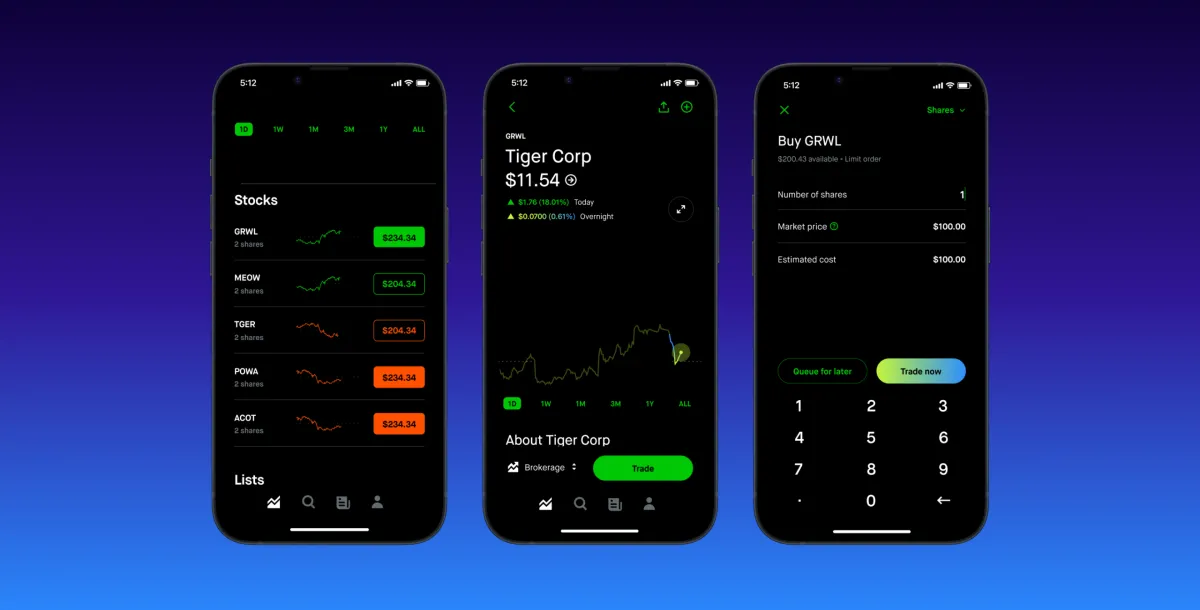

Robinhood Introduces Autonomous Trading And Credit Integration

Robinhood is introducing autonomous financial tools that enable artificial intelligence agents to execute stock trades and manage credit expenditures on behalf of users. This development marks a significant shift toward agentic finance, raising important questions about regulatory oversight and automated wealth management.

The financial technology sector has consistently pursued automation to streamline wealth management and reduce friction in everyday transactions. Retail investors have gradually adapted to algorithmic portfolio rebalancing and automated savings mechanisms over the past decade. The latest development in this trajectory introduces a more direct form of machine-driven capital allocation. Market participants are now observing a structural shift toward systems that can execute complex financial operations without continuous human intervention. This evolution demands careful examination of how autonomous agents interact with traditional brokerage infrastructure and modern credit networks.

What Is the Current State of Autonomous Financial Management?

The concept of agentic finance represents a departure from traditional algorithmic trading platforms that require explicit user commands. Historical fintech applications focused on executing predefined strategies based on market indicators or technical signals. Modern implementations attempt to bridge the gap between passive investment vehicles and active portfolio management by delegating decision-making authority to machine learning models. These systems analyze vast datasets to identify execution opportunities, assess market conditions, and adjust positions in real time. The underlying architecture relies on continuous learning loops that adapt to shifting economic environments. Financial institutions have historically approached automation with caution due to the complexity of capital preservation. The introduction of autonomous agents requires a fundamental reevaluation of how retail investors interact with brokerage platforms. Users must understand that delegating capital allocation introduces new operational dynamics that differ significantly from conventional trading interfaces.

Early computational finance relied on rigid mathematical formulas that triggered trades when specific thresholds were crossed. These systems operated without contextual awareness and could not adjust to sudden market regime changes. The transition to agentic frameworks introduces dynamic reasoning capabilities that process unstructured financial data alongside quantitative metrics. This evolution mirrors broader technological shifts across multiple industries where automation moved from rule-based execution to adaptive problem solving. Financial platforms are now experimenting with natural language interfaces that allow users to express investment objectives in conversational terms. The technology translates these objectives into executable trading parameters while maintaining strict compliance boundaries. Market participants are closely monitoring how these systems handle liquidity constraints and transaction costs. The long-term viability of autonomous finance depends on demonstrating consistent risk-adjusted performance across varying market cycles.

Regulatory bodies are currently developing standardized definitions for machine-driven capital allocation to ensure consistent oversight. Traditional compliance frameworks were designed for human traders who could be held directly accountable for market actions. Delegating execution authority to artificial intelligence requires new legal structures that clarify liability and fiduciary responsibility. Financial institutions must implement robust audit trails to document every automated action taken by these systems. Transparency requirements mandate clear disclosures about how models interpret user parameters and execute trades. The industry is establishing independent testing protocols to evaluate model behavior under extreme market conditions. Consumer protection initiatives focus on ensuring that automated systems prioritize capital preservation over aggressive growth. Educational resources are being expanded to help users comprehend the operational mechanics of agentic finance.

