Navigating Streaming Subscriptions: Direct vs Marketplace Billing

Streaming marketplaces consolidate billing but frequently restrict content access and limit promotional offers. Direct subscriptions through official service websites consistently deliver superior pricing, broader device compatibility, and clearer financial management. Consumers should carefully evaluate platform restrictions and bundle availability before committing to any third-party payment systems.

The modern television landscape has shifted dramatically from traditional cable packages to a fragmented ecosystem of digital streaming services. Consumers now navigate a complex network of monthly billing cycles, promotional tiers, and platform-specific access rules. In response to this fragmentation, major technology companies have introduced subscription marketplaces designed to centralize payments and content discovery. These platforms promise simplified management and consolidated billing, yet they often introduce hidden complexities that disadvantage the average viewer. Understanding the structural differences between direct subscriptions and third-party marketplaces remains essential for maintaining financial control and content flexibility.

Streaming marketplaces consolidate billing but frequently restrict content access and limit promotional offers. Direct subscriptions through official service websites consistently deliver superior pricing, broader device compatibility, and clearer financial management. Consumers should carefully evaluate platform restrictions and bundle availability before committing to any third-party payment systems.

What is the current landscape of streaming subscription marketplaces?

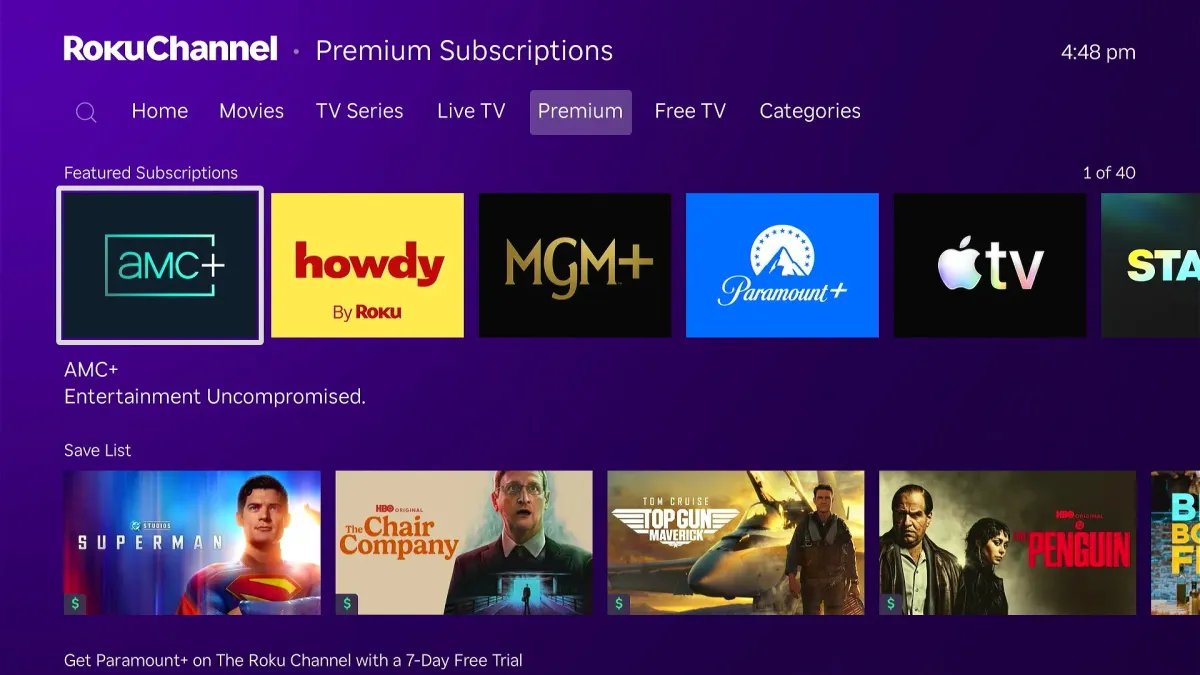

Third-party subscription marketplaces have emerged as centralized hubs for digital entertainment billing. Platforms operated by Roku, Amazon, YouTube, and Apple now aggregate access to numerous streaming catalogs under a single payment umbrella. Roku Premium Subscriptions function through the Roku Channel, while Amazon Prime Video Channels operate within the Prime Video ecosystem. YouTube Primetime Channels and Apple TV Channels follow similar consolidation models. These systems allow users to link multiple service accounts to a unified billing interface.

