Trump Accounts App Launches Thursday for iOS and Android

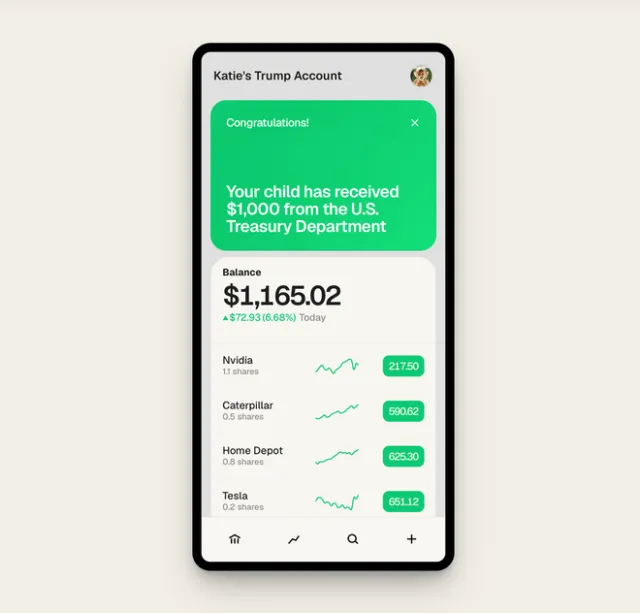

The Trump Accounts app launches Thursday on iOS and Android, enabling parents to manage tax-advantaged custodial investment accounts for their children. Built by Bank of New York Mellon and Robinhood, the platform provides financial literacy tools ahead of July 2026 federal seed funding. Eligible U.S. citizen children born between 2025 and 2028 can receive $1,000 in government contributions.

The intersection of federal policy and personal finance has produced a new mechanism for intergenerational wealth building. A recently enacted legislative framework introduces tax-advantaged investment structures designed specifically for minors, supported by a dedicated mobile application launching this week. This development marks a significant shift in how families can approach early financial planning, combining government incentives with established brokerage infrastructure.

What Is the Trump Accounts Initiative?

The legislative framework establishes a unique category of custodial investment vehicles designed specifically for minors. These accounts operate with structural similarities to traditional individual retirement arrangements, though they are explicitly tailored for younger beneficiaries. The primary objective centers on providing a tax-deferred environment where capital can compound over decades without immediate fiscal friction. This structure encourages disciplined saving habits from an early age.

Families can direct these funds toward low-cost index products, which historically offer steady long-term growth. The structure remains restricted until the beneficiary reaches adulthood, at which point the account transitions to a standard custodial arrangement. This design ensures that the capital serves its intended purpose of funding education, homeownership, or retirement preparation. The legislative foundation was formalized on Independence Day in 2025, establishing a clear timeline for implementation and public awareness.

How Does the New Mobile Application Function?

The application serves as both a monitoring dashboard and an educational resource. Parents and legal guardians can track portfolio performance, review transaction histories, and adjust investment allocations within the allowed parameters. Beyond basic account oversight, the platform integrates comprehensive financial literacy materials designed to help younger beneficiaries understand market dynamics. These resources aim to bridge the gap between abstract financial concepts and practical money management skills. The software architecture prioritizes security and regulatory compliance, ensuring that sensitive family data remains protected. Early access is available to families who have already completed enrollment procedures, allowing them to activate accounts immediately. New participants must register through the official government portal to establish eligibility and verify documentation before gaining full platform access.

Who Qualifies for Federal Seed Funding?

Eligibility for the initial government contribution follows a precise set of demographic and legal criteria. The federal seed money program targets children born between January first, 2025, and December thirty-first, 2028. Participants must hold valid United States citizenship and possess an active Social Security number. The program permits only one account per eligible child, preventing duplicate claims or overlapping benefits.

Parents, legal guardians, or specific adult relatives hold the authority to open and manage these accounts. The priority order for account management places parents and guardians first, followed by adult siblings, and then grandparents. This hierarchy ensures that the primary caretakers retain control over financial decisions during the child's minority. The seed contribution itself amounts to one thousand dollars, deposited directly into the account upon official opening. Additional funding is entirely optional, allowing external contributors to supplement the initial government allocation. The annual contribution limit stands at five thousand dollars per child, providing substantial room for family involvement without overwhelming the account structure.

What Are the Long-Term Financial Implications?

The structural design of these accounts emphasizes patience and compounding growth over immediate liquidity. Because the funds remain restricted until the beneficiary approaches adulthood, the portfolio benefits from extended market exposure. Tax deferral plays a crucial role in this process, allowing gains to reinvest without annual withdrawal penalties or income tax obligations. This mechanism mirrors traditional retirement accounts, though the timeline is significantly compressed due to the younger starting age.

