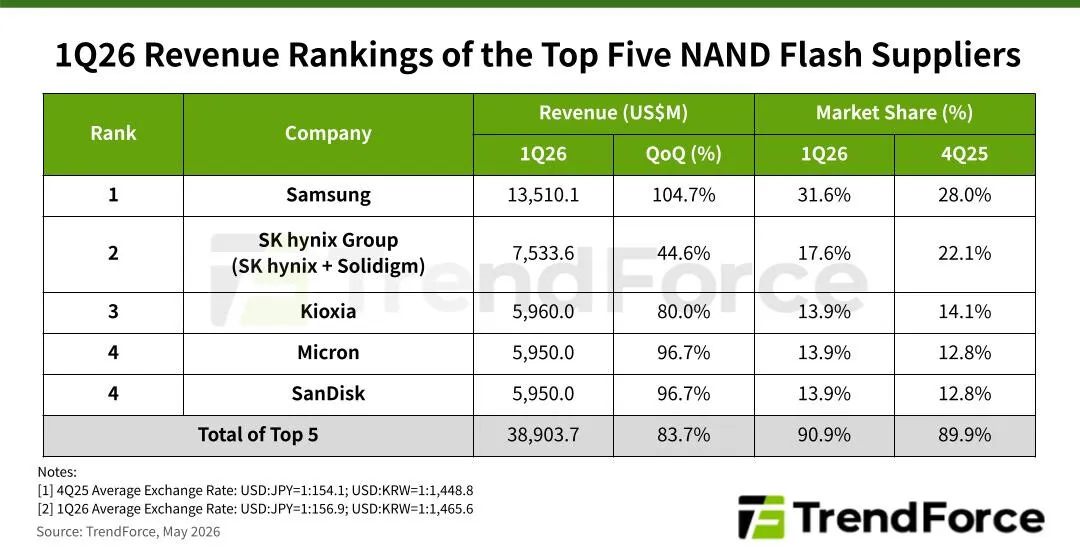

NAND Flash Revenue Surges 83.7% as AI Infrastructure Drives SSD Demand

Cloud service providers have triggered an exponential surge in enterprise solid state drive demand during the first quarter of 2026. This increased requirement for high-speed data transmission and massive storage capacity has directly caused supply shortages that drove significant price increases. The combined revenue of the five largest global NAND flash suppliers consequently rose by eighty-three point seven percent quarter over quarter.

What is driving the exponential surge in enterprise SSD demand?

Cloud service providers worldwide are currently constructing massive data centers to support the computational workloads required by artificial intelligence applications. These applications process vast quantities of information simultaneously, which necessitates storage systems capable of handling extremely high-speed data transmission. Enterprise solid state drives have become the foundational component for these infrastructure projects, fundamentally altering how modern networks operate and process information.

The architecture of modern data centers relies heavily on flash memory technology to ensure rapid read and write operations. Manufacturers are adjusting their production schedules to meet the stringent performance requirements of these enterprise environments. The shift toward specialized storage solutions reflects a broader industry transition toward distributed computing models that prioritize latency reduction and parallel processing capabilities.

Data centers must balance processing power with storage density to maintain operational efficiency. This balance requires continuous investment in advanced semiconductor fabrication techniques. The current market dynamics indicate that storage capacity will remain a critical bottleneck for future technological advancement. Organizations must carefully evaluate their hardware procurement strategies to avoid operational delays during peak demand periods.

Historical trends in semiconductor manufacturing demonstrate that storage technology evolves alongside computational demands. Early data centers relied on mechanical hard drives, but the latency associated with rotating platters proved insufficient for modern workloads. The transition to solid state architecture eliminated mechanical bottlenecks and enabled parallel data processing at unprecedented speeds. This architectural shift fundamentally changed how cloud providers design their server racks.

Enterprise customers now expect consistent low-latency responses regardless of workload intensity. The reliability of flash memory ensures that critical applications remain available during peak processing periods. Manufacturers continue to refine cell density and endurance metrics to extend the operational lifespan of enterprise drives. These technical improvements directly support the massive data storage capacities required to build out AI server infrastructure.

How do supply shortages influence global pricing structures?

The rapid expansion of data center infrastructure has outpaced the current manufacturing capacity for advanced NAND flash memory. When demand exceeds available supply, manufacturers naturally adjust their pricing strategies to reflect market scarcity. The combined revenue of the top five global NAND flash suppliers increased by eighty-three point seven percent quarter over quarter during the first quarter of 2026.

This substantial revenue growth directly correlates with the elevated pricing caused by constrained supply chains. Semiconductor fabrication requires significant capital investment and specialized equipment, which limits how quickly production can scale. Suppliers are prioritizing high-margin enterprise products over consumer-grade alternatives to maximize profitability during periods of tight inventory. This strategic reallocation of manufacturing resources further reduces the availability of standard storage components.

The pricing adjustments also serve as a mechanism to manage demand and prevent market overheating. Companies purchasing enterprise storage must account for these volatile pricing environments when planning long-term infrastructure budgets. Quarter-over-quarter revenue calculations in the semiconductor industry capture short-term market fluctuations and long-term strategic positioning. A significant increase in combined revenue among leading suppliers indicates robust demand across multiple industry verticals.

