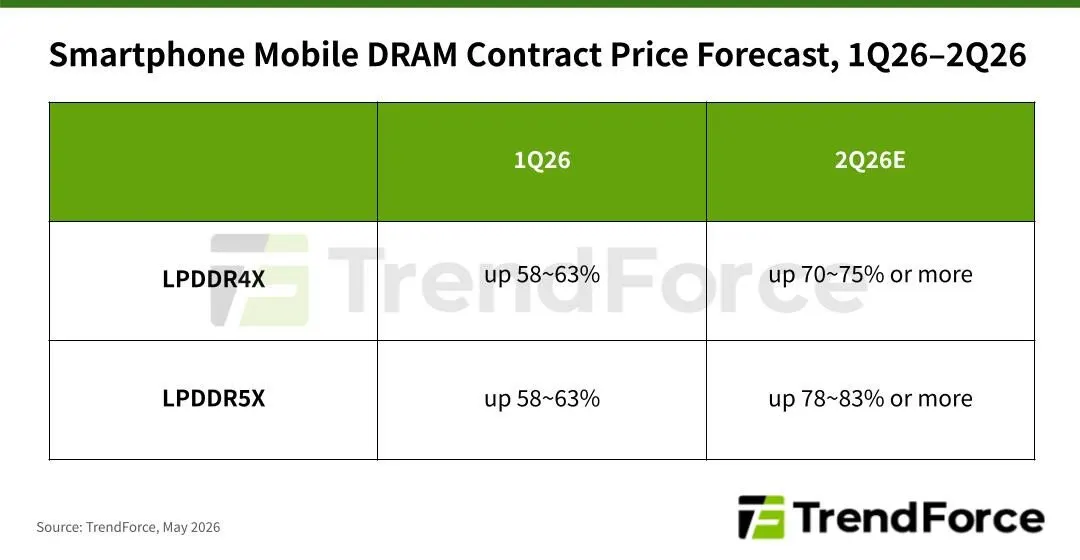

Mobile DRAM Contract Prices Rise in 2Q26, Reshaping Smartphone Economics

Mobile dynamic random-access memory contract prices continue their upward trajectory in the second quarter of 2026, according to recent industry research. This sustained cost escalation places significant financial pressure on smartphone manufacturers, who must now navigate complex procurement strategies while managing broader operational expenditures and maintaining competitive device pricing.

The global semiconductor landscape operates on predictable cycles of scarcity and abundance, yet recent market data indicates a sustained upward trajectory in mobile dynamic random-access memory contract prices during the second quarter of 2026. This continued escalation places measurable financial strain on device manufacturers who must balance component procurement with broader operational expenditures. As supply chain dynamics shift, the ripple effects extend far beyond silicon fabrication facilities into the assembly lines that produce consumer electronics.

Why are mobile DRAM contract prices rising in 2Q26?

The ongoing increase in mobile DRAM contract prices stems from a combination of constrained manufacturing capacity and shifting demand patterns across the consumer electronics sector. Memory producers have historically adjusted output levels based on long-term market forecasts, but recent quarters have demonstrated a more cautious approach to capital expenditure. This deliberate pacing of production expansion means that supply growth has not kept pace with the steady accumulation of orders from device manufacturers. Consequently, the fundamental economic principle of supply and demand drives contract negotiations toward higher valuation thresholds.

Contract pricing mechanisms in the semiconductor industry operate on quarterly or semi-annual cycles, which means that once agreements are signed, the financial commitment remains fixed for a predetermined period. This structure provides manufacturers with cost predictability, yet it also locks them into prevailing market rates during periods of rapid inflation. When major suppliers adjust their baseline pricing to reflect increased production costs or strategic inventory management, downstream buyers immediately feel the impact. The current environment reflects a broader industry recalibration where suppliers prioritize margin protection over aggressive market share expansion.

