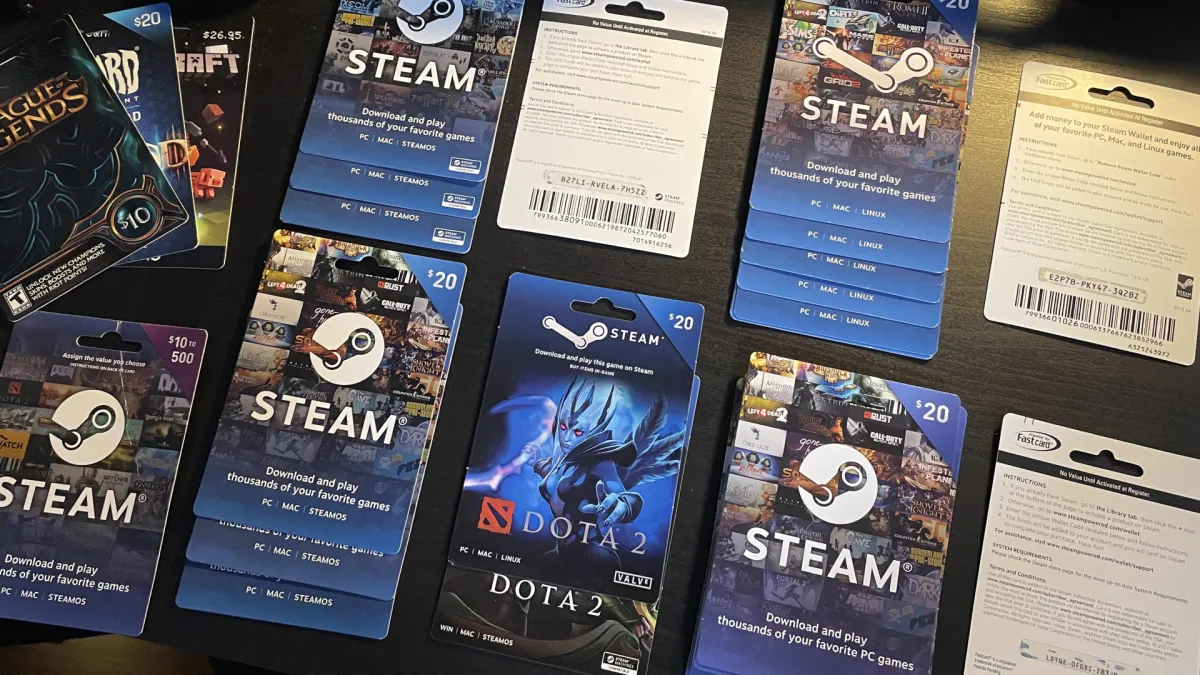

Valve Ends Physical Steam Gift Cards Amid Rising Fraud

Valve is permanently ending the sale of physical Steam gift cards at retail stores due to persistent and escalating fraud. While existing inventory will remain valid until depleted, consumers must now rely exclusively on digital distribution channels. This strategic pivot aims to curb money laundering and protect users from coercion-based theft, fundamentally altering how digital store credit is purchased and gifted.

The digital marketplace has long relied on the tangible convenience of physical gift cards, yet that very convenience has become a liability for major gaming platforms. Valve has officially announced the discontinuation of physical Steam gift cards at retail locations, citing an unsustainable surge in fraudulent activity. This policy shift marks a definitive turning point in how digital currency is distributed within the gaming industry. The decision reflects a broader industry reckoning with the vulnerabilities inherent in untracked payment methods. As scammers adapt to new security measures, platforms are forced to choose between consumer convenience and systemic protection.

Valve is permanently ending the sale of physical Steam gift cards at retail stores due to persistent and escalating fraud. While existing inventory will remain valid until depleted, consumers must now rely exclusively on digital distribution channels. This strategic pivot aims to curb money laundering and protect users from coercion-based theft, fundamentally altering how digital store credit is purchased and gifted.

What drives the widespread reliance on physical gift cards for fraudulent purposes?

Physical gift cards have historically served as a bridge between traditional retail commerce and digital economies. Their appeal lies in their anonymity and immediate liquidity. When a purchaser buys a card at a grocery store or convenience shop, the transaction leaves a minimal digital footprint. Criminal organizations quickly recognized that these cards function as a highly efficient vehicle for money laundering. The process requires minimal technical expertise and operates entirely outside traditional banking oversight.

Scammers instruct victims to purchase specific denominations and transmit the redemption codes through unsecured communication channels. Once the code is entered into a compromised account, the funds can be rapidly converted into cryptocurrency or used to purchase high-value digital goods that can be resold. The Federal Trade Commission estimates that this specific method of theft facilitates over one hundred million dollars in annual losses across the United States. The lack of transactional documentation makes recovery nearly impossible for law enforcement agencies. Criminal networks exploit these gaps with remarkable precision.

Consequently, major brands have found themselves trapped in a cycle of loss prevention that increasingly favors the perpetrator. The anonymity of physical retail purchases allows fraudsters to operate with remarkable speed and efficiency. Every new restriction prompts immediate adaptation from criminal networks. The industry has witnessed countless attempts to combat this threat, yet the fundamental nature of bearer instruments makes them inherently vulnerable to exploitation. Platforms must now accept that convenience cannot outweigh systemic risk.

How does the removal of physical inventory change the mechanics of digital commerce?

