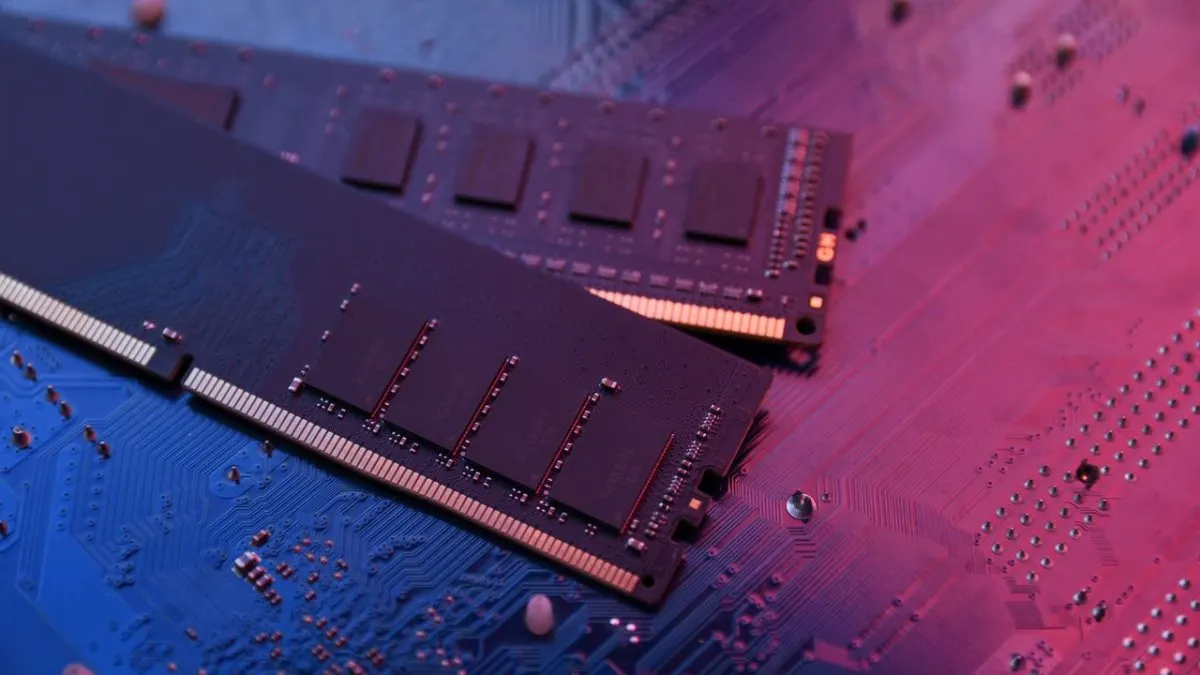

SK Group Chairman Warns RAM Shortage Could Last Until 2030

SK Group chairman Chey Tae-won forecasts that the global RAM shortage will extend through 2030, citing a necessary four-to-five-year timeline for wafer production expansion and an anticipated twenty percent deficit. The prolonged crisis stems from AI-driven high-bandwidth memory demand skewing manufacturing priorities, with significant downstream implications for consumer electronics and enterprise infrastructure.

The global semiconductor industry is navigating a complex period of structural realignment, driven by unprecedented computational demands and the physical realities of advanced manufacturing. A recent assessment from a leading memory chip manufacturer suggests that the current constraints on random access memory will persist well beyond initial market expectations, fundamentally altering production timelines and pricing structures for the remainder of the decade.

What is driving the prolonged RAM supply shortage?

The chairman of SK Group, Chey Tae-won, recently outlined a timeline that diverges sharply from optimistic market projections. According to his assessment, the semiconductor industry requires a minimum of four to five years to restore adequate wafer production capacity. Wafers serve as the foundational substrate upon which integrated circuits are fabricated, and their manufacturing process involves extreme precision, multi-year equipment lead times, and massive capital deployment. The expectation of maintaining more than a twenty percent shortage of these critical substrates indicates that demand is currently outpacing the physical ability to scale fabrication facilities.