The underlying premise suggests that managing subscriptions through a single dashboard reduces administrative friction. However, the architecture of these marketplaces often prioritizes platform retention over consumer flexibility. Viewers frequently encounter restricted access pathways that tie their purchased content strictly to the marketplace application. This structural design creates a dependency loop where the platform controls both the transaction and the delivery mechanism. The consolidation trend reflects a broader industry shift toward ecosystem lock-in rather than open content distribution.

Why do direct subscriptions consistently offer superior financial advantages?

Financial efficiency remains the primary argument for bypassing third-party marketplaces. Streaming providers routinely reserve their most aggressive promotional pricing for direct channels. Free trial periods, introductory monthly rates, and holiday sales are typically exclusive to official websites and native applications. Marketplaces generally lack the authority to replicate these limited-time offers. Consumers who rely solely on third-party platforms often miss out on significant savings opportunities. Direct subscriptions also unlock specialized bundle configurations that marketplaces cannot replicate.

Industry partners frequently negotiate cross-platform discounts that require direct enrollment to activate. These arrangements often combine major streaming catalogs with sports networks or ad-supported tiers at substantially reduced rates. Third-party aggregators usually sell services at standard retail pricing or offer narrower bundle combinations. The financial gap widens when comparing ad-supported versus ad-free tiers. Official channels frequently provide discounted streaming options that bypass marketplace markup structures. Maintaining direct relationships with content providers ensures access to the full spectrum of available pricing models. This principle mirrors the approach used when evaluating comprehensive device updates, where direct access to official channels consistently yields better results.

The practical limitations of platform-locked content access

Content accessibility represents another critical differentiator between direct and marketplace subscriptions. Many third-party platforms enforce strict viewing boundaries that limit where purchased content can be accessed. Subscribers who enroll through certain marketplaces must utilize the platform application to stream their purchased material. This restriction eliminates the ability to use native service applications on alternative devices. Roku Premium Subscriptions exemplify this limitation by confining access exclusively to the Roku Channel interface. Viewers cannot seamlessly transition their subscriptions to competing streaming ecosystems.

Amazon occasionally permits account linking with select providers, yet this functionality remains inconsistent across the catalog. The inability to use preferred applications disrupts user experience and device integration. Many viewers prioritize specific interface designs, search algorithms, or home screen organization when selecting streaming platforms. Marketplace restrictions force content consumption into predetermined digital environments. This limitation reduces consumer choice and complicates device switching scenarios. The technical architecture of these marketplaces deliberately channels usage toward the aggregator rather than the content creator.

How does consolidated billing impact consumer control and transparency?

The promise of simplified billing often masks underlying administrative complexities. Third-party marketplaces claim to streamline subscription management by centralizing payment processing and cancellation procedures. In practice, this consolidation frequently generates confusion regarding service ownership and account management. Different streaming providers maintain varying policies regarding marketplace integrations. Some services allow direct cancellation through their own portals regardless of enrollment origin. Others mandate that subscribers interact exclusively with the marketplace platform for account modifications.

This inconsistency requires viewers to track multiple cancellation pathways and payment rules. Financial control also diminishes when subscriptions are routed through a single aggregator. Direct billing enables the use of limited-use payment methods to cap monthly expenses. Marketplace subscriptions typically require permanent payment method linkage across all enrolled services. This structure complicates budget tracking and increases exposure to unexpected price adjustments. The administrative burden shifts from the consumer to the platform, which benefits from reduced friction in subscription retention.

Transparency suffers when billing statements list aggregated marketplace charges rather than individual service line items. Consumers lose visibility into which specific catalogs are driving their monthly costs. This opacity makes it difficult to evaluate whether a particular service justifies its continued presence in a household budget. Direct billing statements provide clear itemization that supports informed financial decisions. Viewers can easily identify unused services and terminate them before the next billing cycle. This transparency parallels the detailed breakdown found in recent technology previews, where clear reporting eliminates confusion and supports informed financial decisions.

