. The industry is also measuring success by sustainability. Environmental impact is a growing concern for stakeholders. Organizations are tracking their carbon footprint and water usage to improve their sustainability scores. The industry is developing standardized metrics for environmental performance. These metrics allow for consistent comparison across companies. Success is also measured by innovation output. The number of patents filed and new technologies developed indicates industry health. Companies that invest in research and development will lead the market. The industry is also measuring success by customer satisfaction. End-users evaluate systems based on reliability, speed, and ease of use. Organizations that prioritize customer experience will build loyal relationships. The industry is also measuring success by supply chain resilience. Companies that maintain stable operations during disruptions demonstrate strength. The industry is developing risk assessment frameworks to evaluate resilience. These frameworks help organizations identify vulnerabilities and implement solutions. Success in this new era requires a holistic approach. Organizations must balance performance, cost, sustainability, and innovation. The metrics will continue to evolve as technology advances. Companies that adapt their measurement strategies will thrive. The industry is moving toward a future where success is defined by adaptability and foresight. Stakeholders must remain vigilant and proactive to achieve their goals. The journey ahead is challenging but full of opportunity. Organizations that embrace these principles will shape the future of computing.

What is the final trajectory for the global memory market?

The trajectory of the global memory market is firmly aligned with the advancement of artificial intelligence. The shift toward inference-centric computing has created a permanent elevation in hardware requirements. Organizations must approach infrastructure planning with a long-term perspective that accounts for these structural changes. The financial and operational investments required today will determine which companies can compete in the next generation of computing. Supply chain resilience and architectural innovation will remain the primary determinants of market success. The industry must continue to adapt to the physical realities of data processing. The coming years will test the resolve of manufacturers, developers, and investors. Those who commit to sustained innovation will reap substantial rewards. The market will reward those who prioritize efficiency, reliability, and scalability. The industry is entering a period of rapid transformation. Organizations that navigate this transformation successfully will define the future of technology. The structural expansion in memory demand is not a temporary trend but a fundamental shift. The global memory market will continue to grow as computational demands increase. The trajectory is clear, and the path forward requires disciplined execution. Companies that align their strategies with this trajectory will lead the industry. The future of computing depends on the continued evolution of memory technology. The industry is poised for a new era of progress and innovation. Stakeholders must remain focused on long-term objectives to achieve lasting success. The journey ahead is demanding but promising. Organizations that embrace the challenge will shape the next generation of computing. The global memory market will play a central role in this evolution. The trajectory is set, and the industry is ready to advance.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)