The strategic divergence among leading memory manufacturers further complicates the pricing landscape. While some producers maintain conservative pricing frameworks to preserve long-term customer relationships, others are implementing more aggressive valuation adjustments to offset rising operational expenses. This bifurcation forces smartphone brands to evaluate their procurement channels more carefully, often resulting in diversified supplier portfolios. The goal remains consistent across the industry: secure adequate memory inventory to meet production schedules while avoiding excessive financial exposure during volatile market conditions.

Historical memory market cycles typically alternate between periods of oversupply and deliberate capacity constraints. The current phase aligns with a broader industry trend where manufacturers have shifted focus toward higher-margin product segments and advanced process nodes. This strategic pivot naturally reduces the available volume of standard mobile memory modules, creating a structural imbalance that contract pricing must reflect. Device makers must now account for these macro-level supply chain adjustments when forecasting quarterly financial performance and annual production targets.

How does memory pricing affect smartphone manufacturing costs?

Dynamic random-access memory represents a critical component within modern smartphone architecture, directly influencing both device performance and overall production expenses. As memory requirements expand to support advanced processing capabilities, enhanced camera systems, and increasingly complex operating environments, the proportion of total bill of materials allocated to memory modules continues to grow. When contract prices rise, manufacturers face immediate pressure to absorb additional costs or adjust retail pricing strategies to maintain healthy profit margins.

The financial impact varies significantly across different market segments. Premium device manufacturers often possess greater negotiating leverage and can distribute additional component costs across higher retail price points without severely impacting consumer demand. Conversely, budget and mid-tier brands operate with thinner margins and must navigate procurement challenges more carefully. These companies frequently explore alternative sourcing strategies, renegotiate supplier agreements, or adjust internal cost structures to mitigate the financial burden of rising memory expenses.

Supply chain logistics also play a substantial role in how pricing fluctuations translate into manufacturing realities. Securing adequate memory inventory requires precise coordination between procurement teams, assembly facilities, and component distributors. When contract prices increase, the financial commitment required to secure necessary inventory grows proportionally, which can strain working capital and influence production scheduling. Manufacturers must balance the need for immediate component availability against the long-term financial health of their procurement departments.

Hardware evolution continues to drive memory consumption upward, as modern smartphones demand faster data throughput and larger storage capacities for multimedia processing and artificial intelligence workloads. This technological progression means that even if unit prices remained stable, the overall memory expenditure per device would still climb due to increased capacity requirements. The current contract price escalation compounds this effect, forcing engineering and procurement teams to collaborate more closely on component optimization and architectural efficiency.

What strategic adjustments are suppliers implementing?

Leading memory producers are responding to the current market environment by recalibrating their production allocations and refining their pricing methodologies. The two major Korean suppliers have adopted distinct approaches to navigate the shifting landscape, with one pursuing a more aggressive pricing strategy while the other maintains a steadier valuation framework. This divergence creates a complex procurement environment where smartphone brands must carefully evaluate supplier terms, delivery guarantees, and long-term partnership potential.

Memory manufacturers are also prioritizing yield optimization and advanced node development to improve overall profitability. By focusing on higher-performance modules and reducing waste during the fabrication process, suppliers can offset rising operational costs without excessively burdening downstream customers. This strategic emphasis on technical advancement aligns with broader industry trends where component quality and reliability take precedence over sheer volume production. The result is a more selective supply chain where only manufacturers with robust financial backing can secure favorable contract terms.

Inventory management has become a critical differentiator among memory producers. Companies that maintain strategic buffer stocks during periods of price volatility can offer more stable pricing to long-term partners, while those operating with leaner inventory models must adjust contracts more frequently to reflect current market conditions. This dynamic influences how smartphone brands structure their purchasing agreements, often leading to longer-term commitments or multi-year pricing frameworks that provide greater financial predictability.

