Semiconductor Revenue Hits $319 Billion as Memory Cycles Reshape Industry Patterns

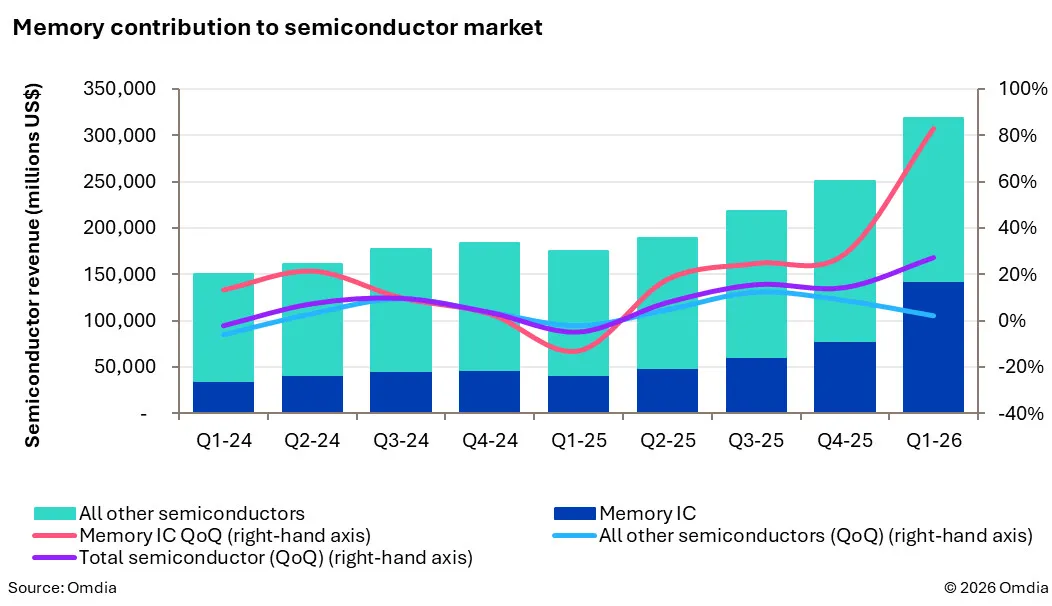

Semiconductor revenue reached three hundred nineteen billion dollars in the first quarter of twenty twenty six, marking a twenty seven percent sequential increase driven primarily by memory chip sales. This surge follows a record setting year and indicates a fundamental shift in traditional market cycles, with lasting implications for manufacturing strategy and global technology supply chains.

The global semiconductor industry recently crossed a significant financial threshold, recording unprecedented quarterly revenue that signals a profound transformation in digital infrastructure. This milestone reflects not merely cyclical growth, but a structural realignment of how computing power is produced, distributed, and consumed across modern economies.

Semiconductor revenue reached three hundred nineteen billion dollars in the first quarter of twenty twenty six, marking a twenty seven percent sequential increase driven primarily by memory chip sales. This surge follows a record setting year and indicates a fundamental shift in traditional market cycles, with lasting implications for manufacturing strategy and global technology supply chains.

Why does the semiconductor market reach this financial milestone?

The achievement of three hundred nineteen billion dollars in quarterly revenue represents a pivotal moment for the hardware sector. This figure emerges from a combination of sustained demand, strategic inventory management, and accelerated production capabilities. The twenty seven percent sequential growth from the previous quarter demonstrates that the industry has moved beyond temporary recovery phases into a period of consistent expansion. Manufacturers have responded to this momentum by optimizing fabrication lines and prioritizing high yield production processes. The financial results underscore the critical role that silicon based components play in modern economic activity.

Every sector that relies on digital processing now depends on the capacity and efficiency of these facilities. The revenue surge also highlights the increasing complexity of modern chip design and the substantial capital required to maintain competitive manufacturing standards. As demand continues to evolve, the financial metrics will likely serve as a benchmark for future industry performance and investment decisions. Companies are recalibrating their operational forecasts to account for this new baseline of economic activity.

How do memory cycles historically dictate industry momentum?

Memory technology has always functioned as the primary indicator of broader semiconductor health. Historically, the industry has operated through predictable cycles of expansion and contraction. During periods of high demand, manufacturers rapidly increase output to capture market share. This surge eventually leads to oversupply, which triggers price corrections and reduced production schedules. The current eighty percent sequential increase in memory revenue breaks from this established rhythm. Traditional forecasting models relied on steady state consumption patterns and gradual inventory adjustments.

The present environment operates under different constraints and expectations. Supply chain resilience has replaced pure cost efficiency as a primary operational goal. Manufacturers are now prioritizing long term reliability over short term margin optimization. This departure from historical patterns suggests that the industry is maturing into a more stable and predictable framework. The implications for future capital allocation and workforce planning will be substantial. Industry analysts are closely monitoring these developments to update long term economic projections.

What structural shifts are altering traditional market patterns?