When third-party platforms actually provide tangible value

Certain scenarios justify utilizing streaming marketplaces despite their inherent limitations. Free trial periods represent a primary exception where third-party platforms maintain a distinct advantage. Some aggregators continue offering introductory trial windows even after direct providers have eliminated them. These trials enable viewers to evaluate specific content libraries without immediate financial commitment. Exclusive promotional pricing also occasionally favors marketplace enrollment. Limited-time discounts on specific catalogs can outweigh the long-term benefits of direct billing. Consumers should carefully compare marketplace offers against current direct pricing before committing.

Bundle configurations present another potential advantage when they align with actual viewing preferences. Some aggregators combine less popular services into discounted packages that reduce overall monthly expenditure. These arrangements only provide value when subscribers consistently utilize the included catalogs. Platform consolidation offers minimal utility when it fails to generate measurable cost savings. The administrative convenience of unified billing rarely compensates for restricted access pathways and limited promotional eligibility. Viewers should approach marketplace subscriptions with strict cost-benefit analysis rather than accepting consolidation as an inherent improvement.

The streaming economy continues to evolve as platforms compete for subscriber attention and retention. Third-party marketplaces offer a centralized approach to digital entertainment billing, yet they frequently prioritize ecosystem control over consumer flexibility. Direct subscriptions through official service channels consistently deliver superior pricing structures, broader device compatibility, and clearer financial management. Consumers who navigate this landscape effectively maintain direct relationships with content providers while selectively utilizing marketplace trials and discounts. The long-term strategy for sustainable streaming consumption relies on deliberate enrollment choices and active budget monitoring. Understanding the structural differences between payment channels empowers viewers to optimize their digital entertainment expenses without compromising access or convenience. This deliberate approach ensures that households retain full authority over their media spending and content preferences.

The evolution of digital entertainment distribution has fundamentally altered how consumers acquire media. Early streaming models relied on direct downloads and standalone applications. As the market matured, technology companies recognized the revenue potential of acting as intermediaries. These intermediaries capture a percentage of every transaction while positioning themselves as essential gatekeepers. This business model encourages platforms to discourage direct enrollment through aggressive interface design and promotional positioning. Viewers must actively resist default checkout pathways to avoid unnecessary marketplace fees.

Platform fees directly impact the pricing strategies of content creators. When subscriptions route through third-party aggregators, the underlying providers receive reduced revenue shares. This financial structure incentivizes streaming services to raise direct subscription prices to compensate for marketplace cuts. Consumers who unknowingly enroll through these channels inadvertently support a pricing model that ultimately increases their long-term costs. Direct billing bypasses intermediary fees and allows content providers to offer more competitive monthly rates.

Developing a systematic approach to subscription management requires regular financial audits. Households should maintain a centralized ledger of all active streaming services and their respective renewal dates. This practice prevents accidental renewals and highlights opportunities to pause services during off-peak viewing periods. Consumers should also monitor official service newsletters for flash sales and loyalty discounts. These direct communications frequently contain time-sensitive offers that third-party platforms never replicate.

The fragmentation of streaming applications has created significant usability challenges for modern households. Different devices prioritize different content ecosystems based on proprietary partnerships. Smart televisions and streaming sticks often display marketplace subscriptions prominently on their home screens. This visual hierarchy subtly encourages users to select platform-locked options over direct alternatives. Savvy viewers must manually navigate device settings to locate direct service applications and establish independent login credentials.

Industry analysts predict continued consolidation as streaming providers seek sustainable monetization models. The current marketplace structure may eventually standardize across major technology firms. However, consumer awareness of direct billing advantages will likely persist as a counterbalance. Educational resources and financial tracking tools will remain essential for navigating this evolving landscape. Viewers who prioritize transparency and cost efficiency will consistently outperform those who accept platform defaults.

The fundamental distinction between direct and marketplace subscriptions ultimately rests on consumer agency. Third-party platforms excel at convenience but frequently compromise on financial transparency and content flexibility. Direct enrollment preserves the ability to switch devices, cancel services, and access promotional pricing without intermediary restrictions. Maintaining independent accounts ensures that viewers control their digital entertainment experience rather than surrendering it to platform algorithms. This approach aligns with broader principles of digital ownership and informed consumer choice.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)