The broader semiconductor ecosystem is also witnessing increased collaboration between memory producers and system integrators. Joint development initiatives and shared forecasting models help align production schedules with actual market demand, reducing the risk of sudden price shocks. These collaborative approaches allow both suppliers and device manufacturers to navigate contract pricing fluctuations with greater precision, ultimately fostering a more resilient supply chain that can adapt to evolving technological requirements.

How will device makers navigate the current market environment?

Smartphone manufacturers are responding to rising memory costs by implementing more sophisticated procurement strategies and diversifying their component sourcing networks. Many companies are establishing direct relationships with multiple memory producers to reduce dependency on single suppliers and create competitive leverage during contract negotiations. This approach allows device makers to secure favorable pricing terms while maintaining flexibility to adjust purchasing volumes based on market conditions.

Financial planning departments are also revising their cost allocation models to account for sustained memory price increases. By integrating long-term procurement forecasts into quarterly earnings projections, manufacturers can better anticipate margin pressures and adjust retail pricing accordingly. This proactive financial management helps prevent sudden cost shocks from disrupting production schedules or forcing abrupt changes to product roadmaps. Companies that successfully navigate these adjustments often emerge with stronger competitive positioning and more resilient supply chain structures.

Product development teams are simultaneously exploring architectural optimizations to reduce memory dependency without compromising device performance. Engineers are working closely with memory producers to develop customized solutions that maximize efficiency while minimizing overall component costs. These collaborative efforts often result in innovative hardware configurations that deliver enhanced capabilities without proportionally increasing the bill of materials. The industry continues to prioritize balanced design philosophies that align technical requirements with economic realities.

Consumer electronics markets are also witnessing a shift toward modular component design, which allows manufacturers to upgrade specific subsystems without replacing entire device architectures. This approach provides greater flexibility when navigating volatile memory pricing environments, as companies can adjust component specifications on a per-generation basis rather than committing to fixed configurations. The result is a more adaptive manufacturing ecosystem that can respond to supply chain fluctuations without disrupting long-term product development cycles.

What does the future hold for mobile memory markets?

The trajectory of mobile DRAM contract pricing will likely remain influenced by broader semiconductor industry dynamics, including fabrication capacity expansion, technological innovation, and global economic conditions. Memory producers continue to invest heavily in next-generation process nodes and advanced packaging techniques, which will gradually reshape supply availability and pricing structures. These long-term investments suggest that the current pricing environment may stabilize as new production capacity comes online and demand patterns normalize.

Device manufacturers are also preparing for a more complex procurement landscape by strengthening their supply chain resilience and diversifying component sourcing strategies. Companies that successfully navigate the current pricing environment will likely establish stronger competitive advantages through optimized cost structures and more reliable component availability. The industry continues to prioritize long-term partnerships and collaborative forecasting to mitigate the impact of market volatility on production schedules and financial performance.

Technological advancement will remain a driving force behind memory consumption growth, as smartphones continue to integrate more sophisticated processing capabilities and enhanced connectivity features. This ongoing evolution ensures that memory procurement will remain a critical component of device manufacturing strategy, requiring continuous adaptation and strategic planning from all stakeholders in the supply chain. The industry will likely see increased emphasis on efficiency, sustainability, and collaborative innovation as manufacturers work to balance performance requirements with economic realities.

Looking ahead, the mobile memory market will likely experience periodic adjustments as production capacity aligns with demand fluctuations. Companies that maintain flexible procurement strategies and strong supplier relationships will be best positioned to navigate these transitions successfully. The broader consumer electronics sector continues to prioritize sustainable growth models that balance technological advancement with financial stability, ensuring that innovation proceeds without compromising supply chain resilience or market accessibility.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Christopher Holloway is the founder and director of Progressive Robot, a UK-based technology company. A full-stack engineer with more than two decades of experience, he works across PHP development, ecommerce, Linux infrastructure, technical SEO and AI automation, and writes here on technology, AI, hardware and software.

Comments (0)