The pricing mechanism ensures that manufacturing capacity is allocated to the most critical applications first. This prioritization stabilizes the supply chain for essential technology sectors. Supply chain constraints often trigger a ripple effect across the broader electronics market. Component shortages force system integrators to revise their product roadmaps and adjust release schedules. The resulting price hikes reflect the true cost of securing manufacturing slots during peak demand periods.

What does this revenue shift mean for the broader technology sector?

Organizations must navigate these financial realities to maintain competitive infrastructure capabilities. The financial performance of major semiconductor suppliers provides valuable insight into the health of the global technology ecosystem. A significant quarter-over-quarter revenue increase among leading NAND flash manufacturers indicates robust demand across multiple industry verticals. Enterprise customers are allocating substantial capital expenditures toward data center expansion to support emerging computational workloads.

This investment cycle typically precedes broader economic shifts in software development and digital services. The concentration of revenue among the top five suppliers highlights the oligopolistic nature of the advanced memory market. Large-scale fabrication facilities require specialized expertise and immense financial resources, which naturally consolidates market share among established players. Smaller manufacturers struggle to compete with the economies of scale and research capabilities of industry leaders.

This consolidation influences long-term pricing stability and innovation trajectories across the semiconductor industry. Market participants must monitor these concentration trends to anticipate future supply chain vulnerabilities. The strategic realignment of manufacturing capacity reflects a broader industry response to technological disruption. As artificial intelligence applications become more complex, the demand for high-speed data transmission continues to accelerate.

Suppliers are investing heavily in next-generation fabrication processes to meet these evolving requirements. These investments will determine the competitive landscape for years to come. Enterprise IT departments must adapt their procurement strategies to align with these market realities. Long-term contracts and diversified supplier relationships provide greater financial predictability during volatile periods. The technology sector will likely see continued consolidation as companies seek to secure reliable hardware supply chains.

How are cloud service providers adapting to storage constraints?

Cloud service providers are implementing multiple strategies to mitigate the impact of enterprise solid state drive shortages. Many organizations are redesigning their data center architectures to optimize storage utilization and reduce dependency on single-source suppliers. Diversifying procurement channels allows these providers to negotiate more favorable terms during periods of market volatility. Some companies are investing directly in semiconductor manufacturing partnerships to secure long-term supply agreements.

These vertical integration efforts help stabilize inventory levels and protect profit margins from sudden pricing fluctuations. Additionally, cloud providers are exploring alternative storage technologies that offer different performance and cost characteristics. The industry is gradually shifting toward more efficient data compression algorithms and tiered storage architectures. These technical adaptations help maximize the utility of existing hardware while waiting for supply chains to normalize.

The strategic response to current shortages will likely shape data center design standards for the coming decade. Data center operators are also reevaluating their workload distribution models to reduce storage pressure. Moving non-critical data to lower-cost archival systems frees up high-performance enterprise drives for active workloads. This tiered approach optimizes capital expenditure while maintaining acceptable service level agreements. The methodology represents a fundamental shift in how cloud infrastructure is managed.

Supply chain resilience has become a primary consideration for technology executives. Organizations that fail to anticipate hardware availability constraints may face significant operational delays. Proactive inventory management and strategic supplier partnerships are essential for maintaining continuous service delivery. The industry will continue to prioritize reliability alongside raw performance metrics. The current market conditions underscore the critical importance of resilient supply chain management in the technology sector.

What are the long-term implications for data infrastructure planning?

Organizations that fail to anticipate semiconductor availability constraints may face significant operational delays during infrastructure expansion projects. Long-term planning now requires close coordination between hardware manufacturers, cloud providers, and enterprise IT departments. Supply chain transparency and predictive analytics are becoming essential tools for managing hardware procurement cycles. The industry is also placing greater emphasis on sustainable manufacturing practices to address environmental concerns associated with semiconductor production.

Regulatory frameworks regarding data sovereignty and hardware security will further influence how storage infrastructure is deployed globally. Companies must balance immediate performance requirements with long-term strategic positioning in a rapidly evolving market. The intersection of artificial intelligence development and semiconductor manufacturing will continue to drive innovation in data storage technologies. Future infrastructure development will depend heavily on the ability to align hardware procurement with emerging computational demands.

Navigating the Future of Data Storage Infrastructure

As data center expansion continues, the semiconductor industry will face sustained pressure to increase production capacity while maintaining quality standards. Stakeholders across the technology ecosystem must adapt to these shifting market conditions through strategic planning and collaborative supply chain management. The ongoing evolution of enterprise storage requirements demonstrates how technological advancement directly influences global manufacturing priorities. As artificial intelligence applications continue to mature, the demand for high-speed data transmission will only intensify.

Manufacturers must balance immediate production constraints with long-term capacity expansion to meet industry expectations. Enterprise customers are increasingly viewing storage infrastructure as a strategic asset rather than a commodity. This perspective shift encourages more rigorous evaluation of total cost of ownership and operational efficiency. The technology sector will likely see continued innovation in both hardware architecture and supply chain logistics. Organizations that successfully navigate these market dynamics will secure a competitive advantage in the digital economy.

The intersection of computational demand and semiconductor supply will define the next era of data infrastructure. Strategic foresight and adaptive procurement practices remain essential for long-term success. The ongoing evolution of enterprise storage requirements demonstrates how technological advancement directly influences global manufacturing priorities. As artificial intelligence applications continue to mature, the demand for high-speed data transmission will only intensify. Manufacturers must balance immediate production constraints with long-term capacity expansion to meet industry expectations.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)