How Do Agentic Systems Approach Market Execution?

Autonomous trading mechanisms operate by interpreting user-defined parameters rather than following rigid programming rules. Traditional quantitative models depend on static mathematical formulas that trigger trades when specific thresholds are crossed. Agentic frameworks utilize natural language processing and contextual reasoning to interpret broader financial objectives. These systems evaluate macroeconomic indicators, sector performance, and individual asset fundamentals to construct execution strategies. The integration of large language models allows these agents to process unstructured data alongside structured market feeds. This capability enables more nuanced decision-making that approximates human analytical processes. The technology draws inspiration from earlier advancements in automated customer service and content curation platforms. For instance, the approach to personalized media delivery shares architectural similarities with how financial agents prioritize asset allocation, much like the Roku platform optimizes content discovery. Companies like Anthropic and OpenAI have contributed to the underlying reasoning capabilities that power these systems. The convergence of predictive analytics and contextual understanding creates a more responsive trading environment.

Market execution algorithms must navigate complex liquidity landscapes while minimizing slippage and transaction costs. Agentic systems continuously monitor order book depth and historical price action to optimize trade placement. These models simulate thousands of execution scenarios to determine the most efficient routing strategy. The technology incorporates real-time news sentiment analysis to adjust positions ahead of major economic announcements. Risk management protocols are embedded directly into the execution layer to prevent excessive exposure. Systems automatically pause trading activity when volatility exceeds predefined thresholds or when liquidity dries up. This proactive approach reduces the likelihood of catastrophic losses during sudden market dislocations. Financial platforms are developing interactive dashboards that allow users to review agent decisions before execution. These tools provide granular control over risk tolerance levels and asset allocation boundaries. The industry is also establishing standardized testing protocols to evaluate model performance under extreme market conditions.

The deployment of autonomous execution systems requires careful consideration of market structure and regulatory compliance. Traditional brokerage models require explicit user authorization for each transaction to maintain compliance standards. Delegating execution authority to machine learning systems introduces novel questions regarding liability and fiduciary responsibility. Regulatory bodies are currently evaluating how existing securities laws apply to algorithmic decision-making that lacks direct human oversight. Financial institutions must implement robust audit trails to document every automated action taken by these agents. Transparency requirements mandate clear disclosures about how models interpret user parameters and execute trades. The industry is developing standardized protocols to ensure that autonomous systems operate within predefined risk boundaries. Compliance frameworks emphasize the importance of maintaining human override capabilities for critical financial operations. These safeguards are designed to protect retail investors from unintended market exposure or system malfunctions.

The Integration of Credit Infrastructure and Investment Automation

The simultaneous deployment of autonomous trading and credit management features signals a broader consolidation of personal finance operations. Historically, brokerage accounts and credit card networks operated as separate financial silos with distinct regulatory requirements. Modern fintech architectures are increasingly designed to treat capital as a unified resource pool. This integration allows machine learning models to optimize liquidity across multiple financial instruments. When an agent executes a trade, it can simultaneously adjust credit utilization ratios to maintain optimal cash flow. The system evaluates interest rates, payment deadlines, and investment returns to determine the most efficient capital deployment strategy. This holistic approach reduces the cognitive load required to manage complex financial portfolios. Users benefit from automated balancing mechanisms that prevent overdrafts while maximizing investment exposure. The convergence of these systems reflects a long-term industry trend toward comprehensive financial operating environments.

Credit card networks have traditionally functioned as short-term borrowing mechanisms with high interest penalties for late payments. Integrating these networks with long-term investment platforms creates new opportunities for automated debt management. Agentic systems can identify high-interest credit balances and automatically allocate investment returns to eliminate them. This process optimizes net worth growth by reducing carrying costs while maintaining investment participation. The technology requires real-time synchronization between banking databases and brokerage accounts to function accurately. Data privacy protocols must ensure that sensitive financial information remains protected during cross-platform transfers. Financial institutions are developing secure APIs that enable seamless communication between credit processors and trading engines. These connections allow agents to execute trades without disrupting credit payment schedules. The integration also enables automated reward optimization that maximizes cashback and points accumulation. Users gain a unified view of their financial health without switching between multiple applications.

The consolidation of credit and investment management raises important questions about systemic risk and consumer vulnerability. When a single platform controls both borrowing and investing, users may face concentrated exposure to platform failures. Regulatory frameworks are being updated to address the unique risks posed by integrated financial ecosystems. Institutions must implement strict data segregation protocols to prevent cross-contamination of credit and investment data. Risk management teams are developing stress testing scenarios that simulate simultaneous market downturns and credit crunches. Consumer protection agencies are reviewing terms of service to ensure that automated credit adjustments remain transparent. Financial literacy programs are expanding to help users understand the implications of integrated capital management. The industry must balance convenience with robust safeguards to maintain trust in automated financial systems.

What Regulatory Frameworks Govern AI-Driven Capital Allocation?