The removal of retail inventory forces a complete transition toward account-linked digital transactions. Digital distribution requires both the purchaser and the recipient to maintain verified accounts within the platform ecosystem. This structural change introduces friction into the gifting process, but it also establishes a critical layer of accountability. When a digital card is purchased online, the transaction is logged, tracked, and tied to a specific payment method.

Scammers can no longer exploit the anonymity of physical retail purchases to launder stolen funds. The shift also impacts how consumers approach digital gifting. Friends and family members must now navigate online storefronts rather than visiting local retailers. While this requires additional steps, it significantly reduces the risk of interception during transit or theft from store shelves. The gaming industry has witnessed similar transitions across multiple sectors.

Digital wallets and platform-specific credits have gradually replaced physical vouchers in many commercial spaces. This evolution mirrors broader trends in software licensing and subscription management, where direct account integration has become the standard for security and compliance. Users benefit from automated purchase histories and easier refund processing. The trade-off involves surrendering the cash-like flexibility that physical cards once provided. Security protocols now dictate the architecture of digital commerce. This structural shift ensures that every transaction leaves an auditable trail, reducing opportunities for illicit activity.

The historical context of platform security and consumer protection

Platform operators have long struggled to balance user convenience with fraud prevention. Digital storefronts initially embraced physical gift cards to lower the barrier to entry for new customers. Many users lacked access to credit cards or preferred not to link financial information to gaming accounts. The physical card served as a practical workaround, allowing cash-based transactions to convert directly into digital currency.

However, the convenience quickly attracted organized crime networks. Fraudsters adapted by targeting retail environments, stealing inventory, or coercing victims into purchasing cards under false pretenses. Platform developers responded by implementing various restrictions, including purchase limits, regional blocks, and enhanced verification protocols. Despite these measures, the fraud ecosystem proved remarkably resilient. Criminal groups continuously developed new methods to bypass security checks and monetize stolen codes.

The cumulative financial impact forced executives to reconsider the viability of the physical distribution model. The decision to terminate the retail program represents a calculated risk, prioritizing long-term platform integrity over short-term revenue from card sales. This approach aligns with broader industry efforts to sanitize digital marketplaces, similar to how macOS Golden Gate could finally unlock the shackles holding back my Mac by enforcing stricter code signing and runtime verification policies. Companies that successfully navigate this transition will likely establish new standards for digital commerce security.

The practical implications for consumers and the gaming ecosystem

Consumers will experience a noticeable shift in how they acquire and manage digital store credit. The immediate effect is the gradual disappearance of physical cards from retail shelves. Existing inventory will remain valid for redemption, but new purchases must occur through official digital channels. This transition requires users to maintain active accounts and link valid payment methods to their profiles.

For many, this represents a necessary evolution in digital security. The removal of physical cards also impacts the secondary market for gaming credits. Discounted codes and unauthorized resellers have historically thrived on the arbitrage between physical retail prices and digital redemption values. Without physical inventory to exploit, these gray market operations will face significant disruption. Users seeking reliable digital services often explore alternatives like Ditch your $20/month ChatGPT fee, as centralized platforms increasingly demand transparent billing practices.

The gaming industry has seen similar disruptions in other sectors, where centralized digital distribution has replaced fragmented physical markets. Users will need to adapt to new purchasing habits, relying on official storefronts and platform-native payment systems. This shift may also influence how digital gifts are perceived, moving away from tangible objects toward purely digital transactions. The long-term outcome depends on effective enforcement.

The broader economic and regulatory landscape of digital currency fraud

Regulatory bodies and financial institutions have increasingly scrutinized the role of gift cards in modern fraud schemes. Law enforcement agencies recognize that these instruments function as unregulated cash equivalents, enabling rapid cross-border money movement. The lack of consumer protections makes gift card fraud particularly lucrative for criminal enterprises. In response, governments have proposed stricter regulations on retail sales. Legislators are pushing for mandatory reporting thresholds and enhanced merchant accountability to close existing loopholes.

Mandatory purchase logs and age verification requirements aim to create accountability where none previously existed. Technology companies face mounting pressure to implement proactive fraud detection systems. Valve's decision to eliminate physical cards reflects a growing consensus that passive security measures are insufficient. The platform must now rely on continuous monitoring, machine learning algorithms, and account behavior analysis to prevent abuse. Advanced threat intelligence sharing between industry participants will become essential.

This approach requires substantial investment in security infrastructure and customer support resources. The financial burden of fraud prevention will inevitably be absorbed by the platform, potentially affecting pricing models and service offerings. However, the alternative of tolerating widespread theft would undermine trust in the ecosystem. The gaming industry operates on a foundation of consumer confidence. Companies that successfully navigate this transition will likely establish new standards for digital commerce security.

Conclusion

The termination of physical Steam gift cards marks a definitive shift in how digital currency is managed within the gaming industry. The decision prioritizes systemic security over retail convenience, acknowledging that untracked payment methods have become a liability rather than an asset. Consumers will need to adapt to digital-only distribution channels, accepting additional verification steps as a necessary trade-off for fraud prevention.

The gaming ecosystem will experience reduced secondary market activity and increased reliance on platform-native payment systems. This transition reflects a broader industry movement toward accountable digital commerce, where security protocols and user verification replace the anonymity of physical transactions. The long-term success of this strategy will depend on sustained enforcement and continuous adaptation to emerging fraud techniques. Industry stakeholders must remain vigilant against evolving criminal methodologies.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)