Semiconductor fabrication is not a linear process that can be rapidly accelerated. Cleanroom construction, lithography machine procurement, and process validation require extensive coordination across global supply chains. When demand surges, the industry cannot simply increase output immediately. Instead, manufacturers must plan capacity expansions years in advance, accounting for yield rates, material availability, and technological node transitions. The physical constraints of building fabrication plants mean that production increases lag significantly behind market signals.

Memory chip manufacturing operates within a tightly regulated economic framework that dictates the pace of technological advancement. Building a modern fabrication facility requires billions of dollars in capital expenditure, alongside years of engineering development to optimize process nodes. The industry has historically experienced cyclical patterns of oversupply and shortage, but the current environment differs due to the structural demands of modern computing. Artificial intelligence infrastructure requires continuous, massive upgrades to memory capacity and bandwidth, creating a sustained floor for production allocation.

Why does high-bandwidth memory dominate semiconductor priorities?

The structural imbalance in the memory market is heavily influenced by the rapid expansion of artificial intelligence workloads. High-bandwidth memory, commonly referred to as HBM, has emerged as a critical component for training and deploying large language models. This specialized memory architecture stacks multiple dynamic random access memory dies vertically, requiring complex manufacturing techniques and significantly more wafer space per chip compared to traditional memory modules. SK Hynix, which operates as a primary division within the SK Group, currently holds a dominant position in supplying this specialized memory to major artificial intelligence hardware manufacturers.

The financial dynamics of semiconductor manufacturing naturally guide corporate strategy. Producing high-bandwidth memory for artificial intelligence applications generates substantially higher profit margins than manufacturing standard consumer random access memory. Consequently, manufacturing lines are increasingly allocated toward high-margin products, leaving conventional memory production constrained. This reallocation creates a secondary shortage in the consumer sector, where desktop computers, laptops, and mobile devices rely on standard memory modules. The global memory market consists of three primary manufacturers, and their collective strategic decisions directly influence global supply availability.

When the industry collectively prioritizes one segment, the other inevitably experiences reduced output. Manufacturers must balance long-term infrastructure investments with immediate market requirements, a process that inherently stretches timeline expectations. The intersection of artificial intelligence advancement and semiconductor manufacturing capacity will remain a defining factor in global technology development. As computational demands continue to escalate, the allocation of wafer space will determine which product categories receive priority access. This dynamic necessitates careful coordination across multiple sectors to maintain equilibrium.

The economics of semiconductor fabrication

Semiconductor manufacturing operates on a foundation of immense financial commitment and technical complexity. Memory chip production is particularly sensitive to yield rates, which measure the percentage of functional chips produced on each wafer. When manufacturers shift production lines toward advanced architectures, they must retrain workforces, recalibrate equipment, and undergo rigorous testing phases. These operational realities mean that capacity expansion cannot be rushed without compromising quality or incurring unsustainable costs. The industry must navigate these uncertainties while maintaining investment in next-generation technologies.

Historical memory market cycles demonstrate that recovery periods are rarely uniform. Supply restoration depends on multiple variables, including equipment availability, raw material procurement, and global economic conditions. Manufacturers must account for extended production timelines when evaluating future product roadmaps and investment strategies. Market participants who adapt their operational models to account for prolonged constraints will likely maintain stronger competitive positioning. The technology sector has consistently demonstrated resilience in the face of component shortages, relying on innovation and strategic planning to restore equilibrium.

Consumer electronics and downstream supply chain effects

The reallocation of manufacturing capacity toward artificial intelligence components has direct consequences for the consumer electronics sector. Hardware manufacturers that produce personal computers, gaming rigs, and mobile devices must now compete for a constrained supply of standard memory modules. This competition drives up component costs and forces supply chain adjustments that ripple across the broader technology market. Industry observers note that certain hardware manufacturers consider the upcoming fiscal period particularly difficult, citing the compounding effects of memory constraints on budget-conscious product lines. For context on how these constraints affect modern hardware ecosystems, readers may explore the broader implications of memory scarcity on emerging computing platforms.

When component costs rise, manufacturers face difficult decisions regarding pricing, feature allocation, and production volumes. The gaming hardware segment, which historically relies on high-performance memory configurations, is particularly sensitive to these fluctuations. System integrators and original equipment manufacturers must adjust their procurement strategies well in advance to secure adequate inventory. This proactive sourcing increases operational complexity and reduces flexibility, making it difficult to respond quickly to shifting consumer demand. The downstream impact extends beyond individual product lines, influencing broader market dynamics and consumer purchasing behavior.

Hardware manufacturers are exploring alternative memory technologies and packaging methods that maximize performance within constrained production environments. The consumer market will experience prolonged pricing pressure, potentially influencing upgrade cycles and product segmentation strategies. As artificial intelligence continues to integrate into broader computing applications, the demand for specialized memory will remain a dominant force in semiconductor manufacturing. This dynamic will continue to shape investment patterns, research priorities, and global supply chain strategies.

How will the industry navigate the next five years?

Industry leaders are actively developing strategies to address the persistent supply imbalance. SK Hynix has indicated that management is formulating plans aimed at stabilizing memory pricing structures, with official details expected from executive leadership in the near future. Stabilization efforts typically involve coordinated production scheduling, long-term customer contracts, and targeted capacity expansion in specific memory categories. However, external factors continue to complicate these efforts. Geopolitical tensions in key energy-producing regions introduce volatility into global shipping and manufacturing costs, directly affecting the economic viability of semiconductor production.

Energy consumption remains a critical variable in chip fabrication, and fluctuating power prices can impact operational budgets and regional manufacturing competitiveness. The industry must balance immediate market demands with long-term technological advancement, a process that requires careful coordination across multiple sectors. Market participants who adapt their operational models to account for extended supply constraints will likely maintain stronger competitive positioning. The technology sector has consistently demonstrated resilience in the face of component shortages, relying on innovation, strategic planning, and market realignment to restore equilibrium.

Historical precedent suggests that memory market cycles eventually normalize, but the current structural shift requires a more extended adaptation period. Manufacturers must navigate these uncertainties while maintaining investment in next-generation technologies. The industry has historically adapted to similar constraints through strategic planning and market realignment, but the current technological shift requires a more extended adaptation period. Market participants who adapt their operational models to account for extended supply constraints will likely maintain stronger competitive positioning.

What does this mean for the broader technology landscape?

The prolonged constraint on memory supply will likely accelerate structural shifts across the technology sector. Enterprises and software developers are already adjusting their architectural approaches to optimize memory efficiency, reducing reliance on excessive component allocation. Hardware manufacturers are exploring alternative memory technologies and packaging methods that maximize performance within constrained production environments. The consumer market will experience prolonged pricing pressure, potentially influencing upgrade cycles and product segmentation strategies.

As artificial intelligence continues to integrate into broader computing applications, the demand for specialized memory will remain a dominant force in semiconductor manufacturing. This dynamic will continue to shape investment patterns, research priorities, and global supply chain strategies. The industry must balance immediate market demands with long-term technological advancement, a process that requires careful coordination across multiple sectors. Market participants who adapt their operational models to account for extended supply constraints will likely maintain stronger competitive positioning.

The intersection of artificial intelligence advancement and semiconductor manufacturing capacity will remain a defining factor in global technology development. Market participants must account for extended production timelines when evaluating future product roadmaps and investment strategies. The technology sector has consistently demonstrated resilience in the face of component shortages, relying on innovation, strategic planning, and market realignment to restore equilibrium. The semiconductor industry operates within a tightly regulated physical and economic framework that dictates the pace of technological advancement.

Concluding outlook on memory market dynamics

Current production constraints reflect fundamental limitations in wafer fabrication capacity rather than temporary market imbalances. Manufacturers are adjusting their strategic priorities to accommodate sustained demand while developing mechanisms to stabilize pricing and restore supply equilibrium. The technology sector will continue to evolve through adaptation, innovation, and coordinated industry planning. Market participants must account for extended production timelines when evaluating future product roadmaps and investment strategies. The intersection of artificial intelligence advancement and semiconductor manufacturing capacity will remain a defining factor in global technology development for the foreseeable future.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)