The expansion of autonomous financial tools operates within a complex landscape of securities regulations and consumer protection laws. Traditional brokerage models require explicit user authorization for each transaction to maintain compliance standards. Delegating execution authority to machine learning systems introduces novel questions regarding liability and fiduciary responsibility. Regulatory bodies are currently evaluating how existing securities laws apply to algorithmic decision-making that lacks direct human oversight. Financial institutions must implement robust audit trails to document every automated action taken by these agents. Transparency requirements mandate clear disclosures about how models interpret user parameters and execute trades. The industry is developing standardized protocols to ensure that autonomous systems operate within predefined risk boundaries. Compliance frameworks emphasize the importance of maintaining human override capabilities for critical financial operations. These safeguards are designed to protect retail investors from unintended market exposure or system malfunctions.

International regulatory bodies are collaborating to establish consistent standards for machine-driven financial management. Divergent national approaches could create compliance fragmentation that hinders the global adoption of agentic finance. Harmonized frameworks would provide clear guidelines for model validation, data governance, and consumer recourse. Financial institutions are investing heavily in compliance technology to meet evolving regulatory expectations. Automated monitoring systems track every agent action to ensure alignment with jurisdictional requirements. Risk assessment models are being updated to account for algorithmic bias and systemic feedback loops. Regulatory sandboxes are allowing controlled testing of autonomous finance features under supervised conditions. These initiatives help policymakers understand the practical implications of widespread agentic adoption. The goal is to foster innovation while maintaining market integrity and investor confidence.

The legal classification of autonomous financial agents remains a subject of ongoing debate among policymakers and industry experts. Some jurisdictions treat these systems as extensions of human traders subject to existing brokerage regulations. Others propose new legal categories that specifically address machine-driven decision-making and liability allocation. Clear legal definitions are necessary to determine responsibility when automated systems execute erroneous trades. Financial platforms are working with legal counsel to structure user agreements that clarify the scope of agent authority. Dispute resolution mechanisms are being developed to handle conflicts arising from autonomous financial operations. Industry associations are publishing best practice guidelines to promote responsible deployment of agentic technologies. These efforts aim to create a predictable regulatory environment that supports sustainable innovation. Market participants require certainty to invest in long-term financial automation infrastructure.

Navigating Risk and Consumer Protection in Automated Finance

The deployment of agentic systems requires careful consideration of risk management principles and user education. Financial automation introduces new vulnerabilities related to data privacy, model bias, and system reliability. Users must understand that machine learning models can produce unexpected outcomes when processing ambiguous financial instructions. Risk mitigation strategies include implementing daily transaction limits, mandatory cooling-off periods, and continuous monitoring dashboards. Financial platforms are developing interactive interfaces that allow users to review agent decisions before execution. These tools provide granular control over risk tolerance levels and asset allocation boundaries. The industry is also establishing standardized testing protocols to evaluate model performance under extreme market conditions. Consumer protection initiatives focus on ensuring that automated systems prioritize capital preservation over aggressive growth. Educational resources are being expanded to help users comprehend the operational mechanics of agentic finance.

Model validation processes are critical to ensuring that autonomous agents behave predictably across diverse market environments. Independent auditors are being engaged to test algorithmic decision-making against historical market data and stress scenarios. These evaluations identify potential weaknesses in logic pathways that could lead to unintended financial consequences. Financial institutions are implementing version control systems to track changes in agent behavior over time. Rollback procedures allow platforms to revert to previous model iterations if performance degrades unexpectedly. User feedback mechanisms help refine agent parameters to better align with individual financial goals. The industry is developing certification programs for autonomous finance developers to establish professional standards. These initiatives promote accountability and continuous improvement in agentic system design. Market stability depends on rigorous testing and transparent operational practices.

Consumer education remains a cornerstone of successful autonomous finance adoption. Users must develop new financial literacy skills to navigate automated investment environments effectively. Platforms are creating interactive tutorials that explain how agents interpret instructions and execute trades. These resources help users set appropriate expectations and understand the limitations of machine-driven management. Financial advisors are being trained to integrate agentic tools into traditional wealth management practices. This hybrid approach combines human expertise with algorithmic efficiency to optimize client outcomes. Regulatory agencies are funding public awareness campaigns to highlight the benefits and risks of automated finance. The goal is to empower users to make informed decisions about delegating financial control. Trust in autonomous systems will grow as transparency and reliability improve over time.

The Future of Automated Wealth Management

The trajectory of financial technology points toward increasingly sophisticated systems that bridge the gap between human intuition and machine precision. Autonomous agents will likely evolve to handle more complex financial planning tasks beyond basic portfolio management. The integration of predictive analytics and contextual reasoning will continue to reshape how retail investors approach capital allocation. Financial institutions must balance innovation with rigorous oversight to maintain market stability and consumer trust. The success of these systems will depend on their ability to operate transparently within established regulatory frameworks. Users will need to develop new financial literacy skills to navigate automated investment environments effectively. The ongoing refinement of agentic finance will determine whether autonomous capital management becomes a standard utility or remains a specialized tool. Market participants will continue to monitor how these technologies interact with traditional economic structures.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)