Over a typical eighteen-year horizon, even modest annual returns can generate substantial capital through the power of exponential growth. The restriction also serves as a behavioral safeguard, discouraging impulsive spending during formative years. When the account transitions to a standard custodial format after the beneficiary turns eighteen, the funds can be deployed for higher education expenses, real estate down payments, or long-term retirement planning. Financial advisors often recommend low-cost index funds for this purpose, as they provide broad market exposure with minimal management fees. The program effectively removes the traditional barrier of initial capital, allowing families to begin building wealth without substantial upfront investment. This approach democratizes access to institutional-grade investment vehicles, which were previously reserved for high-net-worth households.

How Should Families Approach Enrollment and Management?

Navigating the registration process requires attention to specific documentation and procedural deadlines. Eligible families must complete Internal Revenue Service Form four five four seven during their annual tax filing, or utilize the dedicated online portal at TrumpAccounts.gov. The digital registration system verifies citizenship status, Social Security numbers, and birth dates to confirm eligibility. Once approved, the account becomes active, though actual funding will not commence until July fourth, 2026.

This interim period allows families to familiarize themselves with the platform, review investment options, and establish contribution strategies. Parents should consider their long-term financial goals when selecting initial allocations, as early decisions set the trajectory for future growth. Regular monitoring through the mobile application helps maintain alignment with risk tolerance and market conditions. Families intending to make additional contributions should track the five thousand dollar annual limit to avoid tax complications. The optional nature of supplementary deposits means that participation remains accessible regardless of current economic circumstances. Financial literacy resources within the app can guide younger beneficiaries through basic portfolio management concepts. Consistent engagement with the platform ensures that families maximize the benefits of the tax-advantaged structure.

Historical Context and Program Design

The historical precedent for government-backed youth investment accounts traces back to earlier educational savings frameworks. Those earlier models focused primarily on tuition offsets rather than broad market participation. This new initiative expands the scope by integrating direct equity exposure into the custodial structure. The shift reflects a broader policy trend toward early financial empowerment. By removing traditional entry barriers, the program encourages families to view investing as a routine household activity rather than a specialized financial exercise. This approach fundamentally changes how wealth is accumulated across generations.

Security and Administrative Oversight

Security protocols within the application adhere to strict financial industry standards. Multi-factor authentication and encrypted data transmission protect sensitive account information from unauthorized access. The platform also implements real-time fraud detection algorithms to flag unusual transaction patterns. These measures are essential for maintaining trust in a system that handles family wealth. User interface design prioritizes clarity, ensuring that complex financial data remains accessible to non-expert users. The development team has structured the navigation flow to minimize cognitive load during routine account maintenance. Regular software updates will introduce new features based on user feedback and regulatory requirements.

The demographic targeting of the seed funding program reflects deliberate policy calculations. Focusing on children born within a specific four-year window allows the government to manage fiscal outlays efficiently. This staggered approach prevents immediate budgetary strain while ensuring steady program growth. The requirement for a valid Social Security number ties the initiative to existing federal tracking systems. This integration simplifies verification processes and reduces administrative overhead. Families outside the eligible birth window can still benefit from the broader account structure, though they will not receive the initial government allocation. The program design acknowledges that wealth building is a gradual process requiring consistent participation.

Economic historians note that early capital formation significantly influences long-term financial stability. Children who enter adulthood with established investment portfolios face fewer barriers to major life milestones. The tax-deferred structure amplifies this advantage by allowing compounding to operate without annual interruption. Market volatility remains a consideration, though the long time horizon typically smooths short-term fluctuations. Financial educators emphasize that consistent contributions matter more than perfect market timing. The program encourages families to adopt a disciplined approach to regular investing. This mindset shift can produce lasting behavioral changes that extend beyond the account itself.

Administrative oversight ensures that the program maintains its intended fiscal parameters. The Treasury Department monitors account activity to prevent misuse or premature withdrawals. Compliance mechanisms are built into both the digital platform and the underlying brokerage infrastructure. Families must adhere to contribution limits to preserve the tax-advantaged status of the accounts. The system automatically tracks cumulative deposits to prevent accidental overfunding. Regular statements provide transparent reporting on account performance and fee structures. This transparency supports informed decision-making and builds confidence in the platform. Families who engage proactively will find the management process straightforward and efficient.

Conclusion

The introduction of a dedicated mobile platform for managing these custodial accounts marks a practical step toward broader financial inclusion. By combining legislative incentives with accessible technology, the program lowers traditional barriers to early investing. Families who engage with the system now will be positioned to capitalize on the upcoming funding cycle. The emphasis on long-term growth and financial education aligns with established principles of intergenerational wealth preservation. As the launch date approaches, stakeholders across the financial sector will monitor adoption rates and portfolio performance. The success of this initiative will likely influence future discussions regarding youth financial literacy and public investment programs. This structured approach to childhood wealth building represents a significant evolution in personal finance policy.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)