The deviation from established industry rhythms stems from multiple interconnected factors. Artificial intelligence workloads require specialized memory architectures that differ significantly from conventional computing needs. Data center operators are investing heavily in high bandwidth storage solutions to support machine learning training and inference tasks. This demand pattern does not align with traditional consumer electronics refresh cycles. Instead, it follows the trajectory of enterprise infrastructure modernization. The shift also reflects changes in global trade dynamics and regional manufacturing strategies.

Governments and corporations are increasingly focused on supply chain diversification to mitigate geopolitical risks. Production facilities are being distributed across multiple jurisdictions to ensure continuity. This geographic realignment requires substantial coordination and standardized quality controls. The resulting market structure favors companies that can navigate complex regulatory environments while maintaining technical excellence. The financial results indicate that these strategic adjustments are yielding measurable economic returns. Market participants are adjusting their portfolio allocations to reflect these structural changes.

How will these revenue trends influence future manufacturing and investment?

The current financial performance will inevitably shape long term industry strategy. Capital expenditure decisions will likely prioritize advanced node development and memory technology innovation. Companies will continue to evaluate production capacity against projected demand curves. The focus will remain on achieving sustainable growth rather than pursuing temporary market dominance. Workforce development and technical training programs will expand to support next generation fabrication requirements. Research and development budgets will allocate significant resources to packaging technologies and energy efficient designs.

The industry will also face increasing scrutiny regarding environmental impact and resource consumption. Sustainable manufacturing practices will become a competitive differentiator rather than a compliance requirement. Investors will demand transparent reporting on both financial performance and operational resilience. The market will reward organizations that demonstrate adaptability in the face of technological disruption. Financial institutions are adjusting lending criteria to reflect the elevated importance of semiconductor infrastructure in global commerce.

Consumer electronics manufacturers are simultaneously adapting to these broader industry shifts. Recent developments in mobile hardware design suggest that form factor innovation will continue to drive component demand. Apple left some major folding iPhone hints in the iOS 27 code, indicating that display and memory architectures will require greater flexibility and density. This trend aligns with the broader push toward compact yet powerful computing devices. The underlying silicon must support increased processing loads while maintaining thermal efficiency. Manufacturers are already adjusting production schedules to accommodate these evolving specifications.

The convergence of mobile innovation and data center expansion creates a unified demand landscape. Companies that anticipate these overlapping requirements will maintain a competitive advantage. Software ecosystems and hardware capabilities are becoming increasingly interdependent. The market response to recent artificial intelligence announcements demonstrates how quickly consumer expectations can shift. The market hates Siri AI, so it must be good, reflecting a broader pattern where technological integration drives stock valuation and industry sentiment. This dynamic underscores the importance of seamless hardware software coordination. Memory bandwidth and processing speed directly influence user experience and system responsiveness.

What are the practical implications for global technology supply chains?

The current revenue surge carries significant consequences for international trade and industrial policy. Supply chain managers are reevaluating inventory strategies to balance cost efficiency with operational security. Just in time delivery models are being supplemented by strategic stockpiling of critical components. Logistics networks are adapting to handle increased shipment volumes and complex routing requirements. Port infrastructure and transportation capacity are undergoing expansion to meet growing demand.

The industry is also investing in predictive analytics to anticipate bottlenecks before they materialize. These operational adjustments require substantial coordination across multiple jurisdictions and regulatory frameworks. Companies that successfully navigate these challenges will establish long term competitive advantages. The financial metrics serve as a leading indicator of broader economic health and technological progress. Analysts are using these data points to refine global trade models and assess regional manufacturing viability.

How will the industry navigate the transition from cyclical growth to sustained expansion?

The path forward requires careful calibration of production capacity and technological development. Manufacturers must avoid the pitfalls of overexpansion while meeting escalating demand requirements. Workforce retention and technical expertise will remain critical assets in this transition. Educational institutions and industry partners are collaborating to develop specialized training programs. Research funding will focus on materials science and fabrication efficiency improvements.

The industry will also need to address energy consumption and environmental sustainability at scale. Renewable power integration and waste reduction initiatives will become standard operational practices. Financial institutions are recognizing the long term value of semiconductor infrastructure and adjusting lending criteria accordingly. The market will continue to reward organizations that demonstrate strategic foresight and operational discipline. Stakeholders are preparing for a prolonged period of structural transformation rather than temporary market fluctuations.

The Path Forward

The financial results from the first quarter of twenty twenty six provide a clear snapshot of an industry in transition. The twenty seven percent sequential growth and the dominant role of memory revenue illustrate a sector that has moved beyond traditional cyclical constraints. Manufacturers, suppliers, and technology providers are aligning their strategies to support a more stable and predictable market environment. The shift away from historical patterns reflects broader changes in computing architecture, global trade dynamics, and consumer expectations.

Organizations that prioritize resilience, innovation, and sustainable practices will be positioned to thrive in this evolving landscape. The industry continues to serve as the foundational layer for digital transformation across every major economic sector. Future developments will build upon this momentum, shaping the next generation of computing infrastructure. Market participants are focusing on long term value creation rather than short term earnings volatility. The structural realignment underway will define industry standards